Owner income$619k–$4.65M

Owner income$619k–$4.65MHow Much Can A 35-Room Winery Resort Owner Make?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$619k–$4.65M  Net margin25%–60%

Net margin25%–60% Revenue for target pay$2.5M

Revenue for target pay$2.5M Business difficultyHard

Business difficultyHard

A winery resort owner can make strong money, but only after payroll, property costs, debt service, and reinvestment are covered In this researched 35-room to 40-room model, EBITDA moves from $619,000 in Year 1 to $4653 million in Year 5 as occupancy grows from 40% to 75% That is not guaranteed owner take-home Actual distributions depend on financing, reserve policy, capex timing, and whether the owner also takes a salary

Owner income$619k–$4.65MNet margin25%–60%Revenue for target pay$2.5MBusiness difficultyHardWhat could your winery resort pay you?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

How do you check owner income in the Winery Resort model?

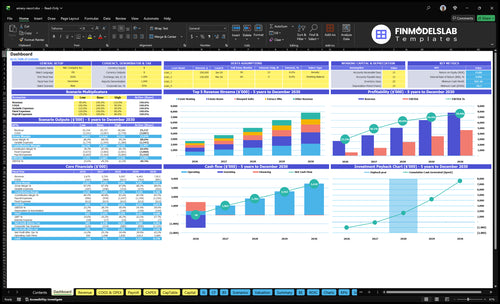

The dashboard shows owner-income outputs, EBITDA, cash runway, breakeven, payback, and scenario charts, plus assumptions tabs for rooms, ADR, occupancy, spa, wine retail, activities, events, COGS, commissions, marketing, wages, capex, debt service, reserves, and salary target. Open the Winery Resort Financial Model Template.

Owner-income model highlights

- Owner take-home outputs

- EBITDA and cash runway

- -$77k in Month 10

- Breakeven in Month 2

- 25-month payback, 70% IRR, 128% ROE

How much revenue does a winery resort need to pay the owner?

A Winery Resort needs enough revenue to create owner-pay capacity after covering operating costs, not just a high top line. In Year 1, the known cost floor is $1.396M before owner pay: $612k fixed overhead plus $784k payroll; use EBITDA, meaning cash profit before financing and taxes, then add target owner income, debt service, reserves, taxes, and reinvestment. For the related operating signal, see What Is The Current Customer Satisfaction Level For Winery Resort?.

Cost Floor

- $612k fixed overhead before owner pay

- $784k Year 1 payroll load

- $1.396M Year 1 cost floor

- $950k payroll by Year 5

Pay Test

- Start with target owner income

- Add debt service manually

- Add reserves, taxes, reinvestment

- Track occupancy from 40% to 75%

Does a winery resort make more if the owner operates it?

A Winery Resort can make more cash with an owner running it, but only if service quality stays high. The model already includes a $130k general manager, $110k head winemaker, $95k executive chef, and $75k spa manager, so replacing one role can lift cash flow fast. Owner-led works best early; hired management is better when you need scale, events, and a strong guest experience.

Cash control

- Cut one salary to lift cash flow.

- Protect service quality or revenue slips.

- Use owner time to watch costs early.

- Keep key staff in food, spa, and wine.

Scale risk

- Burnout risk rises with lodging and vineyard work.

- Events need managers to run smoothly.

- Guest experience matters in luxury stays.

- Front desk and housekeeping still need coverage.

What makes the most money at a winery resort?

Lodging makes the most money at a Winery Resort because it is the base engine: room count moves from 35 to 40, occupancy from 40% to 75%, and blended RevPAR rises from about $120 to $305. Here’s the quick math: events are the biggest listed add-on, but they still range from $60k to $180k, while wine retail goes from $15k to $45k. spa services climb from $12k to $30k and guest activities from $8k to $25k, but there’s no universal winner because wedding rules, food service, positioning, and guest mix change margins.

Room nights drive cash

- 35 to 40 rooms changes scale.

- 40% to 75% occupancy lifts revenue fast.

- $120 to $305 RevPAR changes the base.

- One clean line: rooms set the floor.

Add-ons widen margin

- Events rise from $60k to $180k.

- Wine retail grows from $15k to $45k.

- Spa services move from $12k to $30k.

- Guest activities increase from $8k to $25k.

Want the six income drivers that matter most?

1

$120-$305Occupancy ADR

Room nights and rate set the base, so higher occupancy and ADR lift RevPAR and owner income fast.

2

$60K-$180KEvents Retreats

Private events bring the biggest add-on cash, and they can scale faster than room count.

3

$784K-$950KLabor Mix

Staffing is the biggest fixed cost, so every extra FTE cuts cash that reaches the owner.

4

$1.44MDebt Load

The buildout needs debt and reserves, and those payments come out before owner take-home.

5

$20K-$55KF&B Attach

Spa services and guest activities add low-volume cash that can lift stay spend without many extra rooms.

6

$15K-$45KWine Retail

Wine retail is a useful side stream, but it stays much smaller than rooms and events.

