Owner income$145k

Owner income$145kHow Much Can A TAM Analysis Service Owner Make With $156M Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$145k  Net margin32% to 66%

Net margin32% to 66% Revenue for target pay$452k

Revenue for target pay$452k Business difficultyHard

Business difficultyHard

You’re planning owner pay before the delivery machine is fully proven, so the clean answer is this: the model shows $145,000 in annual owner salary plus business profit capacity that depends on reserves and reinvestment This first-year through mature-year view covers revenue, gross margin, operating costs, cash reserves, target pay, and scenarios for a US owner-operated TAM analysis service These are planning assumptions, not tax advice, salary guarantees, or automatic distributions

Owner income$145kNet margin32% to 66%Revenue for target pay$452kBusiness difficultyHardWant to test your own TAM consulting income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

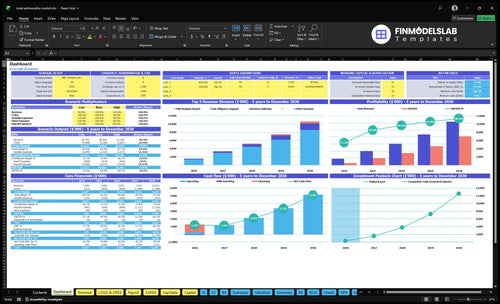

Want to see the owner-pay model behind the numbers?

This dashboard shows revenue, margin, costs, reserves, and owner take-home assumptions in the Total Addressable Market Analysis Service Financial Model Template—open it.

Owner-income model highlights

- Owner pay, clearly shown

- Revenue and EBITDA ramp

- Month 5 breakeven

- Scenario tests pricing tiers

How many TAM analysis projects to make 100k?

If you want $100,000 in owner pay from a Total Addressable Market Analysis Service, the math points to about $711,500 in annual revenue, not a fixed promise. Here’s the quick math: ($272,500 + $94,800 + $45,000 + $100,000) / 72% = about $711,500, and at $8,000 per report, that is about 89 reports a year, or 74 per month, before reserves and taxes. One clean truth: volume has to do the heavy lifting.

Revenue math

- $8,000 per TAM report

- 40 hours per project

- $200/hour billing rate

- 72% contribution after costs

Project volume

- 89 reports for $100,000 owner pay

- 74 reports/month before taxes

- $272,500 non-owner payroll

- $94,800 fixed overhead plus $45,000 marketing

What is the profit margin for a TAM analysis service?

The profit margin for a Total Addressable Market Analysis Service is driven by delivery costs, not personal taxes, and you can sanity-check it against What Are The 5 KPI Metrics For Total Addressable Market Analysis Service?. Modeled EBITDA margin moves from 32% in Year 1 to 50%, 56%, 62%, and 66% by Year 5. Gross margin after premium data and verification costs improves from 80% to 87%, while contribution margin after referral commissions and cloud hosting improves from 72% to 83%. Analyst labor, data subscriptions, verification, revision cycles, and QA time can lift credibility, but they cut owner take-home if not priced into the engagement.

Margin path

- 32% EBITDA in Year 1

- 50% in Year 2

- 56% in Year 3

- 66% by Year 5

Cost drivers

- Gross margin rises from 80% to 87%

- Contribution margin rises from 72% to 83%

- Premium data and verification lift trust

- QA and revisions must be priced in

How much does a TAM analysis service owner make per year?

A Total Addressable Market Analysis Service owner can model $145,000 per year as CEO and Lead Strategist salary, then add approved distributions only after cash reserves and reinvestment are funded; for margin planning, see How Increase Total Addressable Market Analysis Service Profitability?. This is owner-operated profit, not a payroll benchmark: the model also carries a $95,000 Senior Research Analyst salary.

Owner take-home

- $145,000 modeled annual owner salary

- $500,000 Year 1 EBITDA

- $2.952 million Year 3 EBITDA

- $7.03 million Year 5 EBITDA

What matters

- Pay salary first, distributions second

- Keep reserves before owner draws

- Reinvest before taking excess cash

- Separate owner profit from analyst payroll

Which six drivers move TAM consulting owner income most?

1

$8K-$8.8KAverage Fee

A TAM report moves from about $8,000 in Year 1 to $8,750 in Year 5, so fee growth directly lifts take-home on every project.

2

$1.6M-$10.6MProject Volume

More projects, tied to 12.5 to 16.0 billable hours per active customer, drives the biggest swing in top-line revenue and owner income.

3

40-35hLabor Efficiency

Dropping TAM report effort from 40 hours to 35 hours frees capacity, so more revenue fits into the same team.

4

20%-13%Data Costs

Premium data and verification costs fall from 20% to 13%, which keeps more gross profit on each report.

5

$250-$325Client Mix

Shifting more work into due diligence support lifts the hourly rate from $250 to $325 and raises blended pricing.

6

10%-30%Recurring Upsells

Growing retainer advisory from 10% to 30% improves lifetime value and smooths cash flow between big projects.

