Owner income$180k

Owner income$180kHow Much Does A Virtual Shopping Mall Owner Make? $180K Model

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$180k  Net margin52.6%

Net margin52.6% Revenue for target pay$342k

Revenue for target pay$342k Business difficultyHard

Business difficultyHard

A virtual shopping mall owner can model $180,000 in first-year CEO pay if the owner fills that role, but distributable profit is not automatic Under the researched assumptions, the first year produces about $702,000 in GMV and $985,560 in platform revenue before known variable costs, marketing, fixed overhead, payroll, reserves, taxes, and debt service Here’s the quick math: first-year known payroll is at least $690,000, buyer and seller acquisition budgets total $350,000, and fixed overhead is $177,600 By the mature-year case, modeled platform revenue reaches about $403 million on $382 million GMV, but owner take-home still depends on reinvestment and reserve policy

Owner income$180kNet margin52.6%Revenue for target pay$342kBusiness difficultyHardWant to test your owner pay number?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue mix, margin, payroll, reserves, and cash timing.

Want to check owner income in the Virtual Shopping Mall model?

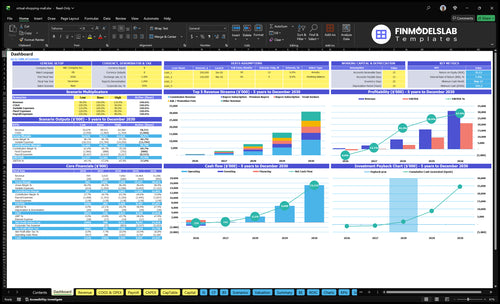

This dashboard shows GMV, platform revenue, gross margin, operating profit, cash available to owner, and reserve-adjusted take-home. Open the Virtual Shopping Mall Financial Model Template to pressure-test the $702,000 first-year GMV case, plus the $753 million base-growth and $382 million mature-year charts.

Owner-income model highlights

- Cash after reserves

- Revenue, margin, profit

- Scenario tests by growth

Is a virtual shopping mall passive income?

No—a Virtual Shopping Mall is not passive income. It needs active work in vendor recruitment, seller onboarding, shopper acquisition, merchandising, support escalation, fraud prevention, content moderation, payment issue handling, and platform operations. The first-year model already includes at least $690,000 of payroll for a CEO, CTO, Head of Marketing, and two Software Engineers, plus $100,000 to acquire 200 sellers at $500 CAC and $250,000 to acquire 10,000 buyers at $25 CAC. So, this is an operating business, not a hands-off asset.

Owner work

- Recruit sellers nonstop

- Onboard each seller

- Handle buyer support

- Moderate fraud and content

First-year math

- $690,000 known payroll

- 200 sellers at $500 CAC

- 10,000 buyers at $25 CAC

- Needs operating discipline

What is the virtual shopping mall profit margin?

Virtual Shopping Mall profit margin is negative in year one under the provided cost stack, because variable costs alone total 130% of platform revenue, before fixed costs, payroll, and acquisition spend. If you want the setup costs behind that number, see How Much Does It Cost To Open And Launch A Virtual Shopping Mall Business? Owner take-home only starts to improve after support, fraud prevention, moderation, admin, and reserves are fully funded.

Year 1 cost stack

- 130% variable costs on revenue

- 25% payment processing

- 15% cloud hosting

- 30% affiliate commissions

- 60% performance advertising

Fixed and funding drag

- $14,800/month fixed overhead

- $177,600/year fixed overhead

- At least $690,000/year payroll

- $350,000 first-year acquisition budgets

- 94% mature-year variable costs

How much revenue does a virtual shopping mall need to pay the owner?

A Virtual Shopping Mall can’t be sized to a universal owner-pay benchmark; the math starts with a $180,000 CEO salary assumption, or about $15,000/month, before you add other costs. First-year fixed overhead is $14,800/month before payroll, and payroll is already at least $690,000/year before incomplete roles, so net revenue has to cover that plus 130% variable costs, $350,000 of acquisition budgets, marketing, and reserves.

Owner pay math

- $180,000 CEO pay target

- $15,000/month owner-cost floor

- $14,800/month fixed overhead before payroll

- $690,000/year payroll floor

Revenue drivers

- 130% variable cost load in year one

- $350,000 acquisition budget total

- GMV depends on blended take rate

- Subscriptions can outrun commissions

Want the six income drivers?

1

$1.05MOperating Costs

The model carries $14.8K/month of fixed overhead plus $180K CEO pay, and Year 1 EBITDA is -$918K, so this is the fastest lever on burn, reserves, and owner cash.

2

10K buyersBuyer Traffic

$250K of buyer marketing at a $25 CAC brings about 10,000 first-year buyers, and that traffic is the base for the $702K GMV run rate.

3

$1.0MBlended Take

Commission, buyer fees, seller fees, and add-ons stack on top of GMV, so the blended take rate decides how much revenue reaches profit.

