Owner income$250k

Owner income$250kHow Much Wind Farm Development Owners Can Make by Year 5

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$250k  Net margin-4% to 92%

Net margin-4% to 92% Revenue for target pay$315k

Revenue for target pay$315k Business difficultyHard

Business difficultyHard

You’re estimating owner income in a capital-heavy wind farm development business, not technician wages or utility salaries In this model, revenue grows from $15 million in Year 1 to $137 million in Year 5, with EBITDA moving from -$67,000 to $1265 million Owner take-home depends on salary, distributions, debt service, reserves, project sales, and whether you sell projects or keep operating equity

Owner income$250kNet margin-4% to 92%Revenue for target pay$315kBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate only, not guaranteed salary, tax advice, or owner distribution advice. It is anchored to the model inputs, including the $250,000 owner-operator salary, $336,000 annual fixed overhead, and payroll ranging from $910,000 to about $2.11 million.

Want to check owner income in the Wind Farm Development model?

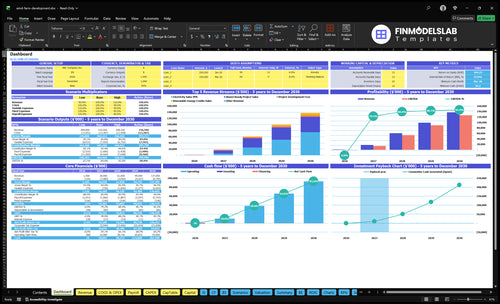

Open the Wind Farm Development Financial Model Template to review dashboard assumptions, revenue build, project costs, payroll, capex, financing, debt service, reserves, scenarios, and owner income. Revenue rises from $15 million to $137 million, EBITDA turns positive after Year 1, breakeven lands in Month 13, payback hits 14 months, and minimum cash is $50,000 in Month 12.

Owner income model highlights

- Owner-income sensitivity charts

- Revenue and EBITDA path

- Reserve and debt planning

Is it more profitable to sell or operate a wind farm project?

For Wind Farm Development, selling shovel-ready projects is usually the faster cash path: modeled revenue is $10 million in Year 2, then $30 million, $40 million, and $50 million by Year 5. Operating the asset can build more long-run revenue because electricity sales and RECs (renewable energy credits) lift Year 5 to $75 million plus $75 million, but it also adds debt, reserve, tax credit, and performance complexity. This is planning logic, not universal advice: cash is faster when you sell, but upside can be higher when you operate.

Sell faster

- $10 million in Year 2

- $30 million in Year 3

- $40 million in Year 4

- $50 million in Year 5

Operate longer

- Electricity sales add revenue

- RECs add extra income

- Year 5 reaches $75 million

- Debt and reserves add risk

How many megawatts does a wind farm need to support owner pay?

You can’t size owner pay from MW alone for Wind Farm Development. The model has to include capacity factor, PPA price, project sale timing, development fees, debt service, reserves, and operating costs, then solve MW from revenue per MW. Here’s the quick math: $336,000 fixed overhead plus $910,000 payroll is $1.246 million a year before debt or ops, so early owner pay has to come from fee revenue before assets scale.

What drives pay

- MW is not enough

- Use revenue per MW

- Include PPA price

- Include capacity factor

Cost floor

- $336,000 overhead yearly

- $910,000 payroll starts

- Total fixed cost: $1.246 million

- Fee revenue must bridge early gap

How much can a wind farm development owner make?

A Wind Farm Development owner can model a $250,000 CEO salary, but the real upside comes from EBITDA, project fees, asset sales, and long-term distributions; track timing against What Is The Current Progress Of Wind Farm Development?. The model shows EBITDA moving from -$67,000 in Year 1 to $126,523 million in Year 5, but owner payouts still depend on reserves, debt, taxes, and board policy.

Owner income view

- CEO salary: $250,000

- Year 1 EBITDA: -$67,000

- Year 2 EBITDA: $14,282 million

- Year 3 EBITDA: $53,897 million

Upside sources

- Year 4 EBITDA: $89,833 million

- Year 5 EBITDA: $126,523 million

- Early developers rely on fees

- Operators seek long-term cash flow

Want the six drivers behind owner income?

1

$1.5M-$137MProject MW Pipeline

More MW in the pipeline lifts development fees, PPA revenue, credit sales, and project sale value.

2

$0-$75MEnergy Price and Offtake

A stronger power purchase agreement locks price and volume, so each megawatt-hour turns into steadier cash.

