How Much Adventure Race Planning Owners Make: $100K Plus Profit

You’re trying to see if race production can pay the owner, not just cover a fun event In this five-year model, owner pay is modeled as a $100,000 annual founder salary, with business EBITDA growing from $3,000 in Year 1 to $1066 million in Year 5 before personal taxes, reserves, reinvestment, debt service, or distributions

Owner incomeYear 1: $100kNet margin1% to 60%Revenue for target pay$262kBusiness difficultyHard

Want the six biggest income drivers?

1

Registrations

$225K-$1.36M

At 1,500 registrations at $150 and 8,000 at $170, this is the core revenue line and the fastest path to owner profit.

2

Event Mix

Editable

Because race count isn't set, more events or a better format mix can lift revenue without a matching jump in fixed cost.

3

Sponsorships

$25K-$126K

Five to 18 packages at $5K to $7K add high-margin cash, so even one extra sponsor can move take-home.

4

Add-ons

$47K-$304K

Merch, photos, training, concessions, and VIP passes scale fast and usually carry better margin than core race fees.

5

Direct Costs

$27K-$134K

Event ops and participant supplies take a real bite, so tighter setup and buying keep more revenue after race-day spend.

6

Labor Mix

20%-15%

Contract staff falls from 20% to 15%, but payroll still grows and cancellation risk can push the Month 24 cash trough to $852K, so thin reserves can cut owner draws fast.

Want to test your owner pay target?

Owner income calculator

Estimate owner take-home and the gap to your target pay from revenue, margin, costs, reserves, and pay goal.

!

Planning note: This is a researched planning estimate only. Actual owner income depends on revenue, margins, payroll, taxes, reserves, and debt. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see the owner-income forecast in Adventure Race Planning?

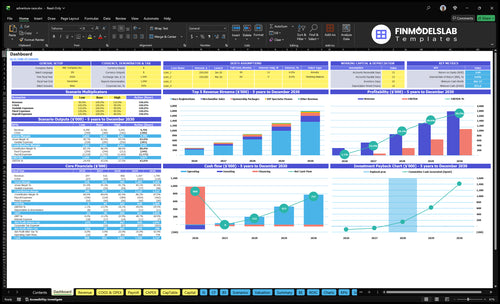

The dashboard in the Adventure Race Planning Financial Model Template shows owner take-home, assumptions, event economics, revenue, costs, scenario tests, and cash flow; open it to review the model. Charts run from 1,500 to 8,000 registrations, $297,000 to $179 million revenue, $3,000 to $1,066 million EBITDA, breakeven in Month 14, payback in 30 months, and minimum cash of $852,000 in Month 24.

Owner-income model highlights

Owner take-home output

Registrations: 1,500 to 8,000

Revenue: $297k to $179M

EBITDA: $3k to $1,066M

Breakeven in Month 14

Payback: 30 months

Cash floor: $852k

Are adventure races profitable after expenses?

Yes, Adventure Race Planning can make money, but the early margin is tight. In the researched case, Year 1 EBITDA is $3,000 on $297,000 revenue, and the startup-cost side is laid out here: What Is The Estimated Cost To Open Your Adventure Race Planning Business?. Safety, insurance, timing, transport, and permits should stay in the budget, not get treated like easy cuts.

Year 1 margin

$3,000 EBITDA on $297,000 revenue

About 1% EBITDA margin

Direct race ops and supplies: 90% in Year 1

Marketing and contract race-day staff: 70% in Year 1

Year 5 shift

$1066 million EBITDA on $179 million revenue

Reported margin: about 596%

Direct race ops and supplies: 75% in Year 5

Marketing and contract race-day staff: 55% in Year 5

Can you make a living organizing adventure races?

Yes, you can make a living with Adventure Race Planning, but the $100,000 founder salary in the model is a planning assumption, not guaranteed income. With month 14 breakeven and a 30-month payback, cash discipline has to hold early, especially when seasonal events create uneven cash flow. The main risks are weather, refunds, permitting delays, low registration, and sponsor dependence.

Cash reality

$100,000 is a model input.

It is not guaranteed take-home pay.

Month 14 is breakeven.

30 months is payback.

What drives the risk

Seasonal events make cash uneven.

Owner-run models save cash, but add workload.

Scaled models need staff and contractors.

Weather and permits can break timing.

How many participants does an adventure race need to be profitable?

For Adventure Race Planning, breakeven lands around Month 14. In Year 1, the model shows $297,000 in revenue across 1,500 registrations, or about $198 per registration; after 16% direct and variable costs, contribution is about $166 per registration, and fixed overhead plus payroll is about $219,800. That puts estimated entry breakeven at 1,322 registrations before capex, reserves, and other model items, and sponsorships plus add-ons lower the pure entry count needed.

