Owner income$83k-$116k

Owner income$83k-$116kHow Much Zero Entry Pool Construction Owners Can Make: $145K-$167M

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$83k-$116k  Net margin57%-72%

Net margin57%-72% Revenue for target pay$900k

Revenue for target pay$900k Business difficultyHard

Business difficultyHard

A zero entry pool construction owner can plan around $145,000 in modeled annual owner compensation, with additional upside only if the business distributes profit The researched assumptions show $5215M revenue and $2968M EBITDA in Year 1, rising to $22965M revenue and $16587M EBITDA in Year 5 EBITDA means profit before interest, taxes, depreciation, and amortization If the owner drew salary plus all EBITDA, pre-tax take-home would range from $3113M to $16732M, but that ignores taxes, debt service, warranty reserves, retained cash, and reinvestment

Owner income$83k-$116kNet margin57%-72%Revenue for target pay$900kBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income depends on pricing, labor mix, taxes, debt, reserves, and project timing. This is not guaranteed salary, tax advice, or owner distribution advice.

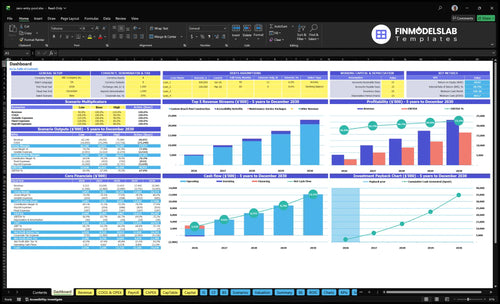

Can you see owner income clearly in the Zero Entry Pool Construction model?

Yes—this dashboard shows revenue, EBITDA, owner compensation, cash need, breakeven, payback, and IRR. Open the Zero Entry Pool Construction Financial Model Template for the full view.

Owner-income model highlights

- Owner compensation is clear

- Revenue: $5,215M to $22,965M

- EBITDA: $2,968M to $16,587M

- Tabs cover assumptions and cash flow

- Tests price, volume, costs

How much profit can a zero entry pool construction owner make?

A Zero Entry Pool Construction owner can make $145,000/year in modeled salary, while the business shows $2.968M EBITDA in Year 1, rising to $8.961M in Year 3 and $16.587M in Year 5; for the operating drivers behind that, see What Are The 5 KPI Metrics For Zero Entry Pool Construction Business?. Profit depends on whether you mean salary, EBITDA, or cash you can actually distribute after taxes, debt, warranty reserves, and reinvestment.

Modeled profit

- $145,000 owner salary modeled annually

- $2.968M EBITDA in Year 1

- $8.961M EBITDA in Year 3

- $16.587M EBITDA in Year 5

Profit levers

- Revenue grows $5.215M to $22.965M

- Project value rises $112,500 to $144,550

- COGS drops from 26% to 20%

- Keep overhead controlled as projects scale

What margins do zero entry pool builders make?

Zero Entry Pool Construction can start at 74% gross margin after subcontractor labor, engineering, raw materials, and equipment procurement, then climb to 80% by Year 5 as direct costs fall from 26% to 20%; see What Are Zero Entry Pool Construction Operating Costs? for the cost base. On $5.215M Year 1 revenue, every 1% cost overrun cuts profit by about $52,150, so scope control matters from day one.

Margin profile

- 74% gross margin at start

- 80% by Year 5

- Direct costs fall from 26% to 20%

- Project-by-project pricing drives returns

Cost pressure points

- Excavation complexity raises cost fast

- Slope design adds labor risk

- Finish, decking, and drainage move budgets

- Rework and inspections eat profit

Does a zero entry pool builder make more as owner-operator or contractor?

For Zero Entry Pool Construction, the owner-operator model usually protects early cash better. The model already carries a $145,000 CEO and Principal Designer role, while a sales-and-project-management owner can scale faster only if they fund $95,000 senior project managers and keep field execution tight. By Year 4, staffing rises from 10 FTE to 20 FTE, so profit only grows if subcontractor reliability, inspection timing, quality control, and warranty callbacks stay under control.

Owner-operator cash edge

- $145,000 CEO role is already baked in

- Keep early overhead lighter

- Protect cash before scale

- Works best in Year 1

Scale only if ops hold

- $95,000 senior PMs add fixed cost

- Headcount grows from 10 to 20 FTE

- EBITDA rises from $2.968M to $16.587M

- That needs lower COGS and CAC

Want the six drivers that move owner income most?

1

$5.22MProject Volume

More completed pool jobs lift Year 1 revenue to $5.215M, and that is the biggest swing in owner take-home.

2

$112.5KContract Value

Each custom build starts around $112.5K in Year 1 revenue, so price and scope changes move cash fast.

3

74%Gross Margin

Holding job margin near 74% keeps more of each contract after labor, materials, and fees.

4

450hCrew Output

At 450 billable hours for a custom build, better scheduling and fewer delays let the same team finish more work.

5

$4.5KLead Quality

Keeping customer acquisition cost near $4.5K helps more of the marketing budget turn into booked work.