3

$14.3M-$126.5MWind Yield

Higher wind output spreads fixed costs over more power and pushes EBITDA up fast.

4

Month 13Build Cost

Lower land, permitting, and grid hookup costs pull breakeven forward and keep more margin.

5

14 moCapital Stack

Cheaper debt and tax credits shorten payback and improve owner take-home.

6

$50KReserve Control

Tight overhead and reserve rules protect the $50K cash floor when delays hit.

Wind Farm Development Core Six Income Drivers

Project MW Pipeline

Project MW Pipeline

A larger MW pipeline can spread $336,000 of annual fixed overhead and payroll across more projects, so the same team can support more revenue. In the model, source revenue rises from $15 million to $137 million, with total revenue scaling to $211 million. Bigger pipeline volume can lift owner income, but only if projects actually reach permit, interconnection, financing, and sale close.

One clean check: more MW is not the same as more profit. If permitting stalls, grid tie costs rise, pricing softens, or financing falls through, the pipeline turns into sunk time and working capital demand instead of distributable cash.

Track MW To Cash, Not Just MW To Plan

Measure MW under development, MW permitted, MW financed, and MW sold separately. That shows where revenue can actually convert into development fees, project sales, electricity sales, and credit sales. Here’s the quick math: if the pipeline grows but close rates slip, owner pay drops even while headline MW looks strong.

Track each stage’s cash need, delay days, and close probability. The key control is working capital: a bigger pipeline needs more cash before revenue lands, so watch reserve levels and timing against the $336,000 fixed overhead base and the $15 million to $137 million revenue path.

1

Energy Price And Offtake

Energy Price and Offtake

PPA price is the main driver here because it sets contracted electricity revenue. In this model, electricity sales rise from $0 in Year 1 to $75 million in Year 5, and REC revenue also adds from $0 to $75 million. That is the cash base for debt service, reserves, and owner draw.

The catch is merchant exposure, basis risk, and curtailment. If more output sells outside the contract, cash becomes less predictable, so distributable profit can lag reported revenue. Stronger contracted pricing helps lenders trust the model and makes owner payout timing easier to plan.

Track Contracted Cash, Not Just Megawatts

Model contracted MWh, PPA price, REC price, and the share left merchant. Here’s the quick math: revenue is volume times price, then cut for curtailment and any basis loss. If the contract covers more output at a fixed price, cash flow is steadier and owner pay is easier to forecast.

Track the gap between expected generation and settled revenue each month. Watch these inputs: PPA term, REC sales, merchant share, basis spread, and curtailment hours. If the contract stack weakens, lender confidence falls and distribution plans should be tighter until pricing is reset or more volume is locked in.

2

Wind Resource And Capacity Factor

Capacity Factor Drives Cash

Capacity factor is actual output as a share of maximum possible output, and it drives how many MWh the site sells. This model does not give MW or capacity factor, so treat both as site-specific inputs. In wind, a small change in production can move cash flow enough to change owner distributions after debt service and reserve funding.

What matters is not nameplate size alone. Annual energy production depends on wind resource, turbine availability, wake losses, and downtime. If output slips, electricity sales and credit sales fall first, then distributable cash falls after lenders and reserves are paid.

Measure Output Losses

Build the model from site data, not guesses. Track expected MWh, availability, wake loss, and outage time, then tie them to contracted price and reserve needs. If the site misses output, owner pay drops fast even when the project still looks “profitable” on paper.

- MWh sold

- Availability rate

- Wake loss %

- Downtime hours

- Debt and reserve coverage

3

Development And Interconnection Cost

Development and Grid Costs

Wind farm development cash hits before owner pay. The model shows land and permitting at 30% to 15% of revenue, studies at 40% to 20%, due diligence at 20% to 7%, and legal at 30% to 12%. Cash timing matters as much as total spend.

Interconnection deposits and grid upgrades are not separately provided, so the real cash burn can be higher than the line items show. If permits or utility work slip, reserves get used up first, and owner distributions can move past breakeven even when project profit still looks fine on paper.

Track Reserve Burn Early

Build a month-by-month cash view for land, studies, due diligence, legal, and every interconnection bill. Use project revenue, deposit dates, reserve cash, and delay months as the core inputs. That shows which stage is eating cash and whether the project needs more funding before owner pay starts.

Stress test the utility queue. One extra month can keep cash tied up and delay distributions, so set a minimum reserve and refresh it after each permit or study result. Only size owner draws from cash left after those commitments.

