Owner income$150k

Owner income$150kHow Much Underwater Drone Business Owners Make: $150K Pay vs Profit

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$150k  Net margin83%-89%

Net margin83%-89% Revenue for target pay$169k

Revenue for target pay$169k Business difficultyHard

Business difficultyHard

An underwater drone exploration business owner can model $150,000 in annual owner pay before personal taxes, but the researched base case does not support extra distributions Revenue rises from about $86,000 in the first year to about $102 million in Year 5 Year 5 still shows about negative $68,000 EBITDA after 11% direct costs, 6% sales and software costs, $74,400 fixed overhead, and $840,000 payroll These are planning assumptions, not guaranteed earnings

Owner income$150kNet margin83%-89%Revenue for target pay$169kBusiness difficultyHardWant to test your owner income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. It excludes personal taxes and financing unless you enter debt service.

How much can the owner take home in the model?

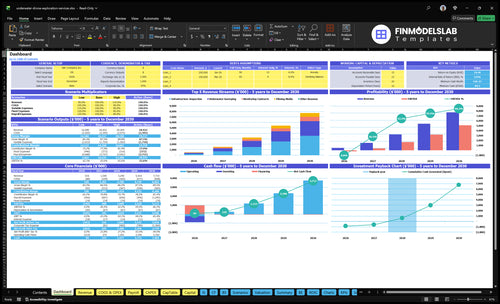

The dashboard covers revenue assumptions, service mix, billable hours, hourly pricing, equipment costs, operating expenses, payroll, owner compensation, and cash reserves in the Underwater Drone Exploration Financial Model Template. Charts show revenue rising from about $86,000 to $102 million, gross margin from 83% to 89%, payroll from $395,000 to $840,000, and EBITDA from about negative $408,000 to negative $68,000. Use it as a planning aid, not the main promise. Open the model.

Owner-income model highlights

- Owner take-home shown

- Revenue and margin charts

- Scenario outputs update fast

What should underwater drone services charge?

Underwater Drone Exploration should price by deliverable, not just time: $250-$290/hour for infrastructure inspection, $275-$315 for underwater surveying, $350-$390 for filming, and $220-$260 for monitoring contracts. Here’s the quick math: model average revenue per customer or project equivalent from $4,301 to $7,222, and use hourly, half-day, day-rate, project, mobilization, reporting, and recurring pricing only when they protect margin after travel, data work, and risk.

Core rates

- $250-$290/hour for inspection

- $275-$315/hour for surveying

- $350-$390/hour for filming

- $220-$260/hour for monitoring

Margin rules

- Charge mobilization separately

- Bill reporting and data work

- Use recurring fees for monitoring

- Protect margin after travel and risk

How many underwater drone jobs do you need to make a living?

You need about 13 billable underwater drone jobs per month at Year 5 economics to make a living from Underwater Drone Exploration; see What Is The Current Growth Trend For Underwater Drone Exploration? for the market context.

Quick Math

- $7,222 average project revenue

- 83% contribution margin

- $914,400 annual payroll base

- About 13 jobs/month break-even target

Operator Reality

- Covers $150,000 owner pay

- Covers payroll, overhead, variable costs

- Modeled Year 5 volume: 118/month

- Owner-operated work lowers payroll pressure

What expenses reduce underwater drone service margins?

If you’re pricing Underwater Drone Exploration, the biggest margin drag is not one line item but the mix of direct job costs, fixed overhead, and reserve needs; see What Is The Estimated Cost To Open And Launch Your Underwater Drone Exploration Business? for the launch spend. Here’s the quick math: operational and mobilization costs drop from 12% of revenue to 8%, maintenance drops from 5% to 3%, and software plus sales costs fall from 12% combined to 6%.

Direct job costs

- 8% of revenue for mobilization

- 3% for equipment maintenance

- 6% for software and sales

- 12% to 8% is the key cut

Fixed costs and launch burn

- $74,400 fixed overhead yearly

- $395,000 to $840,000 payroll range

- $500,000 listed startup capex total

- $250,000 ROV system upfront

Want to see the six income drivers?

1

13/moBillable Utilization

At about 13 monthly jobs in Year 5, you hit break-even against $74.4K of fixed overhead, so every extra job adds to owner take-home faster.

2

$4.3K-$7.2KPricing Mix

Average project revenue in that range, with 83%-89% gross margin, is the cleanest lever for lifting profit per job.

3

15%-35%Contract Mix

Growing monitoring contracts from 15% to 35% raises repeat revenue and cuts idle weeks that drain cash.

4

3%-5%Maintenance Reserves

Holding equipment maintenance near 3%-5% keeps more cash in profit and reserves instead of repair spend.

5

8%-12%Mobilization Costs

Travel and mobilization run at 8%-12% of revenue, so tight field setup protects margin for owner take-home.

