Owner income$120k

Owner income$120kHow Much Virtual Escape Room Owners Make: $120K Modeled Owner Pay

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$120k  Net margin-84% to 40%

Net margin-84% to 40% Revenue for target pay$298k

Revenue for target pay$298k Business difficultyHard

Business difficultyHard

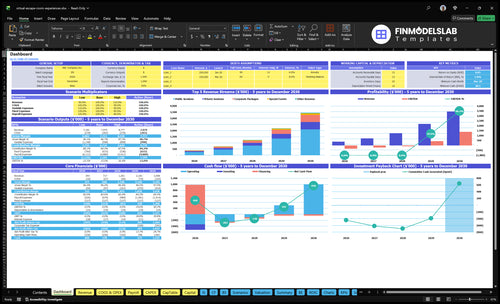

In this five-year planning model, virtual escape room owner take-home is modeled as a $120,000 annual CEO salary, while business profit stays negative until breakeven around Month 37 The page covers revenue, margins, facilitator costs, software fees, marketing spend, overhead, reserves, and scenario-based owner pay before taxes, debt service, and personal distributions

Owner income$120kNet margin-84% to 40%Revenue for target pay$298kBusiness difficultyHardWant to test your virtual escape room income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

How do you check owner income in the Virtual Escape Room financial model?

Dashboard tracks revenue, EBITDA, breakeven, payback, cash, and owner income; assumptions sit in the Virtual Escape Room Financial Model Template.

Owner-income model highlights

- EBITDA moves -$330k to $139m

- Year 4 hits $428k EBITDA

- Breakeven at Month 37

- Payback at Month 56

- Minimum cash: $28k

- Scenario tests Year 1-5

How does scaling a virtual escape room business affect owner income?

Scaling a Virtual Escape Room can lift owner income, but it usually lowers margin per booking because you need more facilitators, support, developers, and managers. In Year 5, the model assumes 96,500 bookings and packages, plus 50 Game Master FTEs, 25 Customer Support FTEs, and 10 Operations Manager FTEs, so growth is real but labor-heavy. Owner-led sessions save cash, but they also cap capacity; delegated delivery opens more dates, but seasonality, corporate lead times, and idle staff can delay distributions to the owner.

Owner-led sessions

- Lower cash burn per session

- Hard cap on bookings

- Owner time becomes the limit

- Faster profit, slower scale

Delegated delivery

- Higher revenue ceiling

- More labor risk from staffing

- Seasonality can leave shifts empty

- Owner payouts can lag

How many bookings does a virtual escape room need to make money?

If you’re asking when a Virtual Escape Room starts making real money, the model points to about 12,700 paid sessions or packages in Year 1, or about $385k in booking revenue before add-ons. That works out to roughly $303 per core booking, using $385k ÷ 12,700. By Year 4, the target jumps to 64,000 bookings and $215m in booking revenue before extras, with $100 to $115 corporate packages lifting average value.

Year 1 target

- 12,700 paid sessions or packages

- $385k booking revenue before add-ons

- About $303 per core booking

- Use bookings, not promises

Scale drivers

- 64,000 bookings in Year 4

- $215m booking revenue before extras

- $100 to $115 corporate packages lift value

- Repeat clients cut volatility, but need sales work

What is the virtual escape room profit margin?

Virtual Escape Room margins can look strong on paper, but you have to separate gross margin, contribution margin, EBITDA, and owner draw. For startup cost context, see How Much Does It Cost To Open The Virtual Escape Room Business? Here’s the quick math: Year 1 variable costs are 18% of revenue, so contribution before fixed costs and payroll is 82%; by Year 5, variable costs drop to 15%, leaving 85% before fixed costs.

Year 1 margin view

- 18% variable costs

- 82% contribution margin

- EBITDA is negative

- Owner draw is separate

Year 5 margin view

- 15% variable costs

- 85% contribution margin

- $139M EBITDA on $345M revenue

- That is about 40% EBITDA margin

Owner pay does not equal profit distributions, so don’t mix them in the margin line. Payment fees, cloud hosting, marketing commissions, and game master fees drive the early drag; if fixed payroll stays high, Year 1 stays red even with an 82% contribution base.

What to watch

- Track each cost bucket separately

- Keep payroll out of profit math

- Use EBITDA for operating profit

- Use owner draw for compensation

Key margin drivers

- Lower payment fees over time

- Reduce cloud and hosting waste

- Trim marketing commissions

- Keep game master costs lean

Want to see the main virtual escape room income drivers?

1

1.1K-8.0K/moPaid Volume

More paid sessions drive the jump from about $393K in Year 1 to about $3.45M in Year 5, so volume is the biggest top-line lever.

2

$31-$36Ticket Size

The blended revenue per booking rises as public, private, corporate, and event prices move up, and that lifts take-home on every session.

