How Much Can An Accent Reduction Training Owner Make? $120K+

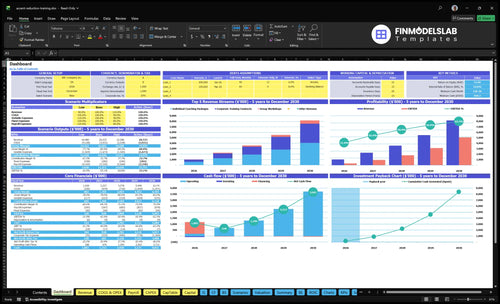

At the researched assumptions, accent reduction training business owner income starts with a modeled $120,000 founder salary The business also produces $1028 million in Year 1 revenue and $328,000 in EBITDA, which means the owner may have room for distributions only after taxes, reserves, debt service, and reinvestment In the mature case, revenue reaches $8174 million and EBITDA reaches $5093 million The model breaks even in Month 5 and reaches payback in Month 9, but those are planning outputs, not promises

Owner income$120kNet margin71%Revenue for target pay$169kBusiness difficultyHard

Want to see what drives owner income most?

1

Package Pricing

$125-$225

Hourly rates run from $125 to $150 for individual work and $180 to $225 for corporate work, so price lifts move take-home fast if demand holds.

2

Staffing Model

1-5 FTE

Senior coach capacity grows from 1 to 5 FTE, and that only helps owner income if utilization stays high enough to cover the added salary load.

3

Client Cost

$150→$120

Customer acquisition cost falls from $150 in Year 1 to $120 in Year 5, but the win matters most if the $45K to $150K marketing budget keeps producing steady leads.

4

Capacity Use

3.5-4.5h

Billable hours per active customer rise from 3.5 to 4.5 a month, which spreads fixed cost over more revenue, but only when coach schedules stay full.

5

Delivery Mix

65%-45%

The mix shifts from 65% individual coaching to 35% corporate contracts and 40% group workshops by Year 5, which changes blended margin and pricing power.

6

Overhead Discipline

$4.7K

Fixed overhead totals about $4.7K a month across tech, insurance, coworking, legal, curriculum, and internet, so any savings here drops straight to EBITDA.

Want to test your own owner-pay case?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, gross margin, labor, overhead, reserves, and target pay.

!

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income changes with revenue, margins, payroll, debt, and reinvestment.

How do you check owner income in the financial model?

How many accent reduction clients do you need to make money?

To reach $1.028 million in annual revenue, the Accent Reduction Training Program needs about 8,341 billable hours at a blended rate of roughly $123 per hour from 65% individual at $125, 15% corporate at $180, and 20% group at $75. If you want the cost side too, see What Are Operating Costs For Accent Reduction Training Program? At 35 billable hours per active customer each month, that is about 20 active customers, and a $45,000 marketing budget at $150 CAC can fund about 300 acquired customers.

Revenue math

$123 blended hourly price

8,341 hours a year

695 hours a month

$1.028 million revenue target

Customer math

20 active customers at 35 hours each

$45,000 marketing budget

300 customers at $150 CAC

Repeat buying changes the count

How much revenue does an accent reduction training business need to pay the owner?

The Accent Reduction Training Program can support a $120,000 founder salary in Year 1 at $1.028 million revenue. With $328,000 in EBITDA (profit before interest, taxes, depreciation, and amortization), the margin is about 31.9% ($328,000 ÷ $1.028 million), but salary and profit are not the same thing. If the owner also wants an extra $100,000 distribution, the rough extra revenue need is about $313,000 before taxes and reserves.

Founder pay math

$1.028 million Year 1 revenue

$328,000 EBITDA

31.9% EBITDA margin

$120,000 founder salary

Cash guardrails

$4,700 monthly overhead

$56,400 yearly overhead

$45,000 Year 1 marketing

$313,000 extra revenue for $100,000

Can an accent reduction training business scale beyond the owner?

Yes, but scaling the Accent Reduction Training Program changes margins, quality control, and management load fast. In the model, staffing rises from 10 FTE in Year 1 to 50 FTE in Year 5 at $75,000 per FTE, founder pay stays at $120,000, and revenue grows from 1028 million to 8174 million. Here’s the catch: coach pay still runs at 180% to 160% of revenue, so hiring adds training and supervision work before it lifts owner take-home.