6

$395K-$840KLabor Workflow

Payroll rises from $395K to $840K as staff scale, so the owner's role and hiring pace decide how much profit is left before taxes and reserves.

Underwater Drone Exploration Core Six Income Drivers

Billable Utilization

Billable Utilization

Billable utilization is the share of pilot, travel, setup, and reporting time that turns into billed inspection, survey, filming, or monitoring work. With $74,400 of fixed overhead and payroll, more booked jobs spread cost over more revenue, so owner pay improves only when the calendar stays full. One clean line: idle days are expensive.

The model rises from 20 customer or project equivalents in Year 1 to about 141 in Year 5. Year 5 needs about 153 per year, or 13 per month, to break even with $150,000 owner pay. Weather, site access, travel time, and reporting time all reduce true utilization, so booked work is not the same as billable work.

Track Billable Hours, Not Just Jobs

Measure booked hours, billed hours, and non-billable time by job type. If reporting or mobilization keeps rising, utilization drops even when revenue looks fine. Compare monthly project equivalents with the 13 per month break-even pace in Year 5. Fewer billable jobs means each job must carry more overhead.

- Log weather delays separately

- Split travel from field time

- Track report hours per job

- Quote access constraints up front

- Review billable ratio each month

Price and schedule for lost time, not just field hours. Use weather windows, site access, travel distance, and report complexity when quoting. If a site adds setup or documentation, that time needs to be billed or the owner’s draw gets squeezed.

1

Pricing And Package Mix

Pricing And Package Mix

When the job is sold as a deliverable, not just field time, revenue per deployment jumps. Here’s the quick math: average project revenue rises from $4,301 to $7,222, a lift of $2,921 per project. The highest rates sit around $350 to $390 for filming, $275 to $315 for surveying, $250 to $290 for infrastructure inspection, and $220 to $260 for monitoring.

This driver includes the mix of project types, reporting depth, sonar support, data quality, and mobilization charges. If those items are underpriced, gross margin drops even when crew hours stay full. One-line test: if the quote does not pay for risk and reporting, it is too cheap.

Price the Output, Not Just the Dive Time

Track average revenue per deployment by package, not just total bookings. Watch which jobs include sonar-supported work, formal reporting, and long mobilization, then price those as separate value items. If filming and surveying quotes cluster near the top of the range, owner pay has more room because fixed overhead and payroll are spread across higher revenue.

- Track revenue per deployment weekly.

- Split quotes by service type.

- Add fees for reporting and risk.

- Charge mobilization separately.

- Test package mix by month.

2

Customer And Contract Mix

Customer and contract mix

Owner income improves when more work comes from repeat commercial and monitoring accounts. In the modeled mix, monitoring rises from 15% to 35%, inspection starts at 40% and later settles at 35%, and filming stays at 10% after the early ramp-up. That shift can smooth utilization and cash flow, but the sales cycle often gets longer before revenue turns into pay.

The key inputs are contract mix, repeat rate, and delivery effort per job. If compliance reporting adds hours, gross margin can fall even when revenue looks steadier. One clean rule: more recurring work helps owner pay only if pricing covers the extra documentation and review time.

Track mix by contract type

Measure revenue share, days to close, and gross margin by service line. Keep separate targets for monitoring, inspection, and filming, then price the reporting work instead of burying it in the field rate. If monitoring grows from 15% to 35%, forecast slower cash conversion at first and watch whether repeat accounts fill the schedule enough to support drawings.

- Track mix by invoice line.

- Price compliance hours separately.

- Watch margin by contract type.

Use the mix to plan staffing and cash. Recurring accounts help smooth utilization, but they can also raise delivery cost when standards are strict. If inspection stays near 35%–40% and filming holds at 10%, the business needs enough repeat volume to cover reporting, review, and idle time between projects.

3

Equipment Costs And Reserves

Equipment Reserve Load

Equipment spend hits owner income before the first project closes. The stated startup capex totals $500,000 across the $250,000 ROV system, $80,000 sensors, $150,000 vessel lease deposit, and $20,000 workstations, so cash for distributions starts under pressure. Project maintenance is modeled at 5% of revenue in Year 1 and 3% in Year 5.

Count batteries, tethers, thrusters, cameras, sensors, and replacement reserves as real costs, even when cash timing is uneven. If those reserves are underfunded, reported profit can look fine while free cash drops, and the owner’s draw gets squeezed after one repair, one lost camera, or one failed thruster.

Fund Replacement Cash First

Track each asset by service hours, repair history, and expected replacement date. Use project revenue to fund a reserve line before owner distributions, then hold cash for wear items and downtime. The clean test is simple: if the reserve can’t cover the modeled 5% first-year maintenance load, owner pay is too aggressive.

- Track revenue by project.

- Log hours on each ROV component.

- Set aside cash after every invoice.

- Forecast battery and tether swaps.

Document what fails, how often, and what it costs. That makes pricing and reserve planning tighter, and it protects take-home income when parts prices jump or a mission needs unexpected replacement gear.

