Owner incomeY1 $405K to Y5 $5.0M

Owner incomeY1 $405K to Y5 $5.0MHow Much Turnaround Consulting Owners Make: $405K Year 1 Case

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner incomeY1 $405K to Y5 $5.0M  Net margin73% to 75%

Net margin73% to 75% Revenue for target payY1 $918K

Revenue for target payY1 $918K Business difficultyHard

Business difficultyHard

A turnaround management consulting owner can make meaningful income, but the cash is not automatic In this researched model, the firm pays a $185K managing partner salary and produces EBITDA of $220K in Year 1, $1754M in Year 3, and $4816M in Year 5 If one owner took salary plus all EBITDA before taxes, reserves, debt service, and reinvestment, pre-tax take-home would be about $405K, $1939M, and $5001M The model breaks even in Month 6, but it also needs $764K minimum cash, so collections and reserves matter

Owner incomeY1 $405K to Y5 $5.0MNet margin73% to 75%Revenue for target payY1 $918KBusiness difficultyHardWant to test your owner take-home?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in a turnaround consulting model?

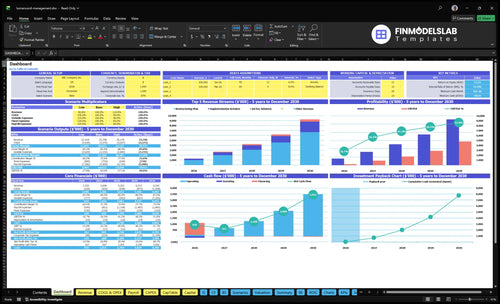

The Turnaround Management Consulting Financial Model Template dashboard shows revenue, EBITDA, owner income, cash, break-even, payback, and IRR—open it.

Owner-income model highlights

- Owner salary: $185K

- Margin range: 73% to 75%

- Break-even: Month 6

- Test: retainers and staffing

What profit margin does a turnaround management consulting firm make?

Turnaround Management Consulting can keep a strong gross margin because Year 1 delivery costs are 27% of revenue, leaving 73% gross margin, and Year 5 delivery costs ease to 25%, or 75% gross margin. EBITDA margin is a separate view and rises from 167% in Year 1 to 518% in Year 5 as revenue grows faster than fixed overhead and payroll. For the cost base behind that, see What Are Operating Costs For Turnaround Management Consulting?

Gross margin

- Year 1: 27% delivery costs, 73% gross margin

- 10% referral commissions

- 7% travel, 5% legal support

- 5% project bonuses

Cash to owner

- Year 5: delivery costs fall to 25%

- EBITDA margin: 167% to 518%

- Owner salary is separate at $185K per year

- Distributions depend on reserves and taxes

Can a solo turnaround management consultant make a strong owner income?

Yes, a solo Turnaround Management Consulting consultant can earn a strong owner income, but it’s capped by billable days and referral flow. The Year 1 model shows $132M revenue with a team, not a pure solo shop, and rates of $350/hour for restructuring and $400/hour for ad-hoc advisory support strong service economics.

Solo upside

- Price restructuring at $350/hour

- Price advisory at $400/hour

- Keep payroll light at launch

- Protect cash with retainers

Main cap

- Sell, diagnose, deliver, collect

- Referral gaps create income swings

- Team model adds $290K payroll

- Capacity rises with three hires

How much revenue does a turnaround consulting firm need to pay the owner?

Turnaround Management Consulting needs about $918K of annual revenue to pay the owner $185K and cover Year 1 costs, assuming a 73% gross margin after delivery costs. If margin slips to 65%, the revenue needed rises to about $1.03M. The Year 1 model shows $1.32M in revenue, but minimum cash still hits $764K in Month 6, so collections timing matters.

Cost base

- $185K owner pay

- $290K non-owner payroll

- $150K overhead

- $45K marketing

Cash watch

- $670K cost before reserves

- $918K revenue at 73% margin

- $1.03M revenue at 65% margin

- $764K minimum cash in Month 6

Want to see the main income drivers?

1

$350-$480Pricing Power

Higher hourly rates and more billable hours per case lift revenue fastest, since plans run from 10 to 60 hours by service.

2

$4.5K CACReferral Quality

A tighter referral pipeline keeps the first-year marketing budget from getting eaten by acquisition costs.

3

45-55 hrsBillable Use

Moving active-customer hours from 45 to 55 a month raises revenue without the same jump in fixed cost.

4

$475K-$1.44MStaffing Leverage

Payroll scales fast, so each hire has to bring in more billable work than it costs.

5

73%-75%Gross Margin

Keeping delivery margin in range protects EBITDA as revenue grows and supports owner take-home.

6

$764K minCash Control

Cash runs to a $764K low point before Month 6 break-even, so collections timing directly affects owner draw.