What scales

10 FTE to 50 FTE

$75,000 per FTE salary

Corporate and group delivery expand

Revenue rises sharply in the model

What gets harder

180% to 160% of revenue

More training and supervision

Consistency becomes harder to manage

Owner take-home improves later

Key Takeaways

Pricing drives margin before cost cuts do.

Client acquisition turns spend into billable packages.

Owner capacity caps revenue without delegation.

Cash reserves must cover the $836,000 Month 2 need.

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income rises as the mix shifts from individual coaching to corporate and group work. Year 1, Year 3, and Year 5 show the lean ramp, core case, and scale path.

Low, base, and high owner-income cases for the model.

Scenario

Low CaseM5 break-even

Base CaseM9 payback

High Case$836k cash

Launch model

This is the lean ramp path: Year 1 revenue is $1.028M and EBITDA is $328k.

This is the modeled core path: Year 3 revenue reaches $3.578M and EBITDA reaches $1.804M.

This is the stronger path: Year 5 revenue reaches $8.174M and EBITDA reaches $5.093M.

Typical setup

Individual coaching still drives most sales, marketing is $45k, CAC is $150, and the founder salary stays at $120k.

The mix shifts toward corporate and group work, marketing reaches $90k, CAC is $135, and senior coach capacity reaches 3 FTE.

Corporate and group work take a bigger share, marketing reaches $150k, CAC falls to $120, and senior coach capacity reaches 5 FTE.

Cost drivers

Individual mix

$45k marketing

$150 CAC

founder salary

1 senior coach FTE

$90k marketing

$135 CAC

3 senior coach FTE

higher corporate mix

50.4% margin

$150k marketing

$120 CAC

5 senior coach FTE

higher group mix

62.3% margin

Owner income rangeBefore owner reserves

$328kLean ramp

$1.8MCore model

$5.1MScale upside

Best fit

Use this to stress-test the first year's cash use and sales ramp.

Use this as the main planning case for staffing, pricing, and cash control.

Use this to test upside if demand, retention, and coach capacity all hold up well.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Accent Reduction Training Program Core Six Income Drivers

Package pricing and structure

Package Pricing Mix

Package pricing is the fastest way to move gross margin here because each sale has a fixed rate and a fixed block of hours. Year 1 pricing is $125 per hour for individual coaching, $180 per hour for corporate training, and $75 per hour for group workshops. The owner’s income rises when higher-priced packages close without hurting conversion or client results.

Here’s the tradeoff: if prices move up faster than buyer trust, close rates can slip and revenue can stall. The business also needs enough billable hours to fill each package. With 40 individual billable hours, 80 corporate hours, and 20 workshop hours, the real test is package mix, not just sticker price.

Track Price, Close Rate, and Hours

Measure three things on every offer: package price, close rate, and delivered hours. That shows whether a higher fee actually lifts owner pay or just slows sales. If higher pricing lowers closes, the margin gain can disappear fast.

Track revenue per booked hour

Watch close rate by package

Compare hours sold to hours delivered

Test price only after outcomes hold

Group and corporate delivery mix

Group and Corporate Mix

This mix matters because corporate hours price at $180, above $125 individual and $75 group hours. A Year 1 corporate contract unit with 80 hours is about $14,400; a group block with 20 hours is about $1,500. As corporate hours rise to 100 and group hours to 30, revenue per delivery block improves, but buyer fit matters because not every client wants the same format.

For the owner, this mix can lift take-home income by spreading revenue across more than one sales motion and reducing dependence on owner-led one-on-one sessions. The tradeoff is lower personalization, so if group work hurts outcomes or close rates, the lower $75 rate can thin profit fast.

Shift Hours Toward Higher-Rate Blocks

Track revenue by format, not just total hours. Watch corporate hours, group hours, close rate, prep time, and repeat contracts. The key test is whether more group seats lift revenue per teaching block without cutting results. If corporate delivery rises from 80 to 100 hours, that is a 25% increase; group hours from 20 to 30 is a 50% increase.

Price by hour and format.

Measure close rate by buyer type.

Cap custom prep on group work.

Protect owner time from one-on-ones.

Client acquisition and conversion

Client acquisition and conversion

This driver turns marketing into paid accent coaching packages. With $45,000 of Year 1 marketing at $150 CAC (customer acquisition cost), the business buys about 300 customers. By Year 5, $150,000 at $120 CAC implies about 1,250 customers. More qualified buyers mean more revenue and faster owner payback; weak leads fill consult calls but do not pay bills.

