Owner incomeY1 -$112k; Y2 $14k; Y3 $263k

Owner incomeY1 -$112k; Y2 $14k; Y3 $263kHow Much Can a Used Bookstore Owner Make? $0 to $263k by Year 3

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner incomeY1 -$112k; Y2 $14k; Y3 $263k  Net margin87%

Net margin87% Revenue for target pay$207k

Revenue for target pay$207k Business difficultyHard

Business difficultyHard

Used bookstore owner income can be $0 in the first year if the store is still ramping and cash is being used to cover losses In the researched case, EBITDA is -$112k in Year 1, $14k in Year 2, and $263k in Year 3 before taxes, debt service, reserves, and owner distributions If the owner also fills the Store Manager role, the model includes a $55k annual manager salary, but that pay still depends on cash availability These are planning estimates, not guaranteed earnings or salary advice

Owner incomeY1 -$112k; Y2 $14k; Y3 $263kNet margin87%Revenue for target pay$207kBusiness difficultyHardWant to test your own used bookstore owner income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

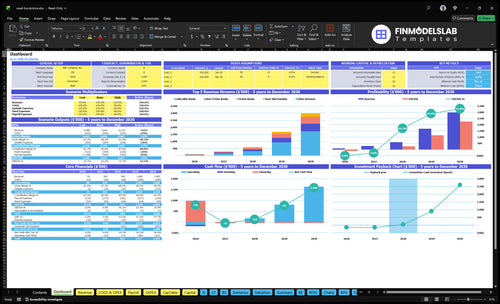

How does the Used Bookstore model show owner income?

This screenshot shows revenue, margin, costs, reserves, and owner take-home flow; open the Used Bookstore Financial Model Template. It’s the next planning step.

Owner-income model highlights

- EBITDA by year

- Month 19 break-even

- $734k cash need

- 37-month payback

- 0.06% IRR

- 367% ROE

- Traffic drives owner pay

- Scenario testing checks assumptions

How much revenue does a used bookstore need to pay the owner?

A Used Bookstore needs about $172k/month in revenue to cover $4,475 in fixed costs and $9,583 in payroll before owner pay. Here’s the quick math: $14,058 in monthly fixed costs divided by an 81.5% contribution margin gets you there, and a $5k/month owner draw lifts the target to about $234k/month. Reserves, taxes, debt service, and slow inventory turns can push the real target higher.

Break-even math

- $4,475 monthly fixed costs

- $9,583 monthly payroll

- $14,058 total monthly burden

- $172k/month break-even revenue

Owner pay target

- $5k/month owner draw

- $234k/month revenue target

- 81.5% contribution margin used

- Higher if turns stay slow

How do used bookstore profit margin and inventory cost affect owner income?

For a Used Bookstore, margin is the quiet driver of owner take-home: Year 1 gross margin is 87% after 10% inventory acquisition cost and 3% trade-in credit redemption, and by Year 5 it rises to 90% as those fall to 8% and 2%. If you’re sizing startup spend, see How Much Does It Cost To Open And Launch Your Used Bookstore Business? But gross margin is not net income, because payment fees, marketing, rent, utilities, insurance, software, payroll, shrinkage, markdowns, sorting labor, and unsold books still hit cash.

Year 1 to Year 5

- 87% gross margin in Year 1

- 10% inventory acquisition cost

- 3% trade-in credit redemption

- 90% gross margin by Year 5

What still cuts income

- Payment fees reduce cash

- Rent and utilities keep running

- Payroll and sorting labor matter

- Unsold books still tie up money

Can a used bookstore support a full-time owner?

Yes, a Used Bookstore can support a full-time owner, but not from gross sales alone; track operating profit after book costs, payroll, rent, and reserves, then benchmark it with What Is The Current Growth Rate Of Book Sales At Your Used Bookstore?. This model shows -$112k EBITDA in Year 1, breakeven in Month 19, and $263k EBITDA by Year 3 before taxes, debt, reserves, and owner distributions.

Owner Pay Test

- Start with EBITDA, not sales

- Year 1: -$112k EBITDA

- Breakeven: Month 19

- Year 3: $263k EBITDA

Cash Reality

- Fund early draws with startup cash

- Deduct book costs and rent

- Reserve for taxes and debt

- Owner can replace $55k manager role

Want the six used bookstore income drivers?

1

50-240/dayFoot Traffic

More visitors at 18% conversion add orders before fixed costs bite, so EBITDA scales fastest here.

2

$29.90Order Value

The 2-unit basket lifts each sale, and a bigger mix of higher-price books pushes take-home cash up.

3

13%-10%Inventory Cost

Lower buy cost and tighter trade-in credits drop COGS, which flows straight into EBITDA.

4

87%Gross Margin

Better pricing and faster sell-through keep margin from leaking into markdowns and dead stock.

5

$4.5K/moOccupancy Cost

Rent-heavy fixed costs hit every month, so lean space use lowers the break-even bar.

6

$115K/yrStaffing Load

Year 1 payroll is the biggest fixed drag, so labor mix and owner hours decide profit speed.

