Owner income≈$150k base

Owner income≈$150k baseHow Much Waste Management Owners Make: $150K Pay And Year 5 EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income≈$150k base  Net margin-103% to 34%

Net margin-103% to 34% Revenue for target pay≈$445k to $4.3M

Revenue for target pay≈$445k to $4.3M Business difficultyHard

Business difficultyHard

Key Takeaways

- Denser routes cut fuel, labor, and truck wear.

- Pricing discipline protects cash as tipping fees rise.

- Higher truck utilization spreads fixed costs over more stops.

- Reserve planning prevents repairs from hitting owner distributions.

Owner income≈$150k baseNet margin-103% to 34%Revenue for target pay≈$445k to $4.3MBusiness difficultyHardWant to test your waste hauling owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Researched planning estimate only. It is not a guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margins, staffing, debt, reserves, and cash timing.

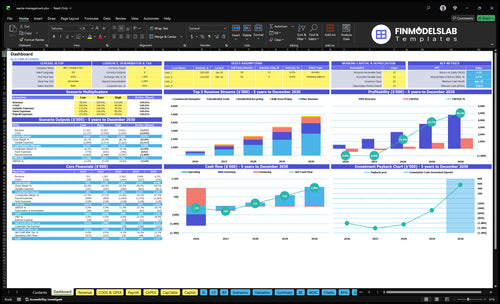

Want to check owner income in the waste hauling forecast?

This screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions in the Waste Management Financial Model Template—open the model.

Owner-income model highlights

- Owner take-home from assumptions

- Revenue and margin trends

- EBITDA: -$457k to $1.442m

- Month 28 breakeven

- 58-month payback, -$450k cash

What is the waste management business profit margin?

Waste Management profit margin starts deeply negative, then improves as fixed payroll, fleet insurance, office costs, and software get spread over more revenue; for the startup cost side, see How Much Does It Cost To Open And Launch Your Waste Management Business?. The implied EBITDA margin is about -103% in Year 1, -17% in Year 2, then 13%, 26%, and 34% by Year 5. EBITDA here excludes debt service, taxes, and reinvestment reserves.

Why margin rises

- More routes dilute payroll.

- More revenue lowers fixed cost share.

- Insurance spreads across more stops.

- Software cost per account falls.

Cost sensitivity

- Disposal fees fall from 8% to 7%.

- Fuel falls from 7% to 6%.

- Maintenance moves from 3% to 25%.

- Variable operating costs drop from 75% to 55%.

How much revenue does a waste management business need to pay the owner?

If you need to pay the owner $150,000, there is no fixed revenue threshold—margin assumptions decide the answer. In this Waste Management model, implied revenue rises from about $445,000 in Year 1 to $2.109 million in Year 3 and $4.304 million in Year 5, with Year 3 EBITDA at $272,000 after owner salary, wages, marketing, fixed overhead, and variable costs. Here’s the quick math: route density and truck utilization decide whether revenue actually turns into owner pay.

Revenue drivers

- $40 residential trash

- $25 recycling service

- $300 commercial dumpster

- $80 bulk pickup

Owner-pay math

- $150,000 owner salary supported

- Year 3 EBITDA: $272,000

- Year 1 revenue: $445,000

- Year 5 revenue: $4.304 million

How much can a waste management business owner pay themselves?

A Waste Management owner can pay themselves $150,000 per year, or $12,500 per month, in this model, as a General Manager / Owner wage from Month 1 through Month 60; see What Is The Current Growth Trend Of Waste Management Service? for market context. Distributions should be treated as $0 in Year 1 and Year 2 because EBITDA is negative at -$457,000 and -$207,000.

Owner Pay

- Pay salary: $150,000 annually

- Monthly draw: $12,500

- Runs from Month 1–60

- Separate from profit distributions

Cash Reality

- Year 1 EBITDA: -$457,000

- Year 2 EBITDA: -$207,000

- Breakeven hits Month 28

- Distribute after debt, taxes, repairs, reserves

Want the six drivers behind waste hauling income?

1

255%→21%Route Density

More stops per route spread fixed overhead and can push the Year 1 variable burden of 255% of revenue toward the Year 5 level near 21%, which is where owner take-home starts to show up.

2

$25-$350Contract Pricing

Monthly price per account ranges from $25 for recycling to $350 for dumpsters, so small rate lifts have a big effect on cash after labor, fuel, and disposal.

3

0.10→0.08Truck Utilization

Average billable hours per active customer fall from 0.10 to 0.08 by Year 5, so fuller routes and fewer dead miles protect margin.

4

8%→7%Disposal Fees

Tipping fees ease from 8.0% of revenue in Year 1 to 7.0% in Year 5, and every point saved flows straight to owner income.

5

$180K-$720KLabor Efficiency

Driver payroll scales from $180K to $720K, so schedule discipline and crew productivity matter as much as top-line growth.