Breakeven math

Month 14 breakeven

$297,000 Year 1 revenue

1,500 registrations total

$198 revenue per registration

Cost and volume

16% direct and variable costs

$166 contribution per registration

$219,800 fixed overhead plus payroll

1,322 entry breakeven before extras

Key Takeaways

Registration volume and pricing drive the biggest revenue swing.

Sponsorship adds upside, but it is never guaranteed cash.

Direct logistics and staffing can consume most revenue.

Build reserves before owner pay, especially with seasonality.

Compare lean, base, and high owner-income cases

Owner income scenarios

Race count stays editable because the model gives registrations, not event count. Owner pay shifts with registrations, sponsor packages, merch, and VIP passes, while direct costs, payroll, overhead, and reserve needs hold take-home down.

Three owner-pay cases based on the modeled event mix and cost structure.

Scenario

Low CaseDownside case

Base CaseBase case

High CaseUpside case

Launch model

This is the tight case, where owner pay stays close to the modeled salary and profit is thin.

This is the model case, where mid-level volume starts to support salary plus a modest draw.

This is the upside case, where higher volume can support salary plus a stronger draw.

Typical setup

Race count stays editable; Year 1 uses 1,500 registrations at $150, 5 sponsorships, $297,000 revenue, and $3,000 EBITDA, so direct costs, overhead, payroll, and reserves leave little room beyond the $100,000 modeled founder salary.

Race count stays editable; Year 3 uses 4,000 registrations at $160, 12 sponsorships, $856,050 revenue, and $292,000 EBITDA, which can support the modeled founder salary with room for a modest owner draw after direct costs, overhead, payroll, and reserves.

Race count stays editable; Year 5 uses 8,000 registrations at $170, 18 sponsorships, $1.79 million revenue, and $1.066 million EBITDA, so owner take-home can rise after direct costs, overhead, payroll, and a reserve set aside.

Cost drivers

registrations

sponsorships

direct event costs

payroll

reserve cash

registrations

sponsorships

merch and VIP sales

payroll

fixed overhead

registrations

sponsorships

merch and VIP sales

staff growth

reserve cash

Owner income rangeBefore owner reserves

$100kSalary only

$100k-$350kModest draw

$300k-$750kStrong draw

Best fit

Use this to stress-test cash flow when launch volume is light and reserve needs are tight.

Use this as the core planning case for lender, investor, or owner cash planning.

Use this to test upside when event volume, sponsor count, and merch sales all run strong.

!

Planning note: These ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution forecasts.

Adventure Race Planning Core Six Income Drivers

Registration Volume And Entry-Fee Pricing

Registration Volume

When more racers buy in at a higher fee, this is the fastest way to lift owner income. Here’s the quick math: 1,500 registrations x $150 = $225,000, while 8,000 x $170 = $1,360,000. That’s why registration volume and price set the top line, and then decide how much is left after safety, timing, and course costs.

Price only works if the race feels worth it. Entry fees have to match race quality, safety planning, location, route design, and format. Early-bird pricing can improve sell-through, but it lowers average fee. Refund rules also change cash exposure, and team entries can raise volume only if the course and operations can handle the load.

Track Fee Mix and Fill Rate

Watch registrations sold, average fee per entry, early-bird share, refund rate, and team-entry share. If early-bird sales fill slots too cheaply, owner profit can flatten even when the event looks busy. The goal is not just more starts; it is more paid starts at a fee that covers safety, overhead, and a real profit draw.

Test price steps against capacity. If the field is close to sold out, a $20 fee lift on a full event can add meaningful revenue without extra course cost, but only if service levels stay high. If the event sells slowly, use early-bird windows to pull cash in sooner, then tighten refund terms so weather or cancellation risk does not hit owner pay.

Sponsorship And Partnership Revenue

Sponsorship Revenue

Sponsorship is upside cash, not base-case cash. In the model, packages grow from 5 at $5,000 to 18 at $7,000, so sponsor revenue rises from $25,000 in Year 1 to $126,000 in Year 5. That income can lift owner pay fast because it has little direct cost, but only if the event has enough audience, repeat exposure, and clean sponsor reporting.

Local businesses, outdoor gear partners, tourism groups, and vendor booths can improve margin beyond entry fees. The quick math is simple: more sponsors at a higher price means more gross profit, but weak turnout or one-off events shrink value. If the race does not create visible reach, sponsor cash stays uneven.

Measure Sponsor Value

Track what sponsors actually buy: athlete count, repeat events, logo placement, email reach, and post-race recap data. Sponsor pricing should rise only when those proof points improve. Audience size, repeat events, visibility, and post-race reporting are the real inputs, not hope. That keeps the forecast tied to cash the business can actually collect.

Use separate lines for title sponsors, partner sponsors, and vendor booths so you can see margin by package. If booth fees and partner cash cover more fixed event overhead, more entry-fee revenue can flow to profit and owner draw. Model sponsorship as upside, and stress-test it at zero.

Track sponsor count by tier.