Used Bookstore Core Six Income Drivers

Sales Volume and Foot Traffic

Sales Volume and Foot Traffic

More visitors only help when they buy and the shelves match demand. In this used bookstore, daily traffic ranges from 50 on Monday to 120 on Saturday, with conversion starting at 18% and rising to 26% by Year 5. Revenue scales from transactions × $2990 Year 1 average order value, so foot traffic turns into income only when browsing becomes checkout.

Repeat buyers matter too: repeat share rises from 40% to 60%. That supports owner income because return visits cost less than new traffic. The risk is weak local foot traffic, poor merchandising, or events that cost more than they sell, which can lift visits but still leave cash flow weak.

Measure Traffic to Cash

Track daily visitors, conversion rate, repeat share, and event profit. Here’s the quick math: Revenue = visitors × conversion × average order value. Compare Monday, midweek, and Saturday traffic separately, because a store with 120 Saturday visitors can still underperform if most are just browsing.

Improve this driver by matching inventory to demand, tightening displays, and cutting low-return events. If conversion stays near 18%, traffic is not paying the bills. Move repeat share toward 60% with good stock and loyalty offers, so more transactions feed gross profit, cash flow, and owner pay without adding much rent or labor.

1

Average Transaction Value

Average Transaction Value

Average transaction value is the cash from one checkout. In a used bookstore, it rises when customers buy more units per order or choose higher-priced categories. Year 1 starts at 2 units per order and a model-listed $2,990 average order value; by Year 4 and Year 5, orders move to 3 units, so revenue per visit should improve if pricing and demand hold.

The key inputs are order count, units per order, category mix, unit price, and gross margin. Collectible books rise from 15% to 23% of sales mix and from $50 to $75 per unit, so basket size can climb fast. But higher sales only help owner pay if sell-through stays healthy and markdowns stay low.

Lift Basket Size

Track units per order, average order value, and sell-through by category every week. Test bundles, children’s stacks, gifts, and store-credit rules, then keep what raises basket size without raising shrinkage or labor too much. One clean rule: higher AOV only helps when the extra item still earns margin.

- Watch collectible share monthly.

- Measure markdowns on slow titles.

- Price bundles above single-book baskets.

- Keep labor tied to real sales.

If baskets get bigger but books sit longer, cash gets trapped on shelves and owner draws get tighter. If the store keeps margin healthy, each extra item helps cover rent, payroll, and the owner’s take-home income.

2

Inventory Acquisition Cost

Inventory Acquisition Cost

For a used bookstore, this is the cash and credits spent to get sellable books onto the shelf. It moves gross profit fast: acquisition cost falls from 10% of revenue in Year 1 to 8% in Year 5, so on $100,000 of sales that’s $10,000 down to $8,000. That 2-point drop only helps if the books actually sell.

Trade-in credit redemption also matters, easing from 3% to 2% of revenue. But cheap stock can still hurt owner income if it sits unsold, gets damaged, or needs heavy sorting. The real driver is cost per sellable book, not just cost per book bought.

Control Cost Per Sellable Book

Track buybacks, donations, estates, and trade-credit redemptions separately, then net them against unsellable rate, sorting labor, and shrink. If acquisition looks low but sell-through is weak, gross margin is fake. The store makes more money when every $1 spent on inventory turns into shelf-ready stock that clears fast.

Use a simple test: measure inventory acquisition cost as % of revenue, then compare it with sell-through by category. Cut stale categories early, cap damaged copies, and limit trade credit if liabilities pile up. Cheap inventory only helps owner pay when it converts to cash, not when it fills storage.

- Track sell-through by category.

- Count unsellable books weekly.

- Watch trade-credit balances.

- Cap sorting labor hours.

- Watch storage limits closely.

3

Pricing, Gross Margin, and Sell-Through

Pricing, Gross Margin, and Sell-Through

Pricing sets the cash each shelf can make, but sell-through decides whether that cash shows up at all. With 87% gross margin in Year 1 and 90% by Year 5, most sales dollars stay in the store before rent and payroll. Fiction starts at $7, non-fiction at $9, collectible books at $50, and merchandise at $15.

Here’s the quick math: higher prices help only if books move. Slow turnover, markdowns, shrinkage, and stale stock cut net income and trap cash on the shelf. A book that sits unsold does not pay owner draw, and dead shelf space blocks the next sale. Track category sell-through, days on hand, and markdown rate by section.

Track Price Against Sell-Through

Set a floor price by category, then watch what sells within 30, 60, and 90 days. If fiction at $7 moves fast but non-fiction at $9 stalls, the issue is not just price; it is demand, mix, or display. The goal is to keep gross margin high without letting shelf space turn into dead cash.

Use a simple scorecard: sell-through rate, markdowns, shrinkage, and gross margin by category. If a section needs repeated markdowns, cut buy volume there, not just price. Premium-priced collectibles can lift revenue, but only if turnover stays healthy enough to fund rent, payroll, and owner pay.

