Owner income$5.8k/mo

Owner income$5.8k/moHow Much Upcycled Fashion Brand Owners Make: $70k Pay Model

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$5.8k/mo  Net margin83%–85.5%

Net margin83%–85.5% Revenue for target pay$82k–$84k

Revenue for target pay$82k–$84k Business difficultyHard

Business difficultyHard

This US estimate separates owner take-home, revenue, gross profit, operating profit, cash reserves, and reinvestment The model shows annual revenue rising from about $55k in Year 1 to $407M in Year 5, with a planned founder salary of $70k and EBITDA moving from -$148k to $309M It excludes tax advice and does not treat profit as guaranteed owner distributions

Owner income$5.8k/moNet margin83%–85.5%Revenue for target pay$82k–$84kBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner take-home depends on sales, margin, payroll, taxes, debt, reserves, and owner draws. This is not salary, tax advice, or owner distribution advice.

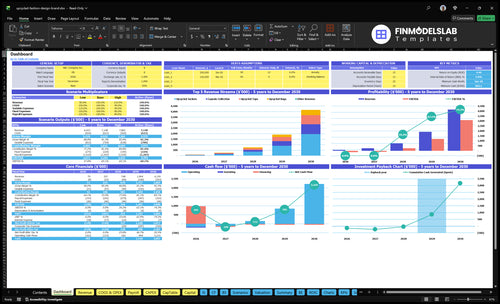

Want the full cash-flow view for the Upcycled Fashion Brand?

Open the Upcycled Fashion Brand Financial Model Template for cash flow, revenue, costs, and owner take-home assumptions.

Owner-income model highlights

- Owner take-home charts

- Revenue ramp $55k to $407M

- EBITDA swing -$148k to $309M

- Month 26 breakeven

- Month 39 payback

- Minimum cash $605k

How much revenue does an upcycled fashion brand need to pay the owner?

If you want the Upcycled Fashion Brand to pay the owner $70k, treat that as a pre-tax planning goal, not a Year 1 promise. With revenue of about $55k in Year 1 and -$148k EBITDA, the model does not yet cover the owner plus the rest of the cost stack. Revenue rises to about $688k in Year 3 with $256k EBITDA, and about $407M in Year 5 with $309M EBITDA.

Owner pay hurdle

- $70k is a planning target.

- Year 1 revenue is about $55k.

- Year 1 EBITDA is about -$148k.

- COGS, fees, shipping, and packaging come first.

What changes the bar

- Gross margin sets the ceiling.

- Marketing spend lifts the hurdle.

- Outsourcing can change margin fast.

- Reinvestment delays owner pay.

How do you scale an upcycled fashion brand without hurting take-home?

Scale helps the Upcycled Fashion Brand only when revenue grows faster than labor, inventory, and marketing. Owner-made production protects control but caps units, while contracted sewing can lift volume and also adds cash risk and quality checks. Here’s the quick read: limited drops only work if demand is real, and wholesale or boutiques should be judged on net margin and cash timing, not top-line sales. In the model, higher-priced capsule collections rise from 100% to 200% of sales mix, so pricing can protect take-home better than chasing low-margin volume.

Protect take-home

- Keep owner-made work for control.

- Use it for highest-risk pieces.

- Limit drops to proven demand.

- Lift capsule mix in the model.

Watch cash drag

- Contracted sewing can raise volume.

- It also adds cash risk.

- Wholesale cuts net margin.

- Judge pop-ups by contribution margin.

What profit margin for upcycled clothing should founders plan for?

Founders should plan for a very high gross margin on the Upcycled Fashion Brand, but not confuse that with take-home pay. The researched gross margin after material acquisition and direct production labor runs from 900% in Year 1 to 915% in Year 5; if you want the setup math, see What Is The Estimated Cost To Open And Launch Your Upcycled Fashion Brand?. Net profit is lower once $3,820 a month in overhead, wages, marketing, reserves, repairs, complex design, returns, slow sourcing, and owner maker time hit the model.

Gross margin

- 900% in Year 1

- 904% in Year 2

- 908% in Year 3

- 912% in Year 4

Net profit pressure

- 915% in Year 5

- 830% to 855% contribution margin

- $3,820 monthly overhead

- Owner maker time cuts take-home fast

Want to see what moves owner income most?

1

$202-$288AOV Pricing

Higher order value lifts take-home on every sale, so pricing on jackets, tops, bags, and capsule pieces drives profit fast.

2

$55K-$407MOrder Volume

More units and a faster drop cadence scale revenue, and that spreads fixed studio and labor costs across more sales.

3

900%-915%Gross Margin

Labor efficiency and material recovery keep more sales dollars in the business, which raises owner cash.