3

4%-5%Client Mix

A bigger share of corporate packages and repeat private groups pushes the average sale higher because those bookings price above public sessions.

4

8%-7%Game Masters

Game master labor is the biggest delivery cost, so every point cut here drops straight into contribution margin.

5

6%-5%Acquisition Cost

Marketing and sales commissions sit near 6% of revenue, so CAC control protects take-home as bookings scale.

6

$10.6K/moFixed Overhead

Fixed software and overhead total $10,550 a month before payroll, and that load is a key reason breakeven lands in Month 37.

Virtual Escape Room Core Six Income Drivers

Monthly paid bookings

Paid Bookings Volume

More paid sessions only lift owner income when each booking covers delivery labor, platform costs, support time, and marketing. The plan assumes 12,700 total bookings and packages in Year 1 and 96,500 by Year 5, so volume is the main top-line driver and the main path to breakeven. The catch is capacity: facilitator hours, customer support, and the event calendar can hit a wall fast.

Track Contribution per Booking

Track bookings by session type, then compare revenue per booking with variable cost per booking. Game Master Fees are 80% of revenue in Year 1 and 70% in Year 5, while Marketing & Sales Commissions are 60% and 50%. That means a fuller calendar helps only if each added session still leaves cash after fulfillment. Owner-hosted sessions save cash, but they cap volume.

1

Average revenue per booking

Average revenue per booking

Average revenue per booking is the ticket price plus any add-ons earned per paid session. For a virtual escape room, the mix matters: Year 1 prices are $25 public, $35 private, $100 corporate, and $75 special event; Year 5 rises to $28, $40, $115, and $85. More corporate and event bookings lift revenue per booking and can improve owner draw if conversion holds.

Here’s the catch: higher pricing only helps if players still buy and the experience feels worth it. Add-ons add $8k in Year 1 and $45k in Year 5, so upsells matter, but weak fit or thin quality can cut demand and reduce total cash, even when the sticker price is higher. One good booking with the right mix can beat several cheap ones.

Price the mix, not just the ticket

Track booking mix, add-on revenue, and conversion rate by public, private, corporate, and special event. Average revenue per booking equals total booking revenue divided by paid bookings, so the owner should watch whether price lifts are holding volume or just shrinking demand.

- Test price changes by segment.

- Watch add-on attach rates weekly.

- Protect corporate conversion first.

- Cut weak offers fast.

If price rises and bookings stay steady, owner income usually improves because each session contributes more cash toward delivery labor, support, and fixed overhead. If conversion slips, the extra price can vanish into lower volume, so forecast both revenue per booking and total bookings together.

2

Corporate and repeat client mix

Corporate mix

Corporate virtual escape room bookings lift order value and make revenue steadier because team events are booked in blocks, not one seat at a time. Here’s the quick math: 500 packages at $100 in Year 1 is $50,000, and 5,000 at $115 in Year 5 is $575,000. That mix can improve cash flow and owner pay if close rates stay solid.

This driver depends on sales follow-up, longer lead times, and repeat HR or team event demand. Repeat buyers lower acquisition pressure, but corporate demand is not automatic. If budget cuts hit, bookings can slow fast, so revenue gets lumpier and the owner has less room to pull cash out each month.

Track repeat close rate

Measure corporate bookings, repeat rate, average package price, and time from first call to close. If repeat HR clients are rising, you can forecast cash better and spend less to win the next deal. That helps protect margin because every repeat sale reduces fresh lead costs.

Watch the mix by month, not just by year. If the corporate share drops during slow sales periods, the owner may need more outbound follow-up or a tighter package price ladder. One clean rule: track bookings by source, then compare them with collected cash and facilitator hours.

3

Delivery labor model

Owner-led vs staffed delivery

Owner-operated delivery saves cash, but it turns the founder into the capacity limit. Once bookings rise, the business can only grow as fast as the owner can host sessions, handle support, and keep quality high.

Staffed delivery removes that bottleneck, but it adds Game Master Fees and payroll. In Year 1, those variable fees run at 80% of revenue; by Year 5, they still take 70%. That means labor is the main swing factor in owner take-home pay.

Track labor per booked session

Here’s the quick math: more Game Master FTEs can lift volume, but only if demand fills the calendar. Payroll grows from 10 Game Master FTEs in Year 1 to 50 in Year 5, so hiring ahead of bookings can crush EBITDA (earnings before interest, taxes, depreciation, and amortization) and drain cash.

Measure these inputs each month:

- Bookings per Game Master

- Game Master Fees as % of revenue

- Payroll FTEs vs. booked sessions

If the ratio slips, slow hiring before margin and owner draw get hit.

4

Customer acquisition cost

Customer Acquisition Cost

Customer acquisition cost is the spend needed to win each paid booking, including ads, commissions, discounts, and sales outreach. In Year 1, Marketing & Sales Commissions run at 60% of revenue, then ease to 50% in Year 5. That gap matters because every dollar saved on acquisition leaves more cash for payroll, fixed overhead, and owner pay.

