Owner income$95k

Owner income$95kHow Much Can a Tree Care Service Owner Make With $95K Pay?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$95k  Net margin-669% to 441%

Net margin-669% to 441% Revenue for target pay$144k

Revenue for target pay$144k Business difficultyHard

Business difficultyHard

You’re trying to separate real owner take-home from top-line sales In this five-year US tree care service model, the owner/lead arborist wage is $95,000 per year, while EBITDA moves from -$195,000 in Year 1 to $485,000 in Year 3 and $1082 million in Year 4 This view covers revenue, margins, payroll, equipment, insurance, overhead, reserves, and the owner’s role

Owner income$95kNet margin-669% to 441%Revenue for target pay$144kBusiness difficultyHardWant to test your own tree service income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

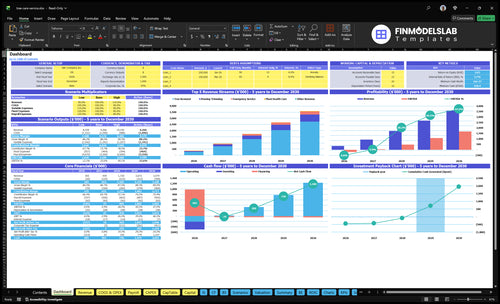

How does Tree Care Service owner income look in the model?

This dashboard shows revenue, margin, costs, reserves, and owner take-home assumptions—open the Tree Care Service Financial Model Template.

Owner-income model highlights

- Scenario tabs test pricing

- EBITDA by year

- $95k owner wage

- $284k initial capex

- $420k minimum cash

- Month 18 break-even

- 40-month payback

- Crew growth and reserves

What costs reduce tree service owner income?

Tree service owner income gets cut first by payroll, then by disposal, materials, fuel, repairs, insurance, rent, marketing, and capex. For startup cost context, see What Is The Estimated Cost To Open And Launch Your Tree Care Service Business? Year 1 payroll is $292,000, fixed overhead is $7,730 per month, marketing is $20,000, and variable operating costs run at 28% of revenue.

Recurring cost drains

- Payroll is the biggest cash drain

- Disposal and fuel hit every job

- Repairs and insurance lower margin

- Rent and marketing stay fixed

Capex and risk leaks

- Initial capex totals $284,000

- Trucks and chipper tie up cash

- Stump grinder and tools add burden

- Downtime and debt service cut distributions

Does a tree service owner make more working in the field or managing crews?

If you’re running a Tree Care Service, the owner usually makes more early by staying in the field, because the model pays the owner/lead arborist $95,000 and skilled labor is expensive. Managing crews can grow revenue, but payroll also rises from $292,000 in Year 1 to $639,500 in Year 4, so take-home only improves if scheduling, safety, estimates, and cash reserves keep pace. The quick rule: field work protects margin early, while crew management wins later only when the system is tight.

Working in the field

- $95,000 owner pay is modeled.

- Protects margin in early years.

- Skilled labor is costly.

- Best when jobs need hands-on control.

Managing crews

- $75,000 certified arborist salary is modeled.

- Capacity grows with more crews.

- Payroll reaches $639,500 by Year 4.

- Works only with strong operations.

How much revenue does a tree service need to make the owner $100k?

For Tree Care Service, the scenario points to about $829,000 in Year 2 revenue to make a $100,000 owner target plausible, because the modeled wage is $95,000 and Year 2 has $55,000 EBITDA, or earnings before interest, taxes, depreciation, and amortization. Year 1 revenue of $291,000 does not support extra pay with -$195,000 EBITDA; track service quality and repeat demand with How Is Tree Care Service Measuring Success In Customer Satisfaction? before raising owner draws.

Revenue target

- Year 1: $291,000 revenue

- Year 1: -$195,000 EBITDA

- Year 2: $829,000 revenue

- Year 3: $156 million revenue

Owner cash test

- Modeled wage: $95,000

- Extra target gap: $5,000

- Year 2 EBITDA margin: 6.6%

- Year 1 EBITDA margin: -67.0%

Want the six income drivers that matter most?

1

18 moCrew Utilization

More billable days spread the $7.7K monthly fixed overhead across more work, and the model does not break even until month 18.

2

$95-$250Job Mix

Mixing $95 plant care with $250 emergency work changes the blended hourly rate and the cash each crew day brings in.

3

4.5-12 FTECrew Structure

The team scales from 4.5 FTE in Year 1 to 12 FTE by Year 5, so each labor hour has to stay productive or wage drag hits take-home.

4

$284KEquipment Load

About $284K of trucks, chipper, grinder, tools, and setup spend sits behind delivery, so downtime or repairs hurt both cash and job capacity.

5

28%Risk Control

With Year 1 variable costs at 28%, insurance, safety, claims, and licensing slips show up fast in margin.

6

$300-$220Lead Conversion

CAC falls from $300 in Year 1 to $220 in Year 5, so better lead flow, closes, and repeat accounts lower the cost of each job.