Total Addressable Market Analysis Service Core Six Income Drivers

Average Project Fee And Scope

Average Project Fee and Scope

This driver is the revenue you earn per engagement, and it moves owner income fast. A TAM report is $8,000 in Year 1 at 40 hours × $200/hour, then $8,750 in Year 5 at 35 hours × $250/hour. Due diligence support starts at $5,000 from 20 hours × $250/hour and reaches $8,125 from 25 hours × $325/hour.

Scope matters as much as price. Higher-fee work can include TAM, SAM, SOM, investor-ready assumptions, segmentation, and methodology notes. The risk is simple: if price rises faster than documentation, data validation, or client value, you sell more hours but not better profit. That can slow cash collection and force more rework, which cuts owner draw.

How to raise fee without hurting margin

Track fee per engagement, hours by work type, and revision count. Here’s the quick math: if a report takes 40 hours and sells for $8,000, each hour must stay defensible. If due diligence support climbs to 25 hours, the extra scope needs a higher rate or a clear change order, not just “more work.”

- Price by scope, not effort.

- Separate TAM, SAM, SOM.

- Charge for extra revisions.

- Document sources and assumptions.

- Test whether clients pay more.

What this estimate hides is quality risk. If the model is thin or the data trail is weak, a higher fee can backfire through refunds, slow approvals, and client pushback. Stronger methodology notes and cleaner validation usually support better pricing more than extra sales effort does.

1

Monthly Project Volume And Pipeline

Monthly Project Volume

Monthly volume drives booked revenue and owner pay, but only when pipeline turns into shippable work. Here’s the quick math: marketing budget rises from $45,000 in Year 1 to $150,000 in Year 5, while CAC improves from $1,200 to $950. That helps fill the funnel, but revenue only lands if close rate and delivery capacity keep up.

Demand gen is not the same as fulfillment. For TAM analysis, the real constraints are proposal speed, turnaround time, analyst bandwidth, and revision load. If active customer billable hours rise from 125 to 160 per month, that is a 28% jump in workload per account, so overselling can lift revenue and still cut margin if quality slips.

Track Pipeline Against Capacity

Measure the pipeline by stage: leads, proposals sent, close rate, and months of analyst hours already committed. The owner should also track how many TAM, SAM, and SOM projects can ship each month without pushing revisions into the next cycle. One clean rule: booked work should never outrun delivery hours.

- Close rate by channel

- Days to proposal

- Average revision rounds

- Hours sold vs. hours available

Use these numbers to price rush work, cap intake, and protect quality. If proposal speed slows or revision load climbs, booked revenue can look strong while cash flow weakens from churn, rework, and delayed delivery. For the owner, the goal is simple: keep utilization high, but leave enough slack for defensible analysis and fast payback.

2

Delivery Labor Efficiency

Delivery Labor Efficiency

Delivery labor efficiency is the hours it takes to produce a defensible TAM, SAM, or SOM report. This driver hits gross margin and owner capacity: a TAM report drops from 40 hours in Year 1 to 35 hours in Year 5, while fee power also rises from $8,000 to $8,750. Fewer hours per deliverable means more projects can ship without adding the same amount of labor.

Protect Hours, Keep QA Tight

Track hours by work type: TAM reports, retainer advisory, and due diligence support. The model shows retainer hours rising from 10 to 15 and due diligence from 20 to 25, so efficiency should come from templates, research workflows, analyst support, and QA checklists, not from rushed analysis. Weak QA can trigger refunds, revisions, and reputation loss, which cuts cash flow and owner pay.

3

Data, Software, And Research Source Costs

Research Source Costs

For TAM work, the source stack means paid data, validation sources, survey inputs, analyst tools, and cloud hosting. Those costs support the credibility premium that lets you charge more, but they also hit margin fast: premium data is 15% of revenue in Year 1 and 10% in Year 5.

Here’s the quick math: external verification adds 5% in Year 1 and 3% in Year 5, plus cloud hosting at 3% and 2%. That is 23% of revenue in Year 1 and 15% in Year 5 before labor. If you treat these as overhead instead of pricing them into proposals and change orders, owner pay gets squeezed.

Price the Source Stack

Track source cost per project, not just total spend. Use revenue per engagement, source cost as a % of revenue, and change-order recovery to see if fees cover the research burden. If a scope needs extra data pulls, survey work, or verification, price it into the proposal before you start.

- Log source cost by project

- Quote verification as separate scope

- Recover extra data in change orders

- Review margin after each delivery

One clean rule: if the research stack rises and pricing stays flat, gross margin falls. Protect take-home income by setting a floor for paid data and tools, then testing whether faster turnaround or stronger diligence support justifies a higher fee.

4

Client Mix And Positioning

Client Mix Drives Net Income

Client mix sets both price and revision load. In Year 1, TAM report work is 75% of allocation, then drops to 55% by Year 5 as retainer advisory rises from 10% to 30% and due diligence support from 15% to 35%. That shift can lift revenue per client, but only if the extra review time and documentation still leave room for owner pay.