4

$69 AOVConversion and AOV

Better conversion and basket size push the same buyer pool into more GMV, and that lifts revenue without adding new acquisition spend.

5

200 sellersVendor Retention

With 200 first-year sellers and a $500 seller CAC, keeping vendors active protects assortment and avoids paying again for the same shelf space.

6

$25Customer CAC

If buyer CAC drifts above $25, the extra spend comes straight out of reserves before it can show up as revenue or owner income.

Virtual Shopping Mall Core Six Income Drivers

Qualified Shopper Traffic

Qualified Shopper Traffic

Traffic only pays off when visits become paid orders. In the first-year model, $250,000 of buyer marketing at $25 CAC brings in 10,000 buyers, which lifts gross merchandise value (GMV) and commission revenue if conversion, average order value, and repeat buying hold up. The risk is vanity traffic: more visits, more ad spend, but little cash left for owner pay.

Track buyers, not clicks

Measure acquired buyers, repeat purchase rate, and CAC by channel. Here’s the quick math: $40 million in mature buyer marketing at $15 CAC buys about 2.67 million buyers, but that only helps if order value and repeat orders cover acquisition cost. Track paid orders per buyer, not raw visits.

- Buyer CAC: $25 first year, $15 mature.

- Paid orders: per acquired buyer.

- Repeat purchases: by channel.

1

Conversion Rate And Average Order Value

Conversion Rate and AOV

For a virtual shopping mall, conversion rate and average order value (AOV) decide how much traffic turns into GMV (gross merchandise value), not owner income on day one. In the first-year model, AOV is $45 for casual shoppers, $75 for trend seekers, and $120 for premium buyers, with 10,200 modeled orders producing about $702,000 GMV.

GMV is only the base. Owner cash comes from commission revenue, which applies $1 per order plus 80% of order value, so weak conversion or low AOV cuts fee income fast. If the buyer mix stays stuck in lower tiers, the platform can still show traffic growth while take-home profit lags behind fixed payroll and overhead.

Track tier mix and order value

Measure conversion by traffic source, then split AOV by buyer tier so you can see where the money is. One clean rule: more premium buyers at the same traffic level means more GMV.

- Track AOV by $45, $75, $120 tiers

- Watch repeat orders: 0.80, 1.20, 1.80

- Separate GMV from commission revenue

- Test checkout steps that lift conversion

Use the model to forecast commission revenue, then compare it with fixed costs before setting owner draw. If conversion rises but AOV falls, GMV can stall even while visits look healthy. That gap is what usually squeezes cash flow first.

2

Active Vendors And Retention

Active Seller Retention

Vendors only help income when they stay active and sell. The model acquires 200 sellers with $100,000 of seller marketing, which implies $500 CAC per seller. That spend only pays off if sellers keep renewing and listing, because dormant accounts still carry acquisition cost but don’t keep subscription revenue flowing.

First-year seller subscriptions are about $187,200, and seller ads plus tools add about $180,000 if adopted monthly. Weak retention hurts assortment and repeat visits, so the owner loses recurring revenue and has less cash left for overhead and pay.

Keep Sellers Selling

Track active sellers, renewals, churn, and monthly ad-tool adoption. Here’s the quick math: if sellers sign up but do not list or sell, the platform looks full but cash flow stays thin. Revenue from this driver comes from sellers who are live, not from total registrations.

- Count active sellers each month.

- Watch seller churn and renewals.

- Measure ad and tool adoption.

Use activation checks, seller follow-up, and simple performance reviews on listings and promotions. If active seller count slips, assortment gets weaker and owner draw usually falls before fixed costs do.

3

Blended Take Rate

Blended Take Rate

Blended take rate is the platform’s share of sales and fees. It includes transaction commissions, seller subscriptions, buyer subscriptions, ads, and tools, so owner income depends on both order volume and fee mix. On $702,000 GMV and 10,200 orders, first-year commission revenue is about $571,800 from $1 per order plus 80% of GMV.

In mature year, the variable commission falls to 72%, which would cut commission revenue on the same GMV to $515,640, a drop of $56,160. That means subscriptions, ads, and tools must carry more weight. Higher fees can lift profit, but only if seller ROI and shopper pricing still work.

Track Fee Mix Against Seller ROI

Measure blended take rate as all fee revenue divided by GMV. Then split it by source so you can see how much comes from commissions, subscriptions, ads, and tools. Track AOV, orders per seller, and churn after any fee change, because a higher take rate that slows sales can reduce cash for owner pay.

Here’s the quick control set:

- Watch fee revenue per order.

- Track GMV by seller tier.

- Compare churn after price changes.

- Test ads and tools adoption monthly.

If seller sales soften after a fee hike, the platform may show higher gross revenue but weaker long-run profit.

4

Customer Acquisition Cost

Marketplace Customer Acquisition Cost

Customer acquisition cost is not just a growth line here; it decides whether new traffic turns into profit or cash burn. At $25 buyer CAC and $500 seller CAC, $250,000 in buyer marketing buys about 10,000 buyers, while $100,000 in seller marketing buys 200 sellers. If repeat orders and average order value do not cover that spend, owner pay gets squeezed fast.