6

$186.6KOverhead Control

Keeping annual fixed overhead near $186.6K protects EBITDA and helps cover owner pay without draining cash.

Zero Entry Pool Construction Core Six Income Drivers

Annual Completed Projects

Annual Completed Projects

Completed and paid projects are what turn your pipeline into owner income. At about $5.215M in Year 1 revenue, this model is roughly 46 custom-equivalent projects at $112,500 each; by Year 5, $22.965M is about 159 projects at $144,550 each. That only helps if excavation, gunite, inspections, finishes, and project management keep pace.

More completions lift EBITDA only when margin and quality hold. If jobs slip into later periods, revenue and cash move back too, and owner pay gets delayed. In practice, project count, average contract value, gross margin, and cycle time decide whether completed work becomes distributable profit or just backlog on paper.

Track job flow by stage

Measure starts, completions, invoices sent, and cash collected each month. Here’s the quick math: if the crew can’t clear excavation, gunite, inspections, and finishes on schedule, completed jobs fall even when sales stay strong. That’s why the real bottleneck is often production, not lead volume.

Use a stage-by-stage forecast for each pool and track days in process, change orders, and rework. A higher completed-project count only improves owner income when pricing covers the extra labor, subcontractor load, and management time. Otherwise, more volume can raise stress faster than profit.

1

Average Contract Value

Average Contract Value

Average contract value is the revenue per pool project. In this model, custom project revenue rises from $112,500 in Year 1 to $144,550 in Year 5, and accessibility retrofit revenue rises from $39,600 to $53,000. Higher scope lifts owner income only when price covers slope entry design, decking, finishes, water features, accessibility upgrades, drainage, and site complexity.

Here’s the quick math: if you sell more complex jobs but miss labor, material, or subcontractor load, gross profit drops fast. Bigger contracts help cash and pay, but only when estimate accuracy stays tight and change orders are billed cleanly. More scope should mean more margin, not just more revenue.

Price to the Full Scope

Track billable hours, price per hour, and actual cost by job. Break estimates into design, excavation, plumbing, decking, finishes, accessibility upgrades, and drainage so the contract price matches the work. If retrofit jobs run from $39,600 to $53,000, the spread should reflect added complexity, not guesswork.

- Compare estimate vs. actual labor hours.

- Track material overruns by job.

- Bill every approved change order.

- Watch subcontractor cost as a share.

The owner’s take-home rises when each larger contract still leaves room for overhead and draw. If estimates miss by even a small share on high-ticket builds, the lost dollars hit profit, not just revenue.

2

Job-Level Gross Margin

Job-Level Gross Margin

Job-level gross margin is the money left after direct job costs but before overhead, taxes, and owner pay. In this model, direct costs run from 26% of revenue in Year 1 to 20% in Year 5, so gross margin rises from 74% to 80%. That margin is what funds EBITDA and distributions, so even small leakage hits the owner’s take-home fast.

This includes excavation, plumbing, steel, shotcrete or gunite, plaster, decking, equipment, labor, subcontractors, permits, and change orders. Here’s the quick math: on $1,000,000 of revenue, a 26% direct-cost rate leaves $740,000 gross profit; at 20%, it leaves $800,000. The gap is $60,000 per million in revenue before overhead.

Control Direct Costs Job by Job

Track gross margin by project, not just by month. Split estimates into labor, materials, equipment, and subcontractors, then compare budget to actual at closeout. If change orders, permit delays, or rework are not captured, margin leaks straight out of owner income. The goal is to keep the direct-cost ratio near the model path from 26% to 20%.

Price every scope item: excavation, steel, plumbing, finishes, and access features. Lock in supplier quotes early, document change orders fast, and review each job’s gross profit before paying drawings or bonuses. One clean rule: if the job margin slips, the owner gets paid less even when revenue looks strong.

3

Crew And Subcontractor Productivity

Crew and Subcontractor Productivity

When crews and subcontractors move cleanly, each pool finishes sooner and costs less. In this model, subcontractor labor and specialized engineering fall from 18% of revenue in Year 1 to 14% in Year 5, so better execution lifts gross margin and cash available for owner pay. If inspections slip or rework stacks up, completed projects drop and cost per job goes up.

Senior project manager staffing rises from 10 FTE to 20 FTE, which supports scale but adds payroll. Faster only helps when quality holds, because a rushed zero-entry build can turn into callbacks, delays, and lost profit.

Track rework, delays, and handoffs

Measure labor hours per job, rework, inspection wait time, and days from excavation to final sign-off. Those inputs tell you if productivity is turning into margin or just more payroll. Use the same checklist on every site, so subcontractors know the standard and project managers catch misses early.

Hold each trade to a schedule and a quality check. If a crew misses a handoff or fails inspection, fix the process fast and document it. The goal is simple: finish more jobs with the same overhead and protect the gross profit that funds owner draws.

4

Lead Quality And Close Rate

Lead Quality And Close Rate

For zero-entry pool construction, leads only matter when they become booked, profitable work. The inputs are lead source, proposal volume, close rate, CAC, and gross profit per booked job. Here, annual marketing spend rises from $45,000 in Year 1 to $85,000 in Year 5, while CAC improves from $4,500 to $3,500, so better-fit leads must convert faster or the extra spend just buys more sales effort.

