Owner income$200k

Owner income$200kHow Much Does a Business Transition Services Owner Make at $184M Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$200k  Net marginBelow 0%

Net marginBelow 0% Revenue for target pay$1.95M

Revenue for target pay$1.95M Business difficultyHard

Business difficultyHard

Under the researched assumptions, a business transition services owner can plan around a $200k annual managing partner salary, but extra pre-tax take-home is not supported until the firm clears overhead, payroll, delivery costs, reserves, and reinvestment Revenue grows from about $325k in Year 1 to about $184M in Year 5 Service gross margin improves from 885% to 915% after third-party specialist fees and data room technology costs The base model still shows no reserve-adjusted distribution because payroll and fixed overhead exceed operating profit

Owner income$200kNet marginBelow 0%Revenue for target pay$1.95MBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Business Transition Services model?

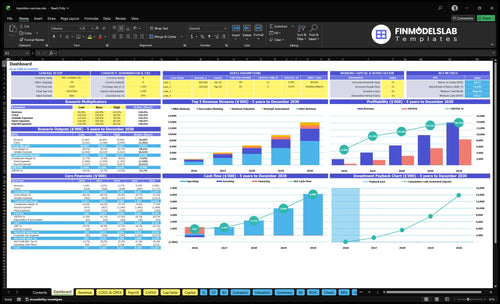

The dashboard shows service revenue, staffing, costs, reserves, and owner pay assumptions; open the Business Transition Services Financial Model Template.

Owner-income model highlights

- Owner pay stays clear

- Service revenue drives margin

- Scenario tabs test assumptions

Are retainers or success fees more profitable for business transition services?

For How Increase Profits Business Transition Services?, retainers are usually the most profitable model because they fund monthly delivery and reduce cash timing risk. Success fees can boost upside, but they’re uncertain, timing-dependent, and may need compliance review. If scope is tight, fixed project fees work; if complexity is unclear, hourly billing protects margin. Model retainer months, collection timing, and specialist costs before calling any fee “profit.”

Retainer model

- Steady monthly cash funds delivery.

- Reduces timing risk on payment.

- Fits ongoing transition work.

- Track retainer months and scope.

Variable fee model

- Success fees add upside.

- Use only if outcome is likely.

- Do not count them as guaranteed income.

- Track probability, timing, and specialist costs.

How much revenue does a business transition services firm need to pay the owner?

A Business Transition Services firm needs about $231M in revenue to pay the owner $200k, using 80% contribution after COGS and variable costs, plus $133M non-owner payroll and $318k fixed overhead. The model says Year 5 revenue is $184M, with a stated gap of about $474k before reserves and taxes. So keep salary, draw, and distribution separate.

Owner pay math

- 80% contribution drives the math

- $133M non-owner payroll is the big load

- $318k fixed overhead is smaller

- $200k owner salary comes last

Cash flow order

- Pay operating costs first

- Hold reserves before distributions

- Keep taxes out of this estimate

- Use owner pay after core costs

How much can a business transition services owner take home?

A Business Transition Services owner can plan on $200,000 in managing partner salary under the modeled cost base, but the model shows no extra profit distribution after costs. The setup in How To Launch Business Transition Services Business? only turns into larger take-home if engagement volume, fee size, utilization, reserves, and cash timing leave profit after payroll and fixed overhead.

Owner Take-Home

- $200,000 planned managing partner salary

- $0 modeled extra profit distribution

- $318,000 modeled fixed cost base

- More margin if overhead stays lower

Profit Levers

- Keep payroll lean in solo mode

- Boutique payroll reaches $153M by Year 5

- Raise fee size per engagement

- Lower CAC, customer acquisition cost

Want the six owner-income drivers?

1

$1.9M-$13.9MEngagement Volume

More qualified engagements drive the fastest take-home growth, with revenue scaling from $1.949M in Year 1 to $13.852M in Year 5 as acquisition spend rises and CAC falls.

2

$275-$495Fee Mix

A better mix toward higher-rate M&A work lifts revenue per hour, since pricing runs from $275 for strategic assessment to $495 for M&A Advisory by Year 5.

3

85-105hBillable Hours

More billable hours spread payroll across more client work, and M&A Advisory alone rises from 85 to 105 hours over the plan.

4

$10.5K-$15KCAC Control

Lower customer acquisition cost protects margin on each new client, and the model improves CAC from $15,000 to $10,500 over five years.

5

45%-55%Deal Mix

A heavier M&A mix and steady succession work support larger, stickier projects and more cross-sell into valuation and assessment.

6

$26.5K/moOverhead Discipline

Fixed overhead runs about $26.5K a month before wages, so reserve discipline matters when payroll scales ahead of demand.