Founder-led startup work may close faster, but it needs tight price discipline. Investor pitch work needs clear assumptions, and agency subcontracting can cut sales effort while compressing margin. Enterprise strategy and diligence work can pay more, but the tradeoff is faster turnaround, deeper docs, and more revisions. One bad mix decision can raise revenue and still lower take-home profit.

Track Mix by Margin, Not Just Revenue

Measure each segment by fee per engagement, revision hours, and gross margin. A higher-fee diligence project is not better if it needs two extra rounds of edits and pulls the owner off sales.

- Split work by start up, retainer, diligence.

- Track revision hours per project.

- Price faster-turnaround work higher.

- Cap low-margin subcontracted volume.

Use the mix to protect cash flow. If retainers rise toward 30%, set a clear update cadence so support does not turn into open-ended labor. If diligence rises toward 35%, build in assumption checks and change-order rules so extra revisions do not eat the margin that pays the owner.

5

Recurring Updates And Upsells

Recurring Updates And Upsells

Retainer revenue lifts lifetime value and smooths cash flow because old TAM work can be refreshed into total addressable market (TAM), serviceable available market (SAM), serviceable obtainable market (SOM) expansion, competitor sizing, segmentation, investor deck support, and diligence follow-on work. The rate moves from $175/hour in Year 1 to $225/hour in Year 5, and retainer mix rises from 10% to 30%. That helps profit, but only if the client keeps buying current data.

This is not passive income. The owner still has to keep methodology clear, source data current, and response times tight. If the update cadence is vague, the retainer turns into extra support work with weak pricing, which can squeeze gross margin and lower take-home pay.

Set A Clear Refresh Cadence

Track retainer hours, update frequency, hours per refresh, and renewal rate. Tie each retainer to a fixed deliverable, like a quarterly market refresh, a new competitor set, or a revised sizing model. That makes revenue easier to forecast and keeps owner pay tied to repeat work, not open-ended favors.

- Set monthly or quarterly check-ins.

- Price scope changes separately.

- Log source dates on every model.

- Hold time for client questions.

Here’s the quick math: 10% to 30% retainer allocation means more stable revenue, but only if the hours are planned. If the rate steps from $175/hour to $225/hour, the gain sticks only when current research, redlines, and turnaround times stay controlled.

6

Compare lean, base, and high-capacity TAM consulting income scenarios

Owner income scenarios

Owner income rises as work shifts from one-off TAM reports to retainers and due diligence. Staffing, data costs, and cash needs decide how much EBITDA reaches the owner.

| Scenario | LowLean case | BaseCore case | HighUpside case |

|---|---|---|---|

| Launch model | This is the launch-year case with slower owner income and a salary-first setup. | This is the modeled middle case with broader service mix and steadier owner income. | This is the stronger earnings path if delivery keeps up with faster growth. |

| Typical setup | Year 1 models $1.558M revenue, $500k EBITDA, a 32% margin, $145k CEO pay, breakeven in Month 5, and minimum cash of $810k in Month 2. | Year 3 models $5.235M revenue, $2.952M EBITDA, and a 56% margin with 3 Senior Research Analyst FTE and 1.5 Data Scientist FTE. | Year 5 models $10.614M revenue, $7.03M EBITDA, and a 66% margin with 5 Senior Research Analyst FTE and 2 Data Scientist FTE. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $500kEarly cash | $2.95MScaled profit | $7.03MCapacity stretch |

| Best fit | Use this to stress-test launch cash, sales pace, and whether the model can carry the owner salary. | Use this as the planning base for hiring, pricing, and cash flow. | Use this to test delivery capacity, staffing risk, and how much owner income survives after reinvestment. |

Planning note: These ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or set distributions.

Related Products

- Total Addressable Market Analysis Service Porter's Five Forces Analysis

- Total Addressable Market Analysis Service BCG Matrix

- Total Addressable Market Analysis Service Business Model Canvas

- How Increase Profitability Of Total Addressable Market Analysis Service?

- Total Addressable Market Analysis Business Plan Template in Pre-Written Word

- How Increase Profitability Of Total Addressable Market Analysis Service?

- How Increase Profitability Of Total Addressable Market Analysis Service?

- How Much It Costs To Start A TAM Analysis Service: $852K CAPEX

- Total Addressable Market Analysis Service Financial Model Template in Excel

- How To Start A TAM Analysis Service In 4 To 8 Weeks

- How Increase Profitability Of Total Addressable Market Analysis Service?

- Total Addressable Market Analysis Service Marketing Mix

- Total Addressable Market Analysis Service Marketing Plan

- Total Addressable Market Analysis Service Business Proposal

- Total Addressable Market Analysis Service PESTEL Analysis

- Total Addressable Market Pitch Deck Example Editable PPTX

- Total Addressable Market Analysis Service Business SWOT Analysis

- Total Addressable Market Analysis Service Value Proposition Canvas

Frequently Asked Questions

The modeled owner salary is $145,000 per year before personal taxes Business profit is separate: EBITDA is $500,000 in Year 1 and $703 million in Year 5 Any distribution above salary depends on cash reserves, reinvestment, debt service, and whether the owner keeps profit inside the business