Referrals, qualified homeowners, accessibility-driven buyers, and design consultations should lift close rate and protect margin. Low-fit leads waste design time and push underpriced estimates, which drags down owner pay even if top-line inquiries look busy. The real test is booked gross profit per lead source, not lead count.

Track Profit by Source

Here’s the quick math: dropping CAC from $4,500 to $3, 500 cuts acquisition cost by about 22%. Use that gain on sources that already show intent, like referrals and design consultations, because those leads are more likely to close and recover sales time.

- Track close rate by source.

- Rank booked gross profit.

- Reject low-fit design leads.

- Review CAC monthly.

If close rate stays flat, a bigger marketing budget just creates more quotes, not more income. If the buyer is price-only or not ready to build, design hours leak out before cash comes back, and that hits take-home pay fast.

5

Overhead And Reserve Discipline

Overhead and reserve discipline

Operating profit is not the same as distributable owner income. In this business, fixed overhead is $15,550 per month or $186,600 per year before payroll and annual marketing. Add $145,000 owner compensation plus project managers, operations, drafting, and maintenance staff, and the cash left for the owner can shrink fast even when jobs look profitable on paper.

Here’s the quick math: insurance, licensing, vehicles, equipment, software, financing, warranty callbacks, and retained cash all come out before true take-home pay. That matters because a pool defect can hit after the client has already paid. One warranty event can erase a month’s margin, so reserve discipline is part of income, not just accounting.

Track cash after overhead

Measure monthly fixed overhead, payroll, and reserve draws separately from project profit. The owner should know how much cash remains after $15,550 of fixed overhead, staffing, and marketing are paid, plus what is held back for callbacks and repair risk. If that number is thin, owner pay is fragile.

- Track overhead burn each month

- Separate warranty reserves from profit

- Watch payroll growth by role

- Review cash after each job closeout

Keep a simple reserve rule tied to completed work, not optimism. If a defect, leak, or finish issue shows up after payment, the reserve keeps the company from raiding operating cash or delaying pay. Cash discipline protects owner income when revenue has already been booked but the real cleanup bill has not.

6

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Owner income shifts with project mix, CAC, staffing load, and margin. The low, base, and high cases show how stronger lead flow and higher margin support larger take-home.

| Scenario | Low CasePlanning case | Base CasePlanning case | High CasePlanning case |

|---|---|---|---|

| Launch model | This is the lower owner-income path built from Year 1 assumptions. | This is the modeled middle path for owner income. | This is the stronger owner-income path built from Year 5 assumptions. |

| Typical setup | Year 1 revenue is $5.215M with $2.968M EBITDA, 74% gross margin, 70% contribution after variable fees, $45,000 marketing, $4,500 CAC, and about 46 custom-equivalent projects. | Year 3 revenue is $13.433M with $8.961M EBITDA, 77% gross margin, 73.7% contribution, $65,000 marketing, and $4,000 CAC. | Year 5 revenue reaches $22.965M with $16.587M EBITDA, 80% gross margin, 77.4% contribution, $85,000 marketing, and $3,500 CAC. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $145,000Conservative planning case | Salary plus distributionsCore planning case | Larger salary plus distributionsUpside planning case |

| Best fit | Use this to test cash pressure and the owner's floor if project flow is choppy. | Use this as the working plan if demand, pricing, and throughput track the model. | Use this to test upside if lead costs fall and the team keeps capacity full. |

Planning note: Planning cases use modeled assumptions and are not guaranteed earnings, salary promises, tax advice, or approved distributions.

Related Products

- Zero Entry Pool Construction Porter's Five Forces Analysis

- Zero Entry Pool Construction BCG Matrix

- Zero Entry Pool Construction Business Model Canvas

- What Are The 5 KPI Metrics For Zero Entry Pool Construction Business?

- Zero Entry Pool Construction Business Plan Template in Pre-Written Word

- How Increase Zero Entry Pool Construction Profitability?

- What Are Zero Entry Pool Construction Operating Costs?

- Zero Entry Pool Construction Startup Costs: $664K Cash Need

- Zero Entry Pool Financial Model Template in Excel

- How To Start A Zero Entry Pool Construction Business In 90–180 Days

- How To Write A Business Plan For Zero Entry Pool Construction?

- Zero Entry Pool Construction Marketing Mix

- Zero Entry Pool Construction Marketing Plan

- Zero Entry Pool Construction Business Proposal

- Zero Entry Pool Construction PESTEL Analysis

- Zero Entry Pool Construction Pitch Deck Example Editable PPTX

- Zero Entry Pool Construction Business SWOT Analysis

- Zero Entry Pool Construction Value Proposition Canvas

Frequently Asked Questions

The model includes $145,000 per year for the CEO and Principal Designer role Business profit is separate: EBITDA is $2968M in Year 1 and $16587M in Year 5 Actual take-home depends on taxes, debt service, reserves, and how much profit the company safely distributes