4

Net cashChannel Mix

The split between direct sales, fees, and discounts changes how much cash is left after each order.

5

$45->$30Marketing CAC

Lower customer acquisition cost helps paid growth stay efficient even as the marketing budget rises.

6

$605KCash Discipline

Cash control matters because the model bottoms at $605K in Month 25, so inventory and spend can strain take-home.

Upcycled Fashion Brand Core Six Income Drivers

Average Order Value and Pricing

Pricing and AOV

Higher prices can lift owner take-home only if buyers still accept the value story. Here the key metric is weighted AOV, which rises from about $202 in Year 1 to $288 in Year 5 as the mix shifts toward bags and capsule pieces. That is a 42.6% lift in revenue per order before fees, returns, and shipping.

Price changes are already built in: jackets move from $250 to $280, tops from $120 to $140, bags from $80 to $95, and capsule items from $400 to $450. The risk is simple: if conversion drops, returns rise, or discounting gets deeper, the AOV gain can vanish and owner profit falls fast.

Track price response by drop

Raise prices in small steps and watch what happens to conversion rate, returns, discount depth, and product fit with the brand story. If buyers value one-of-one design, craftsmanship, limited drops, and sustainability, price can move up without hurting sell-through.

- Track AOV by product mix.

- Test price on new drops first.

- Compare margin after returns.

- Cut discounts before raising prices.

- Check conversion after each change.

1

Unit Volume and Drop Cadence

Unit Volume and Drop Cadence

Owner take-home rises when finished pieces sell through without overloading the production line. In the model, units per order rise from 110 to 130, and revenue rises from about $55k to $407M. That only works if sourcing, cutting, sewing, photography, packing, and support can keep up. Limited drops help test demand and protect cash; unsold inventory turns gross margin into trapped cash.

Track sell-through before scaling drops

Here’s the quick math: track units made, units sold, sell-through rate (sold divided by made), and maker hours per piece. Keep drops small until the last batch clears cleanly. If sell-through weakens, slow the next drop or cut batch size; if maker hours run long, labor and inventory rise faster than cash, and owner pay gets squeezed.

2

Gross Margin and Labor Efficiency

Labor Efficiency and Gross Margin

Upcycled fashion only pays the owner if each piece keeps enough spread after material acquisition and processing and direct production labor. The source model shows materials at 25% to 30% of sales and labor at 60% to 70%, so every extra minute matters. If labor stays high, a piece can still look premium and still reduce take-home income.

Track real sewing time, scrap, and rework by style. Owner labor counts even if no hourly wage is paid at first, so unpaid hours still hit profit. Here’s the quick math: if a design needs more hours than its selling price can support, gross profit gets squeezed and there’s less left for overhead, cash reserve, and owner draw.

Cut Build Time, Protect Owner Pay

Batch similar repairs, standardize patterns, and price by time, not just by look. One clean rule: fewer minutes per unit = more owner income. Measure units started, units finished, sewing hours, and rework hours so you can see which styles earn enough after labor.

- Split labor by task.

- Use the same pattern blocks.

- Flag long-running pieces early.

- Stop scaling slow styles.

If a complicated reconstruction looks premium but takes too long, it can still hurt take-home. Keep those pieces limited until the time study proves the margin holds.

3

Sales Channel Mix and Fees

Sales Channel Mix and Fees

Channel mix changes both cash timing and owner take-home. Direct-to-consumer usually keeps more margin, but here e-commerce platform and payment fees are modeled at 30% of sales in Year 1, falling to 25% by Year 5. Here’s the quick math: $10,000 in online sales at 30% leaves $7,000 before labor, shipping, and overhead.

Wholesale, boutiques, consignment, marketplaces, and pop-ups can widen reach, but they can also cut take-home through discounts, booth costs, returns, or delayed payment. What matters is contribution margin and cash collected, not top-line sales. A channel that books revenue but pays late can still squeeze the owner’s draw.

- Inputs: channel mix, orders, AOV

- Track: fees, discounts, returns, pay lag

- Test: cash per order by channel

Measure Net Cash by Channel

Build a channel P&L for each path. Compare net cash per order, fee rate, discounts, returns, and days to cash. If one channel pays same day and another settles in 30 to 60 days, the same sales number creates very different working capital and owner pay.

Start with the channel that protects margin, then add others only when the extra reach beats the fee drag. If 30% fees plus discounts push contribution too low, cap volume or raise price. The goal is simple: keep the channels that turn sales into usable cash for payroll, inventory, and owner income.