Winery Resort Core Six Income Drivers

Occupancy, ADR, And RevPAR

Occupancy, ADR, and RevPAR

Lodging is the cash base. At 35 to 40 rooms, occupancy rising from 40% to 75% and blended ADR rising from about $300 to $407 lifts RevPAR from roughly $120 to $305 because RevPAR = occupancy × ADR. That swing matters for payroll, debt, and owner pay, especially when the shoulder season weakens.

What this hides: room count alone does not pay the owner. You need the right mix of weekday and weekend rates, plus enough occupied nights. If occupancy drops in slower months, cash gets tight fast even when the resort looks busy on paper.

Improve Yield, Not Just Occupancy

Track occupancy by day, ADR by room type, and RevPAR by segment. Those three numbers show whether demand is coming from low-rate filler nights or high-rate stays that actually support profit and owner draw. Here’s the quick math: more paid nights at higher ADR raises cash without adding equal fixed cost.

Push packages, direct bookings, weekday retreats, and event room blocks to lift midweek yield. A strong mix matters more than raw volume. If shoulder-season demand slips, cut forecasted owner pay early and protect cash for payroll and debt service.

1

Wine Sales Per Guest

Wine Sales Per Guest

Wine retail is separate from lodging, so every extra tasting, bottle sale, and club signup adds cash without needing another room night. In this model, wine revenue rises from $15k in Year 1 to $45k in Year 5. Here’s the quick math: at 50% materials cost in Year 1 and 42% by Year 5, gross profit improves, but it still has to carry heavy labor like the $110k head winemaker and $126k to $168k vineyard crew payroll.

The key inputs are occupied rooms, spend per guest, tasting room traffic, bottle attach rate, and club conversion. If compliance, fulfillment, staffing, or inventory timing slip, cash gets delayed even when sales look strong. One clean rule: more guests only matters if they buy more wine.

Raise Wine Spend Per Guest

Track wine sales per occupied room, not just total wine revenue. Break it into tasting fees, bottle purchases, and club conversion so you can see which step lifts spend. If Year 5 reaches $45k from $15k, the gap should come from better attach rates, not just more foot traffic. That protects margin and helps owner pay.

Use a simple control sheet for inventory timing, cellar stock, and shipping status. Wine materials falling from 50% to 42% helps, but labor still matters. If tasting-room staffing is weak on weekends, or bottles are out of stock when guests are ready to buy, you lose the highest-margin sale right at the point of demand.

- Measure spend per occupied room.

- Split tasting, bottle, and club sales.

- Watch stockouts and shipping delays.

- Forecast labor against guest volume.

2

Events, Weddings, And Retreats

Event Hosting Revenue

Private events, weddings, and retreats can be the resort’s biggest add-on line, growing from $60k to $180k. That revenue is not just venue fees. It also includes room blocks, catering, wine sales, and shoulder-season bookings, so the real test is event contribution after labor and service costs.

High event volume usually raises staffing, coordination, insurance, noise control, and cleanup. A $90k event tent can expand capacity, but only if bookings fill enough dates to pay for it. If events run like one-off rentals, margin gets thin fast. If they bring lodging nights and bottle sales, they lift owner cash.

Bundle Events For Better Margin

Track event count, average venue fee, room-night pickup, catering spend per guest, and wine attach rate. Those inputs show whether each booking adds real cash or just more work. Price on total contribution, not just the venue fee. If an event does not cover labor, insurance, and cleanup, it is too cheap.

- Measure room blocks per event.

- Price for staffing and cleanup.

- Test shoulder-season discounts.

- Cap noise and guest-service risk.

- Forecast cash after event timing.

Use events to fill slow dates, not to crowd peak weekends. The best bookings combine lodging, wine, and dining, so the same guest spend supports more than one profit line. That is how the owner turns a busy calendar into stronger take-home income instead of just higher operating load.

3

Food, Beverage, And Amenities

Food, Beverage, And Amenities Income

This driver adds cash beyond rooms. Spa services are projected at $12k to $30k and guest activities at $8k to $25k, while food and beverage profit depends on attach rate, menu control, staffing, and spoilage. Here’s the quick math: more guests buying meals, wine, spa time, and paid activities raises gross profit, but weak service can wipe out the gain fast.

The cost side matters too. The model uses food and beverage inventory at 80% in Year 1, improving to 72% by Year 5, plus a $95k executive chef and a $75k spa manager. If attach rate stays soft or waste runs high, owner draw shrinks because this income has to cover payroll, not just look good on paper. Guests remember service misses faster than margin math.

Track Attach Rate And Waste

Measure how many overnight guests buy food, spa time, and activities, then compare that to labor and spoilage. Attach rate means the share of guests who add a paid extra. If spa bookings rise but kitchen waste also rises, cash flow can still slip. The goal is simple: sell more add-ons without letting service quality fall.

- Track spa and activity conversion.

- Watch food waste weekly.

- Match staffing to occupancy.

- Control menu breadth and prep.