Tree Care Service Core Six Income Drivers

Crew utilization and billable production days

Crew Utilization

Crew utilization drives revenue before fixed costs move. The share of paid crew days that become billable work matters because $7,730 per month of fixed overhead still runs before wages and marketing, and idle days still absorb payroll, insurance, yard rent, software, vehicle leases, and dispatch.

Here’s the quick math: on a 30-day month, that is about $257 per day in fixed overhead. If weather, cancellations, routing gaps, or seasonal demand cut billable production days, the owner still funds the same base cost, so cash flow and take-home pay shrink fast.

Track Billable Days

Measure billable days, completed jobs, estimate backlog, and cancellation rate every week. Those inputs show whether the schedule is full enough to cover fixed cost and protect owner pay.

- Billable days per crew

- Completed jobs per week

- Estimate backlog for next month

- Cancellation rate by source

If backlog slips or cancellations rise, tighten dispatch, confirm jobs earlier, and keep crews on the highest-value routes first. More paid production days means better gross profit and more cash left for the owner’s draw.

1

Average job value and service mix

Average Job Value and Service Mix

Average job value swings hard by service line, so revenue quality matters as much as volume. Year 1 removal is about $1,920 per job at 12 hours × $160, while emergency work is $1,320 at 6 hours × $220. Pruning and trimming is only about $263 at 25 hours × $105, and plant health care is $95 for 1 hour × $95.

High-ticket removal can lift cash, but it can also drag margin if disposal, safety risk, equipment wear, and insurance rise with the job mix. Here’s the quick math: revenue = jobs × hours × rate, but owner pay depends on what’s left after labor, overhead, and risk. A mix shift toward 60% pruning and trimming by Year 3 can stabilize volume, but it may cap average ticket if pricing and crew speed stay weak.

Track Mix Before You Chase More Jobs

Measure job count, hours, rate, disposal cost, overtime, and rework by service line. If a removal job bills high but leaves little gross profit after truck time, dump fees, and risk costs, it may pay less than a faster prune route. The owner should watch gross margin per job and gross margin per crew day, not just sales.

Use the service mix to plan staffing and cash flow. Plant health care can fill gaps with low ticket value, while emergency work can lift revenue but strain scheduling. Keep a simple weekly mix report: removal, emergency, pruning and trimming, plant health care. Then price each line so the blended margin can support payroll, insurance, and owner draw.

- Track revenue per service line

- Compare margin after disposal

- Price risk-heavy jobs higher

- Forecast mix changes by month

2

Labor productivity and crew structure

Labor Productivity

Labor is the biggest controllable margin lever. Year 1 payroll is $292,000, or about $24,333 per month, and it rises to $541,000 in Year 3, about $45,083 per month. If crews finish jobs faster without overtime, callbacks, or safety shortcuts, gross profit improves and more cash stays available for owner pay.

This driver includes certified arborists, ground crew, dispatch, and sales capacity. The risk is simple: cutting labor too hard can slow jobs, hurt safety, and lower close rate. The owner’s income depends on getting more billable output from each labor hour, not just shrinking payroll.

Track Crew Output

Measure revenue per labor hour, jobs completed per crew day, overtime, subcontractor use, and rework. Here’s the quick math: if payroll rises but output does not, margin gets squeezed fast. Faster crews with fewer callbacks usually raise gross profit more than a blunt headcount cut.

- Track billable hours by crew.

- Watch overtime every week.

- Log rework and callbacks.

- Compare crew-day output monthly.

Use crew mix and dispatch to match the job, then keep the schedule full enough to avoid idle labor. If a job needs more skill, send the right lead and support crew; if not, move lower-cost labor in behind them. That protects safety, speed, and take-home profit.

3

Equipment costs, financing, repairs, and downtime

Equipment, Repairs, and Downtime

Equipment raises capacity, but it also locks up cash and adds risk. Here, initial capex is $284,000, including $130,000 for two heavy-duty trucks, $50,000 for a commercial wood chipper, $35,000 for a stump grinder, and $18,000 for chainsaws and power tools. In Year 1, maintenance and consumables run at 6% of revenue, so cash needs stay tied to sales.

The real hit is downtime: crews sit idle while payroll keeps running, so one broken truck or chipper cuts revenue and still burns labor. That lowers gross margin, delays owner pay, and makes distributions unsafe until repair reserves are funded. The key test is whether uptime is high enough to support billed work without forcing overtime or emergency rentals.

Protect cash with repair reserves

Build a reserve tied to revenue and downtime, not hope. Track equipment hours, repair spend, idle days, and lost billable days by asset so you can see which machine is draining profit. If a truck or chipper goes down, pause owner distributions until you know the repair or replacement cash gap.

- Track billable days lost per asset.

- Compare repairs to 6% of revenue.

- Keep cash for rentals or replacement.

Then forecast payroll, maintenance, and loan or lease payments together. If downtime rises, the owner’s take-home falls twice: less revenue and the same crew cost. One missed production day can erase several good jobs, so the reserve needs to sit ahead of distributions, not after them.