Business Transition Services Core Six Income Drivers

Qualified Engagement Volume

Qualified Engagement Volume

The lever is qualified active engagements, not raw leads. In the model, marketing budget ÷ CAC drives about 12 clients in Year 1 and 40 clients in Year 5; more mandates raise revenue, but only if they are a fit for sale, merger, or succession work and do not trap partner time in bad prospects.

Improve Qualified Intake

Track lead source, close rate, and partner hours per win. Referrals from attorneys, CPAs, bankers, and owners usually cut selling waste and improve fit, while broad marketing can fill the pipeline with low-quality names. Here’s the quick math: if a prospect will not convert into a paid mandate, it still burns time and lowers take-home income.

- Count only qualified mandates.

- Measure CAC by source.

- Drop low-fit channels fast.

1

Average Engagement Value and Fee Mix

Average Engagement Value and Fee Mix

This driver is about how much revenue each client brings in based on hours, hourly rate, and the split between service types. A 85-hour M&A advisory engagement at $400 in Year 1 produces about $34,000, while a 35-hour strategic assessment at $275 produces $9,625. One bigger mandate can equal several small ones, so owner income rises faster when the mix shifts to higher-rate work.

Here’s the quick math: the same M&A advisory work grows to 105 hours at $495 in Year 5, or about $51,975 per client. That is roughly 53% more revenue than Year 1 for the same service line. The catch is scope creep. If the team does not define deliverables tightly, extra meetings and revisions can eat margin and delay cash collection.

Price the mix, not just the hours

Track revenue per client by service line, not just total billings. Split each engagement into hours sold, hours delivered, and realized rate so you can see where pricing holds and where scope leaks. A strategic assessment at $9,625 can be a good entry offer, but it should lead into higher-value advisory work, not replace it.

Also watch success-based fees separately. They can lift upside, but collection timing is uneven, so don’t use them to fund payroll or owner draws. Set a change-order rule, cap revisions, and forecast cash by engagement type. If the mix shifts toward larger mandates without tighter scope control, gross profit can fall even while revenue grows.

2

- Inputs to track: service type, hours, rate

- Price driver: higher-rate work lifts revenue

- Margin risk: scope creep burns labor

- Cash risk: success fees collect later

- Owner impact: better mix supports draws

Advisor Utilization and Delivery Leverage

Advisor Utilization and Delivery Leverage

Revenue capacity is not the same as profit capacity. In this model, owner and senior consultant billable time creates fees, but analysts, project managers, and subcontractors protect delivery scale. If third-party specialist fees fall from 80% to 60% of revenue, and data room technology costs fall from 35% to 25%, gross profit improves and more cash can reach owner pay.

The inputs that matter are billable hours by role, utilization, subcontractor mix, tech spend, and rework. The risk is simple: owner bottleneck, underused staff, or rework. One clean signal is gross profit per engagement. If senior time is spent coordinating instead of billing, fees may hold up, but distributions usually do not.

Track Billable Time and Rework

Measure owner hours, senior consultant hours, analyst and project manager hours, plus subcontractor fees on every job. Then compare those inputs to revenue and gross margin. If a deal needs too much senior time or outside specialist support, the job looks busy but may not pay well. Margin, not just hours, tells you if the team is helping owner income.

To improve this driver, push non-billable work to staff, lock scope early, and review rework by engagement. Keep an eye on the split between revenue and delivery cost, because the gap is what funds overhead and owner draw. If utilization is strong but rework stays high, take-home income still gets squeezed.

3

Referral Pipeline and Client Acquisition Cost

Referral Pipeline and Client Acquisition Cost

Trust drives this business, so referral quality matters more than lead count. The model shows $15k CAC in Year 1 and $105k in Year 5, while annual marketing spend rises from $180k to $420k; if that spend does not produce qualified mandates, partner time gets wasted and owner take-home drops.

This driver includes referral channels, marketing spend, close rate, and sales cycle length. Attorney, CPA, banker, and owner referrals can stabilize intake and reduce selling waste, while broad marketing can fill the pipeline with low-fit prospects that never turn into billable transition work.

Measure CAC by referral source

Track CAC = marketing spend ÷ closed clients, then split it by source so you can see which channels create real transition mandates. A simple view should show referral source, close rate, and first-month billings; that tells you whether a channel is funding profit or just activity.

- Keep attorney referrals warm.

- Keep CPA referrals warm.

- Keep banker referrals warm.

- Cut weak, broad campaigns.

Lower CAC means each dollar buys more client opportunities and more gross margin, so the owner can keep more cash after delivery costs and fixed overhead. If onboarding drags or the firm chases poor-fit prospects, intake risk rises fast and distributions get delayed.