For this model, the inputs are bookings, revenue per booking, commission rate, and sales effort. A lower CAC helps only if volume stays steady; otherwise, weak booking flow still leaves the owner short on cash. Repeat corporate clients, search traffic, and referrals improve margin because they cut paid selling pressure and smooth the calendar.

Track CAC by channel

Measure CAC separately for ads, referrals, search, and corporate outreach. Use the simple check: CAC per booking = total sales and marketing spend ÷ paid bookings. If a channel n eeds heavy discounts or long follow-up, its true CAC is higher than the ad bill alone, and owner take-home falls fast.

Push the mix toward repeat corporate bookings and organic demand, because those bookings usually carry less acquisition drag. Watch whether revenue stays high enough to cover fixed payroll and overhead after the 60% Year 1 marketing and sales load. If volume dips, a low CAC number on paper will not protect profit or draw.

- Track CAC by source each month

- Compare CAC to booking value

- Reduce discount-heavy sales offers

- Prioritize repeat corporate clients

5

Fixed software and overhead load

Fixed software and overhead load

Your owner pay rises when the fixed load stays lean, because these costs hit every month whether bookings are strong or not. The disclosed fixed expenses total $1055k per month, including $25k platform maintenance, $1k software licenses, $3k content development, and $15k G&A. Lower overhead helps early cash flow, but it only works if the experience still feels premium.

Here’s the tradeoff: cutting tools can save cash, but weak uptime, stale content, or clunky delivery can hurt reviews and corporate conversion. That hits revenue quality, not just cost. For this model, the key inputs are monthly bookings, price, platform reliability, content refresh cost, and G&A, because those decide how much of each sale reaches the owner’s draw.

Keep the fixed stack lean

Track monthly fixed spend against bookings, and separate what protects sales from what is just overhead. If a cheaper tool or lighter support plan lowers uptime or slows response times, the saved cash can vanish fast. The goal is simple: keep the monthly base low enough to support profit, but strong enough to protect premium pricing and repeat corporate deals.

- Track uptime, support time, conversion.

- Refresh content on a set cadence.

- Protect corporate demo quality first.

- Review G&A and software monthly.

6

Compare lean, base, and growth owner income scenarios

Owner income scenarios

Owner income swings with booking volume, corporate mix, payroll, and marketing efficiency. Early years stay cash tight; Year 5 can support salary plus distributions.

| Scenario | Low CaseLow case | Base CaseBase case | High CaseHigh case |

|---|---|---|---|

| Launch model | This is the downside path where bookings grow, but payroll and overhead still outrun cash. | This is the middle path where the business scales, but owner distributions are not safe yet. | This is the stronger earnings path where scale can support both pay and owner draws. |

| Typical setup | Year 1 style with about $393k revenue, 82% contribution margin, and -$330k EBITDA, so the owner usually needs outside funding to stay paid. | Year 3 style with about $1.24m revenue, 83.4% contribution margin, and -$81k EBITDA, so it is close but still not profitable. | Year 5 style with about $3.45m revenue, 85% contribution margin, and $1.39m EBITDA, with the modeled $120k CEO salary and room for distributions after reserves. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Funding-dependentCash tight | Salary onlyNear breakeven | $120,000+ distributionsProfit upside |

| Best fit | Use this to stress-test slow bookings and weak funding support. | Use this for a near-break-even plan with tighter control on payroll and sales efficiency. | Use this to test upside if bookings, corporate share, and marketing efficiency keep improving. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Virtual Escape Room Porter's Five Forces Analysis

- Virtual Escape Room BCG Matrix

- Virtual Escape Room Business Model Canvas

- 7 Essential KPIs for Virtual Escape Room Success

- Virtual Escape Room Business Plan Template in Pre-Written Word

- 7 Focused Strategies to Boost Virtual Escape Room Profitability

- How to Calculate Running Costs for a Virtual Escape Room Business

- Virtual Escape Room Startup Costs: $188K Launch Budget

- Virtual Escape Room Financial Model Template in Excel

- How To Open A Virtual Escape Room In 6–12 Weeks With Paid Pilots

- How to Write a Virtual Escape Room Business Plan in 7 Steps

- Virtual Escape Room Marketing Mix

- Virtual Escape Room Marketing Plan

- Virtual Escape Room Business Proposal

- Virtual Escape Room PESTEL Analysis

- Virtual Escape Room Pitch Deck Example Editable PPTX

- Virtual Escape Room Business SWOT Analysis

- Virtual Escape Room Value Proposition Canvas

Frequently Asked Questions

The model includes $120,000 in annual CEO pay, but that is funded owner compensation, not guaranteed profit The business shows -$330,000 EBITDA in Year 1, -$81,000 in Year 3, and $428,000 in Year 4 Distributions become more realistic after breakeven around Month 37