6

10%-8.5%Fleet Costs

Fuel plus maintenance run about 10.0% of revenue in Year 1 and 8.5% in Year 5, so route planning and truck upkeep directly lift cash.

Waste Management Core Six Income Drivers

Route Density

Route Density

Route density is how many billable stops you pack into each truck run. Denser routes cut drive time, fuel per stop, labor hours, and truck wear, so more of each monthly bill turns into owner cash. With fuel at 7% of revenue in Year 1 and 6% in Year 5, wasted miles hit EBITDA fast.

The key inputs are stops per route, miles per pickup, route hours, and missed pickups. Tight residential zones help spread driver wages and fleet insurance across more billable accounts. Scattered accounts can keep trucks busy but still leave weak margins, which lowers safe owner distributions.

Tighten Pickup Zones

Track the route, not just the truck. If miles per pickup or route hours rise faster than billed stops, margin is leaking. Use zone maps, group nearby homes, and review missed pickups weekly so you protect cash before fuel and overtime eat it.

- Stops per route

- Miles per pickup

- Route hours

- Missed pickups

- Fuel as % of revenue

One clean test: if a route adds accounts but not density, it may look bigger and still pay less. That’s the risk in waste collection. Denser routes usually lift EBITDA and make owner pay safer because the same fixed labor and insurance are covering more billable work.

1

Contract Pricing

Contract Pricing

Contract pricing sets the ceiling for owner pay because every recurring service starts with the monthly rate. In Year 1, the model uses $40 for residential trash, $25 for recycling, $300 for commercial dumpster service, and $80 for bulk pickup, so monthly recurring revenue is just customer count times these prices.

What matters is not just price, but churn, price escalators, service level, contamination fees, and missed-payment rate. Underpriced contracts get squeezed when tipping fees and fuel rise, which cuts margin and leaves less cash for the owner to draw.

Track Price, Then Protect Margin

Use a simple formula: MRR = customers × monthly rate. Track each service line separately, then watch whether price changes stick through renewals and escalators. If residential or recycling churn rises after a price bump, the gross revenue gain can disappear fast. Cleaner billing and fewer unpaid invoices usually mean steadier owner distributions.

Measure billing frequency, missed payments, and service exceptions by contract. If contamination or overuse is common, add clear fee language now, not after margins slip. A one-line rule helps: price for rising disposal and fuel before they eat the draw.

- Check MRR by service line.

- Track churn after price changes.

- Enforce escalators in every contract.

- Bill contamination and missed pickups.

2

Truck Utilization

Truck Utilization

When a truck is busy on enough paid routes, the owner spreads $450,000 of truck capex, $2,000 monthly fleet insurance, and maintenance equal to 3% of Year 1 revenue across more billable stops or tons. That usually lifts EBITDA and leaves more cash for owner pay, but only if the route stays dense enough to cover fuel, labor, and disposal time.

Routes per truck, stops per route, tons per load, downtime, preventive maintenance, and overtime are the inputs that matter. Here’s the catch: every extra stop is not profitable if it adds long drive time or higher disposal costs. One empty hour can wipe out the gain from several small stops.

Track paid capacity, not just truck miles

Measure billable stops per route, tons per load, and route hours by truck. If a route looks full but drive time is high, the truck is underused in profit terms. Keep a simple weekly view of downtime, missed pickups, overtime, and maintenance days so you can see when utilization starts cutting owner cash.

Use the numbers to set guardrails. If a truck needs more overtime or more disposal time to add one stop, price that work higher or skip it. Preventive maintenance should be scheduled before breakdowns, because downtime turns fixed fleet costs into dead cash. Dense routes with clean pricing protect margin; scattered routes usually just make the truck look busy.

3

Disposal Tipping Fees

Disposal Tipping Fees

Disposal tipping fees are what you pay to dump collected waste at transfer stations and landfills, plus contamination charges. In this model, disposal fees run at 8% of Year 1 revenue and improve to 7% by Year 5, so every $100,000 of sales can lose about $8,000 at first. That cost comes straight off profit before owner pay, so bad control cuts the money left for distributions.

Here’s the quick math: the key inputs are cost per ton, tons per customer, transfer station fees, landfill charges, and contract pass-through terms. If disposal costs rise and pricing does not move with them, EBITDA compresses fast. Commercial dumpster accounts need tonnage limits and surcharge language, or heavy loads turn into surprise cash hits.

Track Tons and Pass-Throughs

Measure disposal cost by route and by customer, not just as one company average. Watch cost per ton against billed tons, and flag accounts with high contamination charges or big swings in load size. That shows which contracts are helping owner income and which ones are quietly draining margin.

Build pricing rules that let you pass through landfill and transfer station increases, especially on commercial dumpster work. For example, if a customer’s tonnage rises, the invoice should rise too. The goal is simple: protect gross margin, keep cash flow steady, and avoid owner draws getting hit by one big disposal bill.