Measure cash collected, not pledges.

Report reach after each event.

Test booth sales by location.

Staffing, Contractors, Volunteers, And Owner Workload

Race Staffing Load

Labor is the margin gate here: contract race-day wages run 20% of revenue in Year 1 and 15% in Year 5, while the full payroll stack totals $340,000 at scale. The founder’s $100,000 pay is part of that stack, so owner income only rises if event revenue grows faster than staffing cost.

Volunteers can cut the cash load, but only for support work. They do not replace paid skill in safety, timing, medical, or logistics, and that’s where bad staffing shows up fast in refunds, delays, and stress. If the owner does everything personally, short-term profit may look better, but the business will hit a ceiling sooner.

Cut Labor Waste

Build the model from registrations, event count, labor hours per race, contractor rates, volunteer coverage, and fixed payroll. Here’s the quick math: if volume rises but labor stays at 20% instead of trending toward 15%, the extra sales won’t fall through to owner pay as fast as expected.

Track labor by race, not just by month. The useful checks are simple: paid staff per participant, founder hours on operations, and whether volunteer help is covering support tasks instead of core control jobs. If the team still depends on the owner for timing, safety, or logistics, growth is capped and execution risk stays high.

Track labor percent by event.

Watch paid staff per participant.

Log founder hours weekly.

Assign volunteers to support tasks.

Keep core safety roles paid.

Direct Event Logistics, Permits, Insurance, And Safety Costs

Direct Event Logistics And Safety Costs

Direct event operations eat 60% of revenue in Year 1 and 50% in Year 5, while participant supplies run 30% to 25%. That means the event starts with thin gross profit, so owner pay depends on clean execution and strong pricing. Business insurance is $300 per month, and the upfront asset base includes $73,000 in race equipment, vehicle, tents, tables, and medical gear.

This driver includes route setup, land access, timing, communications, medical coverage, and equipment transport. Here’s the quick math: if revenue is $100,000, Year 1 direct ops and supplies can consume $90,000 before other overhead. The work protects the event, but every extra course mile, permit, or safety crew lowers cash available for the owner unless registration volume and pricing are high enough.

Track Safety Cost Per Event

Measure cost per participant and cost per race, not just total spend. Split the model into direct ops, participant supplies, and insurance, then test each event by route complexity, land access, timing setup, and medical coverage. If one race needs more transport or staffing, price it higher or shrink the course.

Use a simple control sheet:

Track cost as percent of revenue

Log permit and access fees

Budget equipment transport separately

Review safety spend before owner draw

Event Frequency And Format Mix

Event Frequency And Format Mix

Fewer large races can lift ticket price, but more repeatable events spread fixed overhead across more starts, sponsors, and repeat participants. Since race count isn’t given, model both paths: a single high-touch course can raise revenue per event, while a series format can smooth cash flow and reduce dependence on one weekend.

Here’s the tradeoff: bigger formats can support higher pricing, but they also push safety, transport, timing, and owner workload higher. The key inputs are event count, average starts per event, sponsor count, repeat-entry rate, and fixed overhead. If the extra gross profit doesn’t beat the added operating load, owner pay gets squeezed.

Test Series Versus One-Off Races

Track revenue per event, gross margin, and owner hours by format. A repeatable trail, biking, navigation, or multi-sport series is easier to forecast than a single flagship race, and it can improve cash collection from registrations and sponsors. But if each added event creates more permits, staffing, and timing cost, margin can stall fast.

Compare starts per event and fee per start.

Test repeat participant rate by format.

Price for safety, transport, timing.

Cap owner workload before adding dates.

Reserves, Refunds, Cancellation Risk, And Seasonality

Reserves, Refunds, and Seasonal Cash

For an adventure race operator, EBITDA is not distributable cash. Weather, permitting delays, low registrations, refund claims, and sponsor checks that land late can squeeze cash even when profit looks fine. In this model, breakeven lands in Month 14, payback takes 30 months, and minimum cash bottoms at $852,000 in Month 24, so owner pay should wait until reserve targets are funded.

Track registration pace, refund exposure, sponsor payment timing, and the monthly cash floor before taking a draw. If cash falls below the reserve plan, owner income should pause because the event still needs money for permits, timing, safety, and reschedules. Reserve logic belongs below profit and above distributions.

Build the reserve before you pay yourself

Measure booked registrations, refunded entries, sponsor invoices outstanding, and committed event cash by month. The key test is simple: can cash stay above the $852,000 low point even if a race shifts or rain cuts turnout? If not, keep earnings in reserve and delay owner distributions.

Forecast cash by event month.

Separate profit from available cash.

Hold refund and weather reserves.

Pay owner after reserve funding.

Use a tighter draw policy when sponsor cash arrives after event costs or when early registrations lag. That protects the season from a bad-weather weekend, a permit slip, or a late-selling race, and it keeps owner income tied to real surplus, not paper profit.