4

Labor And Management Structure

Labor And Management Structure

Payroll is one of the biggest take-home filters here: $784k in Year 1, $822k in Year 2, $846k in Year 3, then $950k in Years 4 and 5. That is about $166k, or 21%, more annual cash pressure before taxes, reserves, and owner pay. This covers the general manager, winemaker, chef, spa manager, front desk, housekeeping, and vineyard crew.

The tradeoff is simple. Owner-operated roles save cash, but service risk rises. Hired management protects scale and events, but it locks in higher fixed cost. Labor works best when staffing follows occupancy, arrivals, tastings, and the event calendar, because idle labor drains cash even when the property looks busy.

Staff to Demand, Not Habit

Build schedules from demand signals, not from a fixed roster. Track room occupancy, check-ins, tastings, spa bookings, and event dates, then set labor hours by day and department. Here’s the quick math: moving payroll from $784k to $950k adds $166k of annual cost, so every extra hour must protect guest experience or event margin.

- Match shifts to arrivals.

- Cross-train front desk and events.

- Separate fixed roles from flex hours.

- Review labor weekly by department.

What this estimate hides: thin event staffing can hurt service fast and damage repeat bookings, while overstaffing cuts margin even when rooms are full. The goal is not the lowest payroll; it is the best payroll mix for rooms, spa, tasting, and event work actually sold.

5

Debt Service And Capital Reserves

Debt Service And Capital Reserves

Accounting profit is not owner cash. For this resort, distributable cash comes after debt service, maintenance, room refreshes, vineyard upkeep, equipment replacement, insurance, and reserve funding. The model also shows $144M of early capex across winery equipment, spa buildout, kitchen, furnishings, irrigation, the event tent, vehicles, and IT, so the cash call is heavy before the business can pay the owner well.

Here’s the quick math: the model’s minimum cash is -$77k in Month 10, and payback is 25 months. But debt service is not supplied, so owner take-home must be stress-tested against the loan schedule, reserve policy, and replacement timing. Profit on paper can still mean zero draw if debt or capex eats the cash.

Track Cash Before Owner Draw

Measure free cash flow after debt service and reserve deposits, not just EBITDA or net income. Build the forecast from loan payment, maintenance capex, refresh cycles, insurance, and vineyard spend, then check the lowest cash month. If cash dips near zero, owner pay should wait until reserves are funded.

Use a simple control list:

- Debt schedule by month

- Capex reserve by asset type

- Minimum cash floor set in advance

- Owner draw only after reserves

6

Compare low, base, and high winery resort owner-income scenarios

Owner income scenarios

Room count, occupancy, rates, and event income change owner take-home fast. Debt service, reserves, taxes, and reinvestment still cut the amount that reaches the owner.

| Scenario | LowDownside case | BaseBase case | HighUpside case |

|---|---|---|---|

| Launch model | This is the lower earnings path if opening demand stays soft and room fill runs below plan. | This is the modeled middle path with steady demand and stronger room rates. | This is the stronger earnings path if occupancy, pricing, and non-room sales all land near the top of plan. |

| Typical setup | About 35 rooms, 40% occupancy, RevPAR near $120, extra income around $95k, EBITDA about $619k, payroll about $784k, and fixed overhead about $612k. | About 37 rooms, 60% occupancy, RevPAR near $210, extra income around $184k, EBITDA about $2.478M, and payroll about $846k. | About 40 rooms, 75% occupancy, RevPAR near $305, extra income around $280k, EBITDA about $4.653M, and payroll about $950k. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $619k EBITDADownside earnings | $2.478M EBITDAModeled base | $4.653M EBITDAUpside case |

| Best fit | Use this to stress-test launch-year cash flow and lender pressure. | Use this as the normal ramp case for budgeting and hiring. | Use this to test peak demand, staffing strain, and reinvestment needs. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Winery Resort Porter's Five Forces Analysis

- Winery Resort BCG Matrix

- Winery Resort Business Model Canvas

- 7 Critical Financial Metrics for a Winery Resort

- Winery Resort Business Plan Template in Pre-Written Word

- 7 Financial Strategies to Boost Winery Resort Profitability

- How Much Does It Cost To Run A Winery Resort Each Month?

- Winery Resort Startup Cost: $144M CAPEX For A 35-Room Launch

- Winery Resort Financial Model Template in Excel

- How To Open A Winery Resort: 18–36+ Month Launch Roadmap

- How to Write a Winery Resort Business Plan in 7 Steps

- Winery Resort Marketing Mix

- Winery Resort Marketing Plan

- Winery Resort Business Proposal

- Winery Resort PESTEL Analysis

- Winery Resort Pitch Deck Example Editable PPTX

- Winery Resort Business SWOT Analysis

- Winery Resort Value Proposition Canvas

Frequently Asked Questions

A winery resort owner’s take-home depends on cash left after debt service, reserves, taxes, and reinvestment In this model, EBITDA rises from $619k in Year 1 to $4653M in Year 5 That is owner-income capacity before financing and distributions, not a guaranteed salary