Track lead volume, consult-to-close rate, and repeat buying. CAC payback gets better when package price, completion, and second purchases rise, because the same marketing dollar creates more gross profit. One clean metric matters most: if CAC rises faster than closed package value, cash flow tightens and owner draw gets delayed.

Measure CAC by channel

Use each channel’s CAC, consult show rate, and close rate to see where spend turns into paid work. If a channel books calls but not packages, cut it fast. Here’s the quick math: $45,000 / $150 = 300 customers in Year 1, and $150,000 / $120 = 1,250 customers in Year 5. Better conversion makes the same spend buy more income.

Track CAC by source.

Track consult-to-close weekly.

Track completion and repeats.

Drop weak lead sources fast.

What this estimate hides is quality. A lower CAC is not good if clients quit early or never buy again. The owner wins when acquisition stays tied to paid package close rate, not just booked calls.

Operating costs and reserves

Operating costs and reserves

For an accent reduction training program, this driver is the cash load from $4,700/month of fixed overhead plus marketing that runs $45,000 in Year 1 and climbs to $150,000 by Year 5. Add launch spend like $15,000 for website and booking, $10,000 for curriculum digitization, and $25,000 for a learning app prototype, and the owner’s pay gets squeezed fast if revenue lags.

The key issue is reserves. The disclosed minimum cash need is $836,000 in Month 2, so underfunding can force the owner to cut pay during ramp-up even if sales are growing. One clean rule: no reserve, no stable draw.

Protect cash before you protect pay

Track monthly burn, not just sales. Use a simple cash forecast with fixed overhead, marketing, and launch spend separated from coach payroll so you can see when owner income is exposed. If marketing rises faster than bookings, the cash gap widens before profit does.

Watch cash runway each month.

Stress test the $836,000 cash floor.

Delay owner draws if reserves dip.

Also, review reserve coverage against the Year 1 spend pattern. If onboarding or client acquisition takes longer than planned, the business may need to keep cash on hand longer than expected, and that directly limits how much the owner can take home.

Staffing and delegated coaching

Delegated Coaching Capacity

Hiring coaches lifts delivery capacity, but it only helps the owner if each new seat stays productive. Senior Speech Coach staffing grows from 10 FTE to 50 FTE at $75,000 per FTE, so coach payroll rises from $750,000 to $3.75 million before support labor. If training systems are weak, more staff can add cost faster than revenue.

This driver includes coach headcount, 0.5 to 1.0 FTE for Operations and Sales Manager support, 0.5 to 2.5 FTE for admin help, and coach per-session pay running 180% in Year 1 and 160% in Year 5. Owner take-home improves only when added billings beat labor, supervision, and no-show drag.

Track Revenue per Coach FTE

Measure billable hours, utilization, cancellations, and revenue per coach FTE every month. Here’s the quick math: if headcount rises but utilization falls, the extra payroll turns into margin loss, not growth. Keep one scorecard for coached hours sold, coached hours delivered, and supervision time so you can see which hires pay back.

Use simple hire gates before adding staff.

Track billable hours per coach.

Watch close rates by coach.

Price for supervision time.

Review payback after each hire.

Cut nonbillable prep fast.

Owner capacity and utilization

Owner Capacity and Utilization

In a one-on-one-heavy accent coaching model, capacity is the revenue ceiling. The key inputs are billable hours per active customer, hours per corporate contract, and the gap between scheduled and delivered time. Average billable hours rise from 35 per month in Year 1 to 45 in Year 5, but cancellations, prep, and no-shows make real capacity lower than the calendar.

Here’s the quick math: if the owner can’t sell more hours than coaches can deliver, revenue stalls before demand does. A package at 40 billable hours or a corporate block at 80 to 100 hours only helps if utilization stays high. One lost hour is lost revenue, not delayed revenue, so underfilled schedules hit take-home pay fast.

Track Delivered Hours First

Measure scheduled hours, delivered billable hours, cancellation rate, and prep time each week. The goal is simple: raise delivered hours per active customer from 35 toward 45 without adding idle gaps. If follow-up work, reschedules, or admin eat too much time, margin falls even when sales look strong.

Protect time blocks with firm booking rules.

Use deposits to cut no-shows.

Bundle corporate sessions to reduce switch costs.

If utilization slips, forecast fewer billable hours and slower owner draws; if it improves, the same coach team can support more revenue before headcount has to rise.