Turnaround Management Consulting Core Six Income Drivers

Engagement Value And Pricing

Engagement Pricing and Scope

Each accepted engagement uses scarce senior time, so pricing goes straight to owner income. At Year 1, a restructuring plan at 60 hours x $350 generates $21K; an implementation retainer at 40 hours x $275 generates $11K; ad-hoc advisory at 10 hours x $400 generates $4K. One underpriced distressed client can crowd out better work.

By Year 5, the same scopes rise to $425, $330, and $480, or $25.5K, $13.2K, and $4.8K. Longer retainers lift revenue per client, but scope creep and late payment can cut realizable revenue fast. Success fees should hit the books only when they are earned and collectible.

Tighten Scope and Collections

Track hours sold, realized rate, and cash collected for each engagement type. The key question is simple: does the file pay for senior time before overhead? If not, the owner is funding the client. Use written scope, milestone billing, and stop-work rules to keep delivery from leaking past the fee.

- Price by scope, not guesswork.

- Bill milestones up front.

- Approve change orders in writing.

- Book success fees after cash clears.

Watch payment timing closely, because distressed clients often delay approvals or dispute work. A strong fee means little if collections slip. The cleaner the scope and the faster the cash, the more income stays available for owner pay instead of sitting in receivables.

1

Referral Pipeline Quality

Qualified Referral Pipeline

Referral quality drives owner income because senior consultants only earn when distressed-business leads turn into billable work. A pipeline built around lenders, bankruptcy attorneys, CPAs, private equity operating partners, investors, and business owners can keep utilization high. With marketing spend rising from $45K in Year 1 to $140K in Year 5, the real test is whether those leads close fast enough to keep payroll productive and collections clean.

Track referral quality, not just lead count

Track source mix, lead-to-engagement rate, and CAC (customer acquisition cost) because Year 5 CAC still needs to improve only from $4,500 to $3,500. Better referrals cut sales waste, reduce idle payroll, and smooth owner draws. Weak referrals do the opposite: more nonbillable time, lower utilization, and more payment problems when distressed clients stall or dispute scope.

- Measure conversion by source.

- Separate qualified from weak leads.

- Track days to first paid work.

- Watch collections by referral source.

2

Billable Utilization

Billable Utilization

Utilization is billable hours ÷ available hours, after sales, diagnostics, travel, client calls, and admin. In this model, average billable hours per active customer rise from 45 per month in Year 1 to 55 in Year 5, a 22% increase in paid time per client. That can lift revenue without the same jump in fixed cost, but only if delivery quality stays tight.

Service mix drives the math. A restructuring plan uses 60 hours, an implementation retainer uses 40 to 50 hours, and ad-hoc advisory uses 10 to 15 hours. If too many days stay nonbillable, owner income falls even when demand looks strong. If the owner overbooks, burnout, rework, and missed deadlines can shrink take-home pay fast.

Protect Billable Hours

Track active customers, billable hours per customer, and nonbillable time by week. Keep a simple time log for sales, diagnostics, travel, and admin, then compare it with paid work. The goal is simple: keep more of the week inside revenue-producing time, but leave enough room for prep and client contact so the work still lands well.

- Log every nonbillable hour daily.

- Split hours by service type.

- Watch week-by-week overbooking.

- Price scope creep before it starts.

A 60-hour restructuring job and a 10 to 15 hour advisory call use capacity very differently, so mix matters. If billable time rises but response times slip, cash may improve short term while owner pay gets squeezed by rework, churn, and quality risk.

3

Staffing Leverage

Staffing Leverage

Staffing leverage means adding consultants and analysts so more hours become billable work without the owner doing all the delivery. In this model, senior turnaround consultants rise from 1 FTE in Year 1 to 5 FTE in Year 5, and financial analysts from 1 FTE to 4 FTE. If utilization stays high, owner income can scale; if hiring runs ahead of demand, idle payroll cuts margin fast.

The key inputs are billable hours, utilization (paid hours as a share of available hours), delivery payroll, supervision time, and rework risk. One clean rule: more staff only helps when each added person is tied to booked client work. Here’s the quick math: a bigger team lifts revenue capacity, but every nonbillable day still costs cash.

Track Utilization Before You Hire

Watch billable hours by role, client, and month. If senior consultants or analysts are below target, pause hiring and fix pipeline quality first. For this business, the owner needs enough revenue per FTE to cover supervision, client management, and rework before paying themselves more.

- Track billable hours weekly.

- Separate billable and nonbillable work.

- Test hiring against booked demand.

- Price for supervision time.

- Cut weak-fit leads fast.

4

Delivery Gross Margin

Delivery Gross Margin

Gross margin is what stays after direct delivery costs, before overhead and owner pay. In Year 1, those costs equal 27% of revenue, so gross margin is 73%. Here’s the quick math: on $100,000 of revenue, about $73,000 is left to fund the team, admin, and the owner.