4

Labor Efficiency

Labor Efficiency

Labor efficiency is how many stops you get from each paid hour, and it hits owner income fast because payroll is the biggest controllable load after fleet and disposal. In this model, payroll includes a $150,000 owner salary, $95,000 for an operations manager, drivers at $60,000 each, customer service at $45,000, and admin at $40,000.

Driver FTE rises from 3 in Year 1 to 12 in Year 5, so labor must scale with route density, not just headcount. Here’s the quick math: if stops per labor hour improve and overtime stays low, more revenue turns into cash for the owner. What this hides: understaffing can lift missed pickups, churn, and retraining costs.

Track Labor per Stop

Measure stops per labor hour, overtime, turnover, missed pickups, and training time. If route density is thin, adding staff before demand is there just raises fixed payroll and cuts distributions. If density is strong, the same payroll base can support cleaner margins and steadier owner pay.

- Compare staffed hours to route density.

- Flag routes with repeat missed pickups.

- Watch overtime before adding headcount.

- Track ramp time for new drivers.

Use separate plans for owner-operated savings and scalable staffed routes. Owner-led routes can show the cash benefit of lean labor, while staffed routes need enough stops to cover wages, payroll taxes, and service recovery. If service slips, retention drops, and labor savings vanish fast.

5

Fleet Operating Costs

Fleet Operating Costs

Fleet cost is the cash left after trucks are legal, insured, fueled, repaired, and financed. In this model, that starts with $450,000 in trucks, $10,000 in maintenance equipment, $2,000 a month in fleet insurance, fuel at 7% of Year 1 revenue, and usage-based maintenance at 3%.

Here’s the quick math: if fuel, repairs, insurance, debt service, and permits run hot, owner distributions shrink fast. The key inputs are fuel per route, repair downtime, insurance claims, debt service, permit costs, spare capacity, and reserve balance. Unexpected repairs hit cash first, so a strong reserve protects take-home pay.

Reserve Before Payouts

Track fleet cost by truck, not just by month. If one route burns extra fuel or causes more downtime, that truck is quietly cutting profit and delaying owner pay. The goal is simple: keep enough cash in reserve so a repair or claim does not force a distribution cut.

- Measure fuel per route weekly.

- Track downtime hours by truck.

- Log every claim and repair.

- Match debt payments to cash flow.

- Hold reserve before owner draws.

Use spare capacity to cover breakdowns without missing pickups. If the reserve is thin, one major repair can wipe out a month of profit. If the reserve is funded first, owner income stays steadier even when maintenance spikes.

6

Compare lean, base, and high owner-income cases

Owner income scenarios

Owner income shifts with route density, pricing, and fleet use. Early losses can still allow salary if funded, while mature scale can support much larger take-home.

| Scenario | Low CaseCash-heavy | Base CaseBreakeven | High CaseMature-scale |

|---|---|---|---|

| Launch model | A Year 1-style ramp can run at a loss, so owner pay is only safe if outside cash covers the burn. | A Year 3-style model can cover overhead and pay a stable owner draw. | A Year 5-style model can support a much stronger owner take-home. |

| Typical setup | About $445,000 revenue and -$457,000 EBITDA, with a small fleet, low route density, and owner pay only if funding covers the burn. | About $2.109 million revenue, $272,000 EBITDA, and 13% margin with breakeven after Month 28 and tighter route density. | About $4.304 million revenue, $1.442 million EBITDA, and 34% margin from denser routes, better pricing, and lower unit costs. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0 - $150,000Funded salary only | $150,000 - $250,000Salary plus draw | $250,000 - $500,000Large take-home |

| Best fit | Use this to stress-test a launch that depends on funding and slower route build. | Use this once the business has passed Month 28 breakeven and can fund routine owner pay. | Use this to test mature operations with strong cash flow and room for debt service and reserves. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Waste Management Porter's Five Forces Analysis

- Waste Management BCG Matrix

- Waste Management Business Model Canvas

- 7 Critical KPIs to Scale Your Waste Management Business

- Waste Management Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Waste Management Profitability

- Running Costs for Waste Management: Operating Expenses

- How Much It Costs To Start A Waste Management Business: $633K CAPEX

- Waste Management Financial Model Template in Excel

- How to Start a Waste Hauling Business in 3-6 Months in the US

- How to Write a Waste Management Business Plan in 7 Steps

- Waste Management Marketing Mix

- Waste Management Marketing Plan

- Waste Management Business Proposal

- Waste Management PESTEL Analysis

- Waste Management Pitch Deck Example Editable PPTX

- Waste Management Business SWOT Analysis

- Waste Management Value Proposition Canvas

Frequently Asked Questions

In this researched model, the owner role is paid $150,000 per year as General Manager / Owner That is wages for active work, not profit distribution EBITDA is negative in Year 1 and Year 2, then reaches $272,000 in Year 3 and $1442 million in Year 5 before debt, taxes, and reserves