4

Specialization and Transition Complexity

Specialization and Transition Pricing

When the firm shifts toward harder work like sale prep, succession planning, merger transition, and leadership handoff, fee per deal can rise. In this model, M&A Advisory grows from 45% to 55% of mix, while Succession Planning falls from 35% to 25%. That can lift owner income if pricing covers the extra senior time and risk.

Here’s the catch: complex mandates usually need more legal review, valuation support, and longer sales cycles. If a higher fee does not offset those added hours and outside costs, gross margin falls and cash gets tied up longer. In plain terms, specialization can raise revenue quality, but it can also reduce the amount left for owner pay.

Track Fee Mix and Delivery Load

Measure the mix shift, not just total revenue: share of M&A work, share of succession work, senior hours per deal, and outside specialist cost. If complex work uses more owner time, price for that risk up front and write the scope tightly so rework does not eat margin.

Watch sales-cycle leng th, realization, and cash timing on each mandate. A deal that looks strong on paper can still hurt take-home pay if legal review, valuation work, or handoff support drags out billing and collection. Use one simple rule: every higher-complexity project must show a clear fee premium before it starts.

5

Overhead, Reserves, and Risk Management

Overhead and reserve discipline

Fixed overhead is $265k per month before payroll, covering office rent, professional liability insurance, technology subscriptions, professional services, and communications. The file also lists $318k per year, so the monthly run rate is the cash control number. At that level, overhead hits profit before owner pay, so lean spending directly lifts take-home.

Payroll is modeled to rise from $415k in Year 1 to $153M in Year 5, so staffing and contractor spend need tight limits. Hold back cash for slow collections, subcontractor buffers, travel, and transaction delays. No reserve, no draw.

Track cash before owner draw

Watch cash on hand, days sales outstanding (how long clients take to pay), and the reserve balance before any owner distribution. If a client pays late or a deal closes later than planned, keep cash inside the business until payroll and third-party costs are covered. That keeps profit from turning into a cash squeeze.

Set a monthly floor for fixed costs plus the next round of subcontractor fees and travel. Then pay the owner only from cash above that floor. If overhead stays lean and reserves stay funded, more profit can safely become owner take-home.

- Track overhead by cost line.

- Reserve for delayed collections.

- Hold cash for subcontractors.

- Delay draw until floor is met.

6

Compare lean, base, and high-performance owner-income scenarios

Owner income scenarios

Owner income stays salary-led in each case, but client count, pricing, and hiring pace decide whether cash stays tight or has room for more.

| Scenario | Lean CaseLean Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the lower-income path built from a Year 1-like start with slower client flow. | This is the modeled middle path built from a Year 3-like operating pace. | This is the stronger-income path if the firm lands more clients and keeps execution tight. |

| Typical setup | About 12 clients, roughly $325,000 revenue, an 88.5% service gross margin, a $200,000 planned owner salary, and no distribution. | About 23 clients, roughly $830,000 revenue, a 90.0% service gross margin, a $200,000 planned owner salary, and no distribution. | About 40 clients, roughly $1.84M revenue, a 91.5% service gross margin, a $200,000 planned owner salary, and no modeled distribution. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $200,000 salary onlyLean Case | $200,000 salary onlyBase Case | $200,000 salary onlyHigh Case |

| Best fit | Use this to stress-test funding risk, slow sales cycles, and early-stage cash pressure. | Use this as the core planning case for steady delivery, hiring, and cash discipline. | Use this to test upside if demand stays strong and hiring does not outrun profit. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Business Transition Services Porter's Five Forces Analysis

- Business Transition Services BCG Matrix

- Business Transition Services Business Model Canvas

- What Five KPIs Should InsertBusinessName Track?

- Business Transition Services Business Plan Template in Pre-Written Word

- How Increase Profits Business Transition Services?

- What Are Operating Costs For Business Transition Services?

- Business Transition Services Startup Costs: Plan For $573K

- Business Transition Services Financial Model Template in Excel

- Start a Business Transition Consulting Firm in 8 to 16 Weeks

- How To Write A Business Plan For Business Transition Services?

- Business Transition Services Marketing Mix

- Business Transition Services Marketing Plan

- Business Transition Services Business Proposal

- Business Transition Services PESTEL Analysis

- Business Transition Services Pitch Deck Example Editable PPTX

- Business Transition Services Business SWOT Analysis

- Business Transition Services Value Proposition Canvas

Frequently Asked Questions

Under the provided assumptions, it does not generate modeled profit distributions in the first five years Revenue grows from about $325k to $184M, and service gross margin improves from 885% to 915% Still, payroll reaches $153M and fixed overhead is $318k per year, so extra owner distributions are not supported