Here’s the quick math: mature buyer CAC improves to $15 and seller CAC to $350, so scale gets cheaper only if behavior improves with it. A buyer engine that jumps from $250,000 to $40 million and a seller engine from $100,000 to $12 million can lift GMV, but it also raises cash needs before fees, subscriptions, and repeat purchases show up.

Track CAC by cohort, not just channel

Measure CAC by buyer and seller cohort, then compare it w ith repeat order rate and AOV by tier. Paid ads, affiliates, influencer campaigns, and SEO only work if the first order and follow-on orders repay the acquisition cost. A clean test is payback by cohort: if the margin from repeat purchases does not outrun CAC, cut spend or raise order value.

Keep a simple dashboard: buyers acquired, sellers acquired, CAC, repeat orders, and cash burn. Watch for scale where acquisition spend grows faster than repeat purchase behavior, because that usually means lower contribution and less owner draw. One line to remember: cheap traffic that does not reorder is still expensive.

5

Operating Cost Discipline

Operating Cost Discipline

Here’s the quick math: fixed overhead is $14,800/month, or $177,600/year, and payroll is at least $690,000/year for support labor, fraud prevention, content moderation, and admin overhead. That puts fixed operating load at $867,600/year before variable costs, reserves, reinvestment, or owner pay. If the business can’t cover that stack, take-home shrinks fast.

Variable costs add more pressure. At 130% of revenue, every $1 of sales creates $1.30 of processing, hosting, affiliate, and performance ad cost. So revenue growth alone can burn cash if cost control is weak; the owner gets paid only after these costs, reserves, and reinvestment needs are covered.

Track Cost Before Owner Pay

Measure the monthly cost stack in three lines: fixed overhead, payroll, and variable cost as a share of revenue. The key question is simple: does one more dollar of sales leave cash behind, or consume more cash than it brings in?

- Track variable cost by channel.

- Separate processing and ad spend.

- Review payroll per active order.

- Protect reserves before owner draws.

If support labor, fraud prevention, or content moderation grows faster than orders, margin drops and take-home income falls. Cut waste in performance ads first, then tie staffing and software spend to actual transaction volume, not projected traffic.

6

Scenario objective: compare lean, base, and high owner-income cases

Owner income scenario table

Income swings hard because this is a two-sided marketplace with heavy buyer and seller acquisition costs, fixed payroll, and thin first-year margins.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | A lower earnings path built on first-year buyer and seller ramp. | A modeled path with mid-stage growth and better repeat buying. | A stronger earnings path that depends on mature scale and mix shift. |

| Typical setup | Typical setup uses 10,000 buyers, 200 sellers, $702,000 GMV, $985,560 revenue, a 130% variable cost load, $350,000 acquisition budgets, $177,600 fixed overhead, and a $180,000 CEO salary. | Typical setup assumes about 75,000 buyers, 1,250 sellers, about $753 million GMV, and about $940 million revenue, with a healthier mix and more room to absorb fixed payroll. | Typical setup assumes 266,667 buyers, 3,429 sellers, about $382 million GMV, and about $403 million revenue, with reserves built before any owner distribution. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | -$918kLow Case | $365k - $3.5MBase Case | $9.4M - $21.1MHigh Case |

| Best fit | Use this to stress-test launch burn and owner draw timing. | Use this for a normal growth plan with reinvestment. | Use this to test scale, reserve buildup, and delayed distributions. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Virtual Shopping Mall Porter's Five Forces Analysis

- Virtual Shopping Mall BCG Matrix

- Virtual Shopping Mall Business Model Canvas

- Tracking 7 Core KPIs for Virtual Shopping Mall Success

- Virtual Shopping Mall Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Virtual Shopping Mall Profitability

- Analyzing the Monthly Running Costs for a Virtual Shopping Mall Platform

- Virtual Shopping Mall Startup Costs: $350K Launch Marketing Plus Build

- Virtual Shopping Mall Financial Model Template in Excel

- How To Open A Virtual Shopping Mall In 10 To 20 Weeks

- How to Write a Virtual Shopping Mall Business Plan in 7 Steps

- Virtual Shopping Mall Marketing Mix

- Virtual Shopping Mall Marketing Plan

- Virtual Shopping Mall Business Proposal

- Virtual Shopping Mall PESTEL Analysis

- Virtual Shopping Mall Pitch Deck Example Editable PPTX

- Virtual Shopping Mall Business SWOT Analysis

- Virtual Shopping Mall Value Proposition Canvas

Frequently Asked Questions

The model supports a $180,000 CEO salary assumption if the owner fills that role, but that is not the same as profit distribution First-year assumptions show about $985,560 in platform revenue, $702,000 in GMV, $350,000 in acquisition budgets, and at least $690,000 in known payroll before reserves and taxes