4

Marketing Efficiency and CAC

Marketing Efficiency and CAC

If spend only buys orders, owner pay gets thin fast. Here, annual marketing rises from $15k in Year 1 to $100k in Year 5, while CAC drops from $45 to $30. The real test is contribution profit, meaning cash left after direct costs, not just sales volume.

The repeat side matters more over time. Repeat customers rise from 150% to 450% of new customers, repeat life stretches from 6 to 18 months, and repeat order frequency climbs from 0.25 to 0.60 orders per month. If payback is slow, marketing just front-loads cash out the door.

Track cash payback, not clicks

Judge organic content, email, influencer seeding, paid ads, and pop-ups by channel CAC and cash payback. Track new customers, repeat share, and how long it takes each channel to recover spend. One clean rule: if repeat buyers do not raise contribution faster than spend grows, cut or fix the channel.

- CAC by channel

- Payback months

- Repeat customer share

- Orders per repeat buyer

- Contribution after channel fees

5

Inventory and Cash Reserve Discipline

Cash Reserve Discipline

Cash reserves control owner pay even when margins look strong. In upcycled fashion, cash gets tied up in materials, packaging, production help, returns, photography, and new drops, so profit on paper does not equal cash available to draw.

The model shows a $605k minimum cash need at Month 25, breakeven at Month 26, and payback at Month 39. With $41k of capex for machines, tools, inventory, studio setup, photography equipment, website, furniture, and storage, reserve planning is not leftover cash.

Track Cash Before Owner Draw

Measure cash on hand, inventory on hand, open payables, and cash tied to each drop. Here’s the quick math: if cash must cover $41k of capex plus working capital, owner take-home should wait until sell-through turns cash back fast.

Track these inputs each month:

- Units made and sold

- Sell-through rate by drop

- Returns and rework cost

- Monthly fixed costs

- Capex and drop timing

- Owner draw timing

If a drop moves slowly, cash stays trapped longer and owner income drops with it.

6

Scenario objective for low, base, and high owner income planning

Owner income scenarios

Owner income moves from salary-only to distribution-heavy as revenue grows, cash strain eases, and reinvestment needs fall. Founder pay, staffing, and working capital drive the gap.

| Scenario | Low CaseCash strain | Base CaseModeled base | High CaseUpside case |

|---|---|---|---|

| Launch model | This is a lean launch where founder pay is capped and the business is still proving demand. | This is the modeled full-time case with founder pay funded and profits starting to support distributions. | This is a scaled upside case where owner income can expand, but cash use and reinvestment get much harder to manage. |

| Typical setup | About $55k revenue, 900% gross margin, and -$148k EBITDA, with founder pay up to $70k only if funded. | About $688k revenue, 908% gross margin, and $256k EBITDA after a $70k founder salary, with breakeven already passed. | About $407M revenue, 915% gross margin, and $309M EBITDA after a $70k founder salary, with distributions shaped by taxes, debt, inventory, and reinvestment. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Up to $70k salarySalary only | Salary plus distributionsDraws possible | Salary plus major distributionsHigh upside |

| Best fit | Use this to stress-test demand proof and cash survival before relying on distributions. | Use this for a full-time operating plan with controlled reserves and some owner draw potential. | Use this to test the upside ceiling, not the likely near-term take-home. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Upcycled Fashion Brand Porter's Five Forces Analysis

- Upcycled Fashion Brand BCG Matrix

- Upcycled Fashion Brand Business Model Canvas

- 7 Essential KPIs to Guide Your Upcycled Fashion Brand

- Upcycled Fashion Business Plan Template in Pre-Written Word

- How to Boost Upcycled Fashion Brand Profitability in 7 Steps

- How To Budget and Run an Upcycled Fashion Brand Monthly Costs

- Upcycled Fashion Brand Startup Costs: $41k CAPEX And $605k Cash Need

- Upcycled Fashion Financial Model Template in Excel

- How to Start an Upcycled Fashion Brand in 8 to 16 Weeks

- How to Write an Upcycled Fashion Brand Business Plan

- Upcycled Fashion Brand Marketing Mix

- Upcycled Fashion Brand Marketing Plan

- Upcycled Fashion Brand Business Proposal

- Upcycled Fashion Brand PESTEL Analysis

- Upcycled Fashion Brand Pitch Deck Example Editable PPTX

- Upcycled Fashion Brand Business SWOT Analysis

- Upcycled Fashion Brand Value Proposition Canvas

Frequently Asked Questions

The modeled launch capex totals about $41k before operating losses That includes $8k for sewing machines, $10k for studio setup, $7k for website development, and $5k for initial material inventory The bigger issue is cash runway: fixed overhead is $3,820 per month, and the model’s minimum cash need reaches $605k at Month 25