4

Insurance, safety, claims, and risk

Insurance, Safety, and Claims Risk

Tree care is a high-risk business, so insurance and claims can change owner pay fast. The model uses $1,200 per month for business insurance and licensing before any claim-driven increase. That cost hits cash flow whether the crew is busy or not, and workers comp, general liability, and employee classification can all move the monthly take-home number.

Here’s the key point: more removal and emergency work usually means more risk than routine pruning. If a claim, reclassification, or coverage change raises premiums, the same revenue can leave less profit for the owner. Safety training and claims history are not side items here; they shape the draw the owner can safely pay.

Track Risk Before It Hits Profit

Measure the inputs that drive this cost: job mix, incident count, workers comp class, claim frequency, and premium changes. A simple forecast should separate pruning from removal and emergency calls, because the risk profile is not the same. One claim can erase several months of margin.

Use a weekly safety log, pre-job checklists, and crew training records so the insurance file is clean. Track how much revenue comes from higher-risk work, then keep a reserve for deductibles and premium jumps. If claims history worsens, owner pay should be adjusted before cash gets tight.

5

Pricing, lead flow, and recurring accounts

Profitable lead flow

Lead flow only helps income when it turns into booked work at the right price. Here, marketing spend rises from $20,000 in Year 1 to $50,000 in Year 3, while CAC, or customer acquisition cost, improves from $300 to $250. That implies about 67 customers in Year 1 and 200 in Year 3 if those numbers hold.

The real risk is chasing volume with discounts. Local search, referrals, and commercial maintenance accounts can keep crews booked with steadier margins, but missed calls and weak estimates still leak cash. If booked revenue rises while job margin falls, owner income can stall even with a fuller calendar.

Track close rate and repeat work

Measure estimate close rate, booked revenue, job margin, repeat accounts, and missed calls every week. Those five numbers show whether lead spend is creating profit or just noise. Here’s the quick math: if CAC drops from $300 to $250, the business gets a 17% better acquisition cost, but only if close rate holds.

Use discounts only when they protect utilization without crushing margin. Commercial maintenance accounts are valuable because they repeat, smooth cash flow, and make owner pay more predictable. If pricing gets cut just to fill the schedule, the crew may look busy while take-home profit gets smaller.

- Track source by channel

- Count missed calls daily

- Review close rate weekly

- Separate repeat from one-time work

- Test price before discounting

6

Compare low, base, and high owner income scenarios

Owner income scenarios

Owner income shifts with ramp, crew load, and job mix. Year 1 is loss making, Year 2 gets near break-even, and Years 3 to 4 open room for real draws.

| Scenario | Low CaseRamp-up | Base CaseBreak-even | High CaseScale |

|---|---|---|---|

| Launch model | This is the ramp-up case, where the business still posts a Year 1 loss. | This is the modeled break-even case, where Year 2 turns slightly positive. | This is the scale case, where growth lifts EBITDA into six figures and beyond. |

| Typical setup | It runs with about $291,000 implied revenue, -$195,000 EBITDA, $95,000 owner wage, a 28% variable cost load, and roughly $292,000 payroll. | It uses about $829,000 implied revenue, $55,000 EBITDA, and the same $95,000 owner wage as the model hits Month 18 break-even. | It reflects Years 3 to 4 scale, with EBITDA moving from $485,000 to $1,082,000 before reserves, debt, taxes, and reinvestment. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Salary-only rampCash strain | Near break-even payMonth 18 pivot | $485,000 - $1,082,000Growth upside |

| Best fit | Use this to test the downside if demand builds slowly and payroll stays heavy. | Use this as the core operating case for planning cash, hiring, and owner pay. | Use this to test upside when the crew is busy, marketing is efficient, and jobs fill the schedule. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Tree Care Service Porter's Five Forces Analysis

- Tree Care Service BCG Matrix

- Tree Care Service Business Model Canvas

- 7 Critical KPIs to Measure Tree Care Service Profitability

- Tree Care Service Business Plan Template in Pre-Written Word

- How to Boost Tree Care Service Profitability with 7 Key Strategies

- Running Costs for a Tree Care Service: What to Budget Monthly?

- How Much It Costs To Start A Tree Care Service: $420K Plan

- Tree Care Service Financial Model Template in Excel

- How To Start A Tree Care Service In 6–12 Weeks And Book First Jobs

- How to Write a Tree Care Service Business Plan in 7 Steps

- Tree Care Service Marketing Mix

- Tree Care Service Marketing Plan

- Tree Care Service Business Proposal

- Tree Care Service PESTEL Analysis

- Tree Care Service Pitch Deck Example Editable PPTX

- Tree Care Service Business SWOT Analysis

- Tree Care Service Value Proposition Canvas

Frequently Asked Questions

In this model, the owner/lead arborist wage is $95,000 per year, or about $7,917 per month, before personal taxes Extra distributions depend on profit and cash EBITDA is -$195,000 in Year 1, $55,000 in Year 2, and $485,000 in Year 3, before debt service, taxes, reserves, and reinvestment