4

Financing And Tax Credit Structure

Financing and Tax Credit Structure

For a wind farm, EBITDA does not equal owner cash. Debt service, sponsor equity, tax equity, and credit assumptions decide what is left for distributions, so a project can look strong on paper and still pay the owner late. The disclosed model shows IRR of 0.24, payback at 14 months, and breakeven in Month 13.

This driver includes leverage, production tax credit assumptions, and investment tax credit assumptions. Those credits can change the split between cash flow, debt paydown, and owner draw. What this estimate hides: tax credits are modeled assumptions and need professional review, not tax advice.

Track Debt, Equity, and Credit Inputs

Measure the cash stack before you forecast owner pay: debt service coverage, sponsor equity, tax equity, and the timing of credit monetization. If debt eats too much cash, distributions slip even when revenue is up. That is the whole game here.

Build two cases at minimum: one with full credit value and one with delayed or reduced credit use. Watch how a small change in leverage or tax credit timing moves Month 13 breakeven and the 14-month payback. If the tax structure is not confirmed, keep owner draws conservative.

5

Operating Cost And Reserve Discipline

Operating Cash vs Owner Pay

Cash on paper is not cash in your pocket. Operating cash flow turns into owner income only after O&M, land leases, insurance, asset management, major maintenance reserves, and working capital. With $28,000/month fixed overhead and $2,000/month general insurance, the business already burns $30,000/month before those reserve needs. That’s why owner pay can lag even when the project looks profitable.

Guard the Reserve Floor

Track a monthly cash bridge: opening cash, operating cash flow, reserve adds, and ending cash. The key input is the $50,000 minimum cash target in Month 12. If reserves are thin, distributions should wait. That discipline protects the project from downtime, repairs, and delay risk, but it also pushes owner draws later.

- Track O&M and lease payments monthly

- Set maintenance reserves before draws

- Separate project cash from owner pay

6

Compare lean, base, and high owner-income cases

Owner income scenarios

Owner income shifts with project timing, PPA ramp, and exit pace. Early years are salary-led; later years can add distributions once EBITDA and cash turn steady.

| Scenario | Low CasePre-breakeven | Base CaseBankable | High CaseDistribution-ready |

|---|---|---|---|

| Launch model | This is the downside case, where owner income stays thin until projects convert and distributions remain delayed. | This is the modeled case, where owner income follows the planned ramp and turns more predictable after breakeven. | This is the upside case, where stronger operating results support higher owner income and faster cash distributions. |

| Typical setup | The model assumes slower project sales, lower PPA pricing, higher development cost, tighter reserves, and little to no early distribution cash. | The base case follows the model's revenue ramp, with project fees from Year 1, power sales starting in Year 2, breakeven in Month 13, and a $250,000 CEO salary. | The high case assumes stronger offtake, higher capacity factor, faster shovel-ready exits, and lower cost percentages across development and advisory work. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Pre-breakeven salary onlyPre-breakeven | $250,000 salaryBankable | Salary plus distributionsDistribution-ready |

| Best fit | Use this to stress test early-year cash and delayed exits. | Use this for lender decks and a standard operating plan. | Use this to test upside from strong sales, better yields, and faster asset exits. |

Planning note: Scenario ranges use researched planning assumptions from the model and are not guaranteed earnings, salary promises, tax advice, or distribution forecasts.

Related Products

- Wind Farm Development Porter's Five Forces Analysis

- Wind Farm Development BCG Matrix

- Wind Farm Development Business Model Canvas

- 7 Key Financial Metrics for Wind Farm Development Success

- Wind Farm Development Business Plan Template in Pre-Written Word

- 7 Proven Strategies to Boost Wind Farm Development Profit Margins

- How Much Does It Cost To Run Wind Farm Development Monthly?

- Wind Farm Startup Costs: $845K Developer CAPEX Before Buildout

- Wind Farm Development Financial Model Template in Excel

- How To Start A Wind Farm Development Business In 12–36+ Months

- 7 Steps to Write a Wind Farm Development Business Plan

- Wind Farm Development Marketing Mix

- Wind Farm Development Marketing Plan

- Wind Farm Development Business Proposal

- Wind Farm Development PESTEL Analysis

- Wind Farm Development Pitch Deck Example Editable PPTX

- Wind Farm Development Business SWOT Analysis

- Wind Farm Development Value Proposition Canvas

Frequently Asked Questions

The modeled owner-operator salary is $250,000 per year, but distributions are not automatic EBITDA is -$67,000 in Year 1, then $14282 million in Year 2 and $126523 million in Year 5 Actual take-home depends on debt service, reserves, taxes if modeled, and whether cash is reinvested