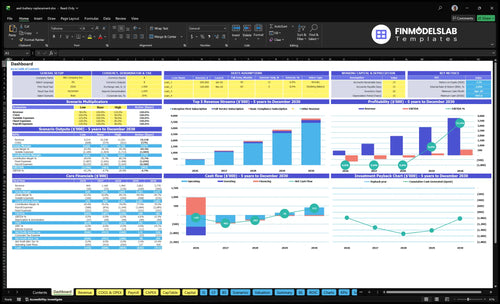

You’re estimating owner take-home for an AED (automated external defibrillator) battery replacement service, not a generic field service salary The researched model shows a planned $180,000 CEO salary, revenue growing from $469,000 in Year 1 to $3778 million in Year 5, and breakeven in Month 41 Figures are planning assumptions before taxes, debt service, personal benefits, and guaranteed distributions

Owner income$180kNet margin-137% to 15%Revenue for target pay$1.2MBusiness difficultyHard

Want to test your own AED service owner income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want the six drivers that move AED service owner income?

1

AED Base

$469K-$3.78M

More devices and sites drive the biggest revenue swing, with model revenue rising from $469K in Year 1 to $3.778M in Year 5 and breakeven in Month 41.

2

Contract Attach

55%-95%

Moving more customers into full-service and enterprise plans lifts recurring cash and cuts churn, so each account pays back faster.

3

Ticket Mix

$45-$3.5K

Shifting volume from basic compliance to higher-tier plans lifts monthly revenue per customer far more than price tweaks alone.

4

Unit Margin

93.5%-94.7%

Battery and pad cost stays under 7% of revenue, so small supply savings flow straight into owner take-home.

5

Route Density

7.3%-8.5%

Fewer miles per stop cut field delivery cost and protect margin as the team adds more sites.

6

Labor Use

$509K-$1.61M

Keeping technicians productive matters as payroll rises from $509K to $1.607M, especially with fixed overhead at $27,600 a month.

Want the AED Battery Replacement Service income forecast model?

How much can an AED battery replacement service owner make?

An AED Battery Replacement Service owner can make $180,000 per year as Chief Executive Officer in this source model, but owner profit above salary starts only after breakeven in Month 41; see How To Start AED Battery Replacement Service Business? for the startup path. EBITDA runs negative in Years 1–3, then turns positive at $190,000 in Year 4 and $581,000 in Year 5.

Owner Pay

CEO salary: $180,000/year

Year 1 EBITDA: -$641,000

Year 3 EBITDA: -$226,000

Breakeven: Month 41

Upside Drivers

Revenue grows: $469,000 to $3.778 million

Year 5 EBITDA: $581,000

Extra take-home depends on cash reserves

Technician routes scale beyond owner labor

Can an AED battery replacement service scale beyond the owner?

Yes—AED Battery Replacement Service can scale beyond the owner, but only if route density and technician utilization stay high enough to cover the heavier field stack. Here’s the quick math: certified field technicians rise from 30 FTEs in Year 1 to 160 FTEs in Year 5 at $52,000 each, while revenue grows from $469,000 to $3.778 million; EBITDA turns positive in Year 4 at $190,000 and reaches $581,000 in Year 5. The catch is simple: adding technicians raises capacity, but it also adds payroll, training, insurance, vehicle cost, scheduling work, and quality control.

Where scale works

30 to 160 FTEs adds capacity

$469,000 to $3.778 million revenue

EBITDA turns positive in Year 4

$581,000 EBITDA in Year 5

What limits it

Payroll rises with each tech

Training and certification add cost

Vehicles and insurance add overhead

Scheduling and quality control get harder

What margins and costs matter most in an AED battery replacement service?

For an AED Battery Replacement Service, the biggest pressure is not demand; it’s the mix of direct cost and fixed overhead. In the first year, battery and electrode pad costs run 65% of revenue and field technician delivery costs run 85%; by Year 5, those fall to 53% and 73%, and you can compare the plan structure in How To Write A Business Plan For AED Battery Replacement Service?.

Direct cost drivers

Battery and pad cost starts at 65% of revenue.

Field service cost starts at 85%.

Combined direct cost improves from 150% to 126%.

The table shows direct margin at 850% to 874%.

Fixed burden risks

Fixed overhead is $27,600 per month.

Payroll grows from $509,000 to $1.607 million.

Marketing grows from $120,000 to $300,000.

Watch expired inventory, returns, and weak route density.