The cost mix matters: 10% referral commissions, 7% travel, 5% contracted legal support, and 5% project bonuses. By Year 5, gross margin improves to 75% as referral, travel, and legal support rates fall, even though bonuses rise to 9%. High billing rates still do not guarantee owner income if direct costs eat the spread.

Protect the Spread

Track gross margin by client, not just by month. Use the formula revenue minus direct delivery costs, then watch each cost line: referral fees, travel, legal support, and project bonuses. If one engagement runs hot on travel or outside help, it can wipe out the gain from a strong rate.

Set targets before work starts. For each deal, model expected revenue, referral commission, travel days, legal spend, and bonus rules. Then compare budget to actuals at closeout. If travel or specialist support rises, cut scope or reprice fast, because every 1 point of margin matters more as revenue scales.

- Track margin by engagement.

- Cap travel before kickoff.

- Price referral fees into bids.

- Link bonuses to collected revenue.

5

Collections And Reserve Discipline

Collections And Reserve Discipline

In turnaround consulting, cash timing matters more than booked profit. Distressed clients may pay late, dispute scope, or stop work midstream, so EBITDA can look healthy while cash for owner draws is tight. Here, the model still needs $764K minimum cash in Month 6 even though breakeven also lands in Month 6, so weak collections can trap profit inside the firm.

The inputs are simple: billed hours, retainer size, milestone timing, days sales outstanding, and the reserve target. Strong collections convert earnings into usable cash; weak ones force the owner to hold back draws to cover payroll, taxes, and rework. One bad client can create a cash gap even when the P&L says you are even.

Track cash, not just revenue

Use upfront retainers, milestone billing, aged receivables reviews, and stop-work rules. Aged receivables should be reviewed weekly, with clear action on anything over 30 days. The key test is simple: if cash on hand falls below the reserve, the owner should pause new work or push collection before taking draws.

Track DSO days sales outstanding, unbilled work, collected cash, and reserve balance by client. Build forecasts from expected billings and collection timing, not just hours sold. If a client delays payment past the billing milestone, the reserve protects payroll and tax payments, but it also means the owner must wait to pay themselves.

- Review receivables every week.

- Invoice at milestones, not completion.

- Stop work when terms are broken.

- Keep the reserve above $764K.

6

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Owner income rises as referral flow, billable hours, and pricing scale. The spread is driven by utilization, collections, and staffing mix.

| Scenario | Low CaseDifficulty risk | Base CaseUtilization risk | High CaseCollections risk |

|---|---|---|---|

| Launch model | A Year 1 launch keeps the firm founder-led and cash-light, with income tracking the first-year run rate. | A Year 3 model assumes a staffed boutique with repeat referrals and a steadier owner draw. | A Year 5 model assumes a scaled advisory team with more active clients and higher hourly pricing. |

| Typical setup | Revenue is about $1.32M, gross margin is 73%, EBITDA is $220k, and the owner takes a $185k salary while the firm reaches Month 6 breakeven. | Revenue is about $4.252M, gross margin is 74%, EBITDA is $1.754M, and the owner salary stays at $185k as the team handles more active customers. | Revenue is about $9.295M, gross margin is 75%, EBITDA is $4.816M, and the $185k owner salary sits inside a larger operating base. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $405kOwner-led launch | $1.94MStaffed boutique | $5.00MScaled advisory team |

| Best fit | Use this to stress-test a lean boutique launch with slower deal flow and tighter cash. | Use this as the core planning case for a growing advisory firm with repeat work. | Use this to test upside if the firm builds a bigger team and keeps collections tight. |

Planning note: These ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions; the model also shows a $764k minimum cash need, so reserve cash first.

Related Products

- Turnaround Management Consulting Porter's Five Forces Analysis

- Turnaround Management Consulting BCG Matrix

- Turnaround Management Consulting Business Model Canvas

- How Increase Turnaround Management Consulting Profitability?

- Turnaround Management Consulting Business Plan Template in Pre-Written Word

- How Increase Profitability For Turnaround Management Consulting?

- What Are Operating Costs For Turnaround Management Consulting?

- Turnaround Consulting Startup Costs: $764k Base-Case Funding

- Turnaround Management Consulting Financial Model Template in Excel

- How to Open a Turnaround Management Consulting Firm in 6-12 Weeks

- How To Write A Turnaround Management Consulting Business Plan?

- Turnaround Management Consulting Marketing Mix

- Turnaround Management Consulting Marketing Plan

- Turnaround Management Consulting Business Proposal

- Turnaround Management Consulting PESTEL Analysis

- Turnaround Management Consulting Pitch Deck Example Editable PPTX

- Turnaround Management Consulting Business SWOT Analysis

- Turnaround Management Consulting Value Proposition Canvas

Frequently Asked Questions

In this model, the owner salary is $185K per year If one owner also took all EBITDA before taxes, reserves, debt service, and reinvestment, pre-tax cash would be about $405K in Year 1, $1939M in Year 3, and $5001M in Year 5 Those are planning assumptions, not guaranteed distributions