4

Travel And Mobilization

Travel And Mobilization Costs

When work stays local and repeat, travel stays small and margin holds. When jobs move farther out, the owner needs mobilization fees, lodging coverage, and tight scheduling, or profit leaks fast. In this model, travel and mobilization run at 12% of revenue in Year 1 and 8% in Year 5, so a $100,000 job can lose $12,000 before other direct costs if travel is priced wrong.

Here’s the quick math: if revenue rises but routing is weak, owner tak e-home can still drop because idle crew and vehicle time eat cash. Bundle nearby marina, dock, hull, and infrastructure jobs into one trip so the same day covers more billable work. Local repeat routes protect margin because they spread travel across more hours and reduce empty miles.

Price the Trip, Not Just the Job

Track miles driven, nights away, travel hours, mobilization fee, and lodging cost on every project. Use those inputs to test whether each route still clears the 12% first-year travel load. One clean rule: if the trip adds unbilled time, the job is underpriced.

- Charge more for long-distance work.

- Bundle nearby sites into one route.

- Cover lodging before departure.

- Block schedules to cut idle time.

What this estimate hides: weather delays, site access gaps, and reroutes can push travel cost above plan. Build a simple route sheet before booking, then compare actual travel cost to revenue after each job. If travel cost drifts toward the model’s 8% Year 5 level, the owner keeps more cash for pay.

5

Owner Role And Labor Workflow

Owner Labor Split

The owner’s take-home changes with the job mix: piloting, sales, editing footage, client management, and report writing all sit inside this driver. If the owner does too many low-value tasks, profit draw gets delayed because cash is tied up in labor instead of distributions. One clean rule: the owner should spend time where the business most needs judgment, not admin.

Here’s the quick math: payroll rises from $395,000 to $840,000, including $150,000 owner salary, $110,000 lead technical salary, and $95,000 data analyst salary. Added pilot capacity helps coverage and quality control, but it also lifts the utilization bar before owner distributions appear. One more hire can protect service quality and still reduce free cash.

Track Role Utilization

Measure billable hours by role, not just total hours sold. The inputs that matter are pilot time, sales time, editing time, client calls, and reporting time. If non-billable work grows faster than booked projects, owner pay gets squeezed even when revenue looks fine. Utilization means billable time divided by available time.

- Track owner billable share weekly.

- Cap editing and reporting spillover.

- Model payroll against booked projects.

- Use hires to raise capacity only.

6

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Income changes fast here because pricing, utilization, and staffing move together. The lean case reflects first-year ramp, base follows Year 3 scale, and high assumes Year 5 capacity and owner pay.

| Scenario | Lean CaseLean Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | A lower-earnings ramp with limited utilization and heavy startup payroll. | A modeled mid-scale year with steadier service mix and still-elevated staffing. | A stronger operating year with fuller utilization, better pricing, and more monitoring work. |

| Typical setup | About $86,000 revenue, 83% gross margin, $395,000 payroll, and $74,400 fixed overhead, before capex. | About $484,000 revenue, 86% gross margin, and $535,000 payroll, with more inspection and survey work flowing through the team. | Year 5 scale with more monitoring contracts, 89% gross margin, $840,000 payroll, and $150,000 owner pay. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | -$408,000Lean Case | -$236,000Base Case | $150,000High Case |

| Best fit | Use this to stress-test Year 1 cash strain and hiring risk. | Use this for the Year 3 operating plan and break-even tracking. | Use this to test upside staffing and owner take-home. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Underwater Drone Exploration Porter's Five Forces Analysis

- Underwater Drone Exploration BCG Matrix

- Underwater Drone Exploration Business Model Canvas

- Tracking Key KPIs for Underwater Drone Exploration Services

- Underwater Drone Exploration Business Plan Template in Pre-Written Word

- Increase Underwater Drone Exploration Profitability: 7 Key Strategies

- How to Manage Running Costs for Underwater Drone Exploration

- Underwater Drone Exploration Startup Costs: $670K CAPEX Plan

- Underwater Drone Exploration Financial Model Template in Excel

- How To Open An Underwater Drone Exploration Business In 8–16 Weeks

- How to Write an Underwater Drone Exploration Business Plan

- Underwater Drone Exploration Marketing Mix

- Underwater Drone Exploration Marketing Plan

- Underwater Drone Exploration Business Proposal

- Underwater Drone Exploration PESTEL Analysis

- Underwater Drone Exploration Pitch Deck Example Editable PPTX

- Underwater Drone Exploration Business SWOT Analysis

- Underwater Drone Exploration Value Proposition Canvas

Frequently Asked Questions

The researched model pays the owner $150,000 per year before personal taxes That is payroll, not profit distribution Revenue grows from about $86,000 in the first year to $102 million in Year 5, but EBITDA stays negative through Year 5, so extra take-home is not supported in the base case