Key Takeaways

More active AEDs drive revenue, but density must stay tight.

Contract attach rates smooth cash and improve retention.

Battery-only visits can miss travel and support costs.

Labor growth helps capacity, but utilization protects margin.

AED battery replacement income scenarios for low, base, and high cases

Owner income scenarios

Owner income swings here because payroll, capex, and marketing absorb cash early. EBITDA turns positive by Year 4, but distributions still depend on reserves and the Month 40 cash trough.

Low, base, and high cases show how salary and distributions can differ as the service scales.

Scenario

Low CaseCash burn

Base CaseNear breakeven

High CaseUpside case

Launch model

This case models a slow launch where Year 1 revenue is $469,000 and EBITDA is -$641,000, so owner income stays salary-led.

This case models the core operating plan where Year 4 revenue reaches $2.863 million and EBITDA turns positive at $190,000.

This case models the stronger path where Year 5 revenue reaches $3.778 million and EBITDA rises to $581,000.

Typical setup

Year 1 uses 85.0% direct margin, $120,000 marketing, about $509,000 payroll, and $27,600 monthly fixed overhead, with little room for distributions.

Year 4 runs at 86.8% direct margin, $280,000 marketing, about $1.334 million payroll, and enough profit to support salary with limited distributions.

Year 5 uses 87.4% direct margin, $300,000 marketing, about $1.607 million payroll, and stronger profit that can support salary plus larger draws if reserves hold.

Cost drivers

Negative EBITDA

heavy payroll

early marketing spend

fixed overhead

reserve drain

Positive EBITDA

higher revenue mix

lower CAC

larger field team

cash recovery after Month 41

Higher volume

stronger mix

better CAC

scaled field team

reserve needs still matter

Owner income rangeBefore owner reserves

$180k salary onlyNo draws

$180k plus limited drawsModest draws

$180k plus stronger drawsHigher draws

Best fit

Use this to stress-test a launch that protects cash and keeps the owner on salary only.

Use this for the most balanced view of owner pay when the business is moving toward stable operations.

Use this to test upside when the service scales well and cash stays above the low point.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or actual distributions.

AED Battery Replacement Service Core Six Income Drivers

Active AEDs under service

Active AEDs Under Service

More active AEDs under service means more inspections, battery replacement events, and renewal touches, so revenue grows as the serviced base grows. This driver ties volume to revenue, with disclosed growth from $469,000 in Year 1 to $3,778 million in Year 5, but only if route capacity and retention stay tight.

The main inputs are serviced AED count, locations per route, renewal rate, and revenue per account. One clean rule: more accounts help only when they are dense enough to keep travel time below the extra revenue they bring. Low-density sites can raise labor and fuel faster than gross profit.

Track Density Before You Add Accounts

Watch accounts per zip code, visits per technician day, and same-day cluster rate. Here’s the quick check: if a new account adds miles but not enough recurring revenue, it can cut owner pay even when top-line sales rise.

Test new accounts against route density and renewal rate before signing. If the route gets spread out, schedule quality drops, missed touchpoints rise, and the owner ends up buying growth with unpaid drive time instead of profit.

Battery and pad gross margin

Battery and Pad Gross Margin

If battery and electrode pad costs run at 65% of revenue in Year 1, product gross margin is only 35%. By Year 5, costs at 53% leave 47% gross margin, so every point of procurement, shipping, or return control changes cash fast at the disclosed $3,778 million revenue level.

This driver includes procurement cost, shipping, brand compatibility policy, returns, warranty exposure, and expired inventory risk. Here’s the quick math: a 1-point margin swing equals about $37.8 million at Year 5 revenue, but gross profit is still not owner pay because payroll, vehicles, insurance, marketing, and reserves come out below gross profit.

Control Landed Cost and Waste

Track landed cost per battery kit, return rate, warranty claims, and expired stock by SKU and device type. Use a clear compatibility rule so you do not buy parts that sit too long or fail on site. If a battery-only job does not cover travel and admin, it helps revenue but still hurts take-home income.

Set a minimum product gross margin by tier, then test it against shipping, spoilage, and replacement frequency. A clean target is better than a big average. Watch the share of revenue spent on parts every month; moving from 65% to 53% already lifts gross margin by 12 points, which gives more room for payroll and owner draw.

Track landed cost by SKU.

Review expiries before reordering.

Log returns and warranty losses.

Price compatibility risk into the tier.