4

Occupancy Cost

Occupancy Cost

For a used bookstore, occupancy cost is the monthly space bill: $4,475 total, including $3,500 rent, $400 utilities, $150 insurance, $100 software, $50 website, $200 cleaning, and $75 security monitoring. This cost only works when foot traffic, conversion, and repeat visits create enough gross profit to cover it and still leave room for owner pay.

Cheap space can still hurt income if it sits off the main walk path and reduces walk-ins. Higher rent can be fine when the store has enough visibility, strong sell-through, and space for sorting, displays, and backstock. Here’s the quick test: if the location does not improve sales quality, lower rent may not improve take-home income.

Track rent against sales, not just the lease

Measure occupancy cost as a share of monthly gross profit, not just as a flat bill. Track visitors, conversion, repeat visits, and average basket size so you can see whether the space earns its keep. If traffic is weak, the rent problem is really a sales problem.

Test locations by looki ng at walk-in demand, shelf room, and backstock capacity before signing. A store that supports better browsing and inventory depth can justify higher fixed cost, but only if it lifts gross profit enough to cover $4,475/month and protect cash flow.

- Track monthly gross profit first.

- Watch walk-ins and conversion.

- Check room for backstock.

- Compare rent to sales lift.

5

Staffing and Owner Labor

Staffing and Owner Labor

Year 1 payroll is $115k: $55k Store Manager, $35k Lead Bookseller, and $25k Part-time Bookseller. That cost decides if the owner is earning wages, real profit, or both. If the owner fills the manager role, cash payroll can fall, but take-home income is being bought with owner labor hours, not just store profit.

Scalable income starts only when the store covers all paid labor and still leaves EBITDA (earnings before interest, taxes, depreciation, and amortization). If part-time coverage or marketing support expands, payroll rises, so the store needs stronger gross profit and steadier sales just to keep owner pay intact.

Track labor before you add hours

Measure payroll as a share of gross profit, not just sales. Track owner hours, manager coverage, part-time coverage, and the cash left after payroll each month. Here’s the quick math: if the owner steps in as manager, payroll drops, but the owner should still count those hours as labor cost when judging profit.

Test staffing changes against sales lift from better coverage. Add hours only when they raise conversion, repeat visits, or marketing response enough to support the extra wage load. If labor rises faster than gross profit, owner distributions shrink even when the store looks busy.

- Track payroll dollars per month

- Log owner hours by role

- Compare sales lift to labor growth

- Protect EBITDA before owner draws

6

Compare low, base, and high used bookstore owner income outcomes

Owner income scenarios

Owner income swings with traffic, conversion, repeat buying, and the need to cover rent and payroll before any draw. These cases map a cash-heavy launch, near breakeven, and distribution-capable upside.

| Scenario | Low CaseCash-heavy launch | Base CaseNear breakeven | High CaseDistribution-capable |

|---|---|---|---|

| Launch model | Year 1 runs at -$112k EBITDA, so the owner is cash-funding the manager role instead of taking a profit draw. | Year 2 reaches $14k EBITDA and Month 19 breakeven, so owner income stays tight and reserve-first. | Year 3 reaches $263k EBITDA before taxes, reserves, debt service, and distributions, so the store can support owner payouts. |

| Typical setup | Monthly revenue is about $12k, gross margin after inventory costs is not enough to cover the $3,500 rent and payroll, and the owner has to stay hands-on. | Monthly revenue is about $20k, gross margin stays tight once rent and payroll land, and the owner still has to protect cash through the breakeven month. | Monthly revenue is about $30k, the collectible mix lifts gross margin, and rent and payroll are covered before reserves, debt service, and distributions. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | No profit distributionCash-funded only | Near breakevenTight cash control | $263k EBITDA pathUpside case |

| Best fit | Best for owners stress-testing a hard launch and a fully hands-on store role. | Best for operators who can hold reserves and wait for breakeven before paying themselves. | Best for founders modeling a scalable store that can fund distributions after the ramp. |

Planning note: These ranges use researched planning assumptions from the model, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Used Bookstore Porter's Five Forces Analysis

- Used Bookstore BCG Matrix

- Used Bookstore Business Model Canvas

- 7 Core KPIs to Master for Your Used Bookstore

- Used Bookstore Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Used Bookstore Profitability by 10%

- How Much Does It Cost To Run A Used Bookstore Monthly?

- Used Bookstore Startup Costs: $65K Setup Plus Cash Reserve

- Used Bookstore Financial Model Template in Excel

- How To Open A Used Bookstore In 8 To 16 Weeks With Launch Checks

- Writing Your Used Bookstore Business Plan: 7 Actionable Steps

- Used Bookstore Marketing Mix

- Used Bookstore Marketing Plan

- Used Bookstore Business Proposal

- Used Bookstore PESTEL Analysis

- Used Bookstore Pitch Deck Example Editable PPTX

- Used Bookstore Business SWOT Analysis

- Used Bookstore Value Proposition Canvas

Frequently Asked Questions

In this model, profit-supported distributions are unlikely in Year 1 because EBITDA is -$112k Year 2 reaches $14k EBITDA, and Year 3 reaches $263k before taxes, reserves, debt service, and distributions If the owner fills the $55k Store Manager role, that pay is labor compensation, not the same as business profit