Replacement ticket and product mix

Replacement Ticket Mix

This driver covers what gets billed on each service visit: batteries, electrode pads, inspection labor, and documentation. Owner income goes up when the average ticket covers travel, admin, and support time, not just parts. The key inputs are pad attach rate, replacement frequency, inspection fee, and subscription tier.

Here’s the quick math: a battery-only job can look busy but still lose money if it does not cover the full visit cost. Ethical, need-based replacement only matters because overstating wear hurts trust and can raise churn. Source revenue grows from $2.863 million in Year 4 to $3.778 million in Year 5 as mix and volume mature.

Track Visit Yield

Measure each visit by ticket size, attach rate, and gross margin. If pad attach rate is weak or inspection fees are too low, the owner pays for driving, scheduling, and follow-up out of profit, not revenue.

Use a simple rule: every visit should recover parts, labor, and the time to document compliance. Watch for battery-only work that misses travel and admin cost. Tight pricing by subscription tier keeps cash flow steadier and protects owner draw.

Labor utilization and owner role

Labor role and owner pay

Owner take-home changes with the job the owner does. If the owner is the CEO, the model uses $180,000; if the owner runs field ops, the benchmark is $95,000; certified technicians are set at $52,000 each. The driver is not headcount alone, but whether those labor hours turn into paid inspections, replacements, and renewals.

As technician FTEs rise from 30 to 160, payroll grows from $509,000 to $1.607 million. That can lift capacity, but if utilization, pricing, or quality control slip, margin falls and owner take-home gets trapped behind wages, travel, and rework.

Track labor by role and route

Track paid visits per tech, accounts per route, utilization or billable hours divided by paid hours, and labor cost per serviced AED. Those inputs show whether each labor hour is covering travel, inspection, and admin time. One clean rule: if a route cannot pay for its hours, it should not be added.

Owner role: service, manage, sell, operate.

Tech FTEs and paid hours.

Accounts per route and renewal rate.

Labor cost per serviced AED.

Separate the owner’s role in the model: hands-on service, team management, contract sales, or operations. Pay the owner as salary or draw only after labor is covered. The fastest income leak is adding FTEs before each tech’s workload, pricing, and quality checks are tight.

Route density and travel cost

Route Density

Route density is how many AED service stops fit into one technician day and one zip code. It includes visits per technician day, miles per visit, accounts per zip code, and the same-day cluster rate. When density is weak, unpaid drive time and downtime eat the ticket, and a good service price can still lose money. With $5,500 a month in fleet insurance and maintenance, sparse routes cut owner cash fast.

In Year 1, field technician service delivery cost runs at 85% of revenue, improving to 73% by Year 5. That gap is the profit pool for owner pay, reserves, and growth, so route waste matters more than it looks on paper. More clustered stops mean more billable visits per day and less fuel, mileage, and dead time between jobs.

Pack Stops by Zip

Measure the route before you add accounts. If a new account adds long drives, it can lower take-home income even when the ticket looks solid. Build forecasts around the four route inputs, then test schedule blocks by zip, same-day clusters, and technician capacity. What this hides: one low-density account can drag down a whole day’s margin.

Track visits per technician day.

Track miles per visit.

Count accounts per zip code.

Measure same-day cluster rate.

Drop weak-density accounts first.

Maintenance contract attach rate

Maintenance Contract Attach Rate

Maintenance contract attach rate is the share of active AED accounts that buy a recurring service plan. It turns uneven battery and inspection work into monthly recurring revenue, which smooths cash between replacement cycles and makes gross profit easier to forecast. That steadier cash flow helps the owner pay themselves without waiting for one-off service spikes.

The mix matters: $45 to $57 basic compliance plans, $95 to $125 full-service plans, and $2,500 to $3,500 enterprise fleet contracts all change cash flow and margin. The risk is underpricing service commitments, because extra labor, reporting, and route time can eat the fee fast.

Price and Track the Recurring Mix

Use the attach rate to track how many AEDs convert to paid service plans, then split it by customer type. The key inputs are active AEDs, renewal rate, contract tier, and locations per route. One clean rule: if a plan does not cover labor, travel, and admin time, it is too cheap.

Monthly recurring revenue by tier

Renewal rate by account type

Service time per location

Watch whether higher-priced plans improve scheduling and reduce idle drive time. If attach rate rises but route density stays low, the owner can still lose money on travel and support. Price for the work you are promising, not just the battery swap.