How Much Non-Alcoholic Drink Production Owners Make at $622K+ Sales

A non-alcoholic beverage business owner can plan around pre-tax owner-income capacity of about $437,775 in Year 1 to $3,095,860 in Year 5 in this model, before taxes, debt service, reserves, and reinvestment These are researched assumptions, not guaranteed pay The model starts at 180,000 units and $622,500 in revenue, then grows to 1,000,000 units and $3,728,000 in revenue The key caveat is cash: inventory builds, production deposits, and growth spending can hold back distributions even when profit looks strong

Owner income$437.8k to $3.10MNet margin32% to 68%Revenue for target pay$215kBusiness difficultyHard

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on sales, margins, payroll, taxes, debt, and reserves.

Want to check owner income in the Non-Alcoholic Drink Production model?

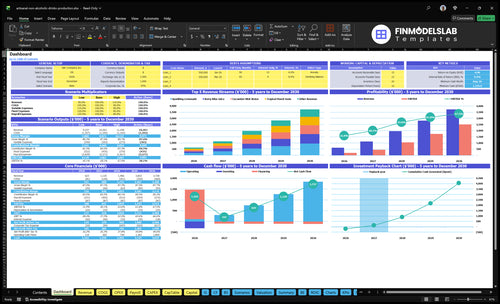

This decision-support dashboard in the Non-Alcoholic Drink Production Financial Model Template shows income outputs, assumptions, and scenario tabs for volume, pricing, COGS, overhead, owner pay, and cash reserves; open the model.

Owner-income model highlights

Revenue spans $622.5k-$3.728m

Volume spans 180k-1.0m units

Gross margin near 87%

Fixed overhead is $78,600

Pre-tax cash reaches $3.096m

How do packaging and ingredient costs affect non-alcoholic beverage owner income?

If you’re pricing What Is The Estimated Cost To Open Your Non-Alcoholic Drink Production Business?, packaging and ingredients hit owner income fast. In this model, unit COGS runs from $0.30 to $0.40 per unit, Year 1 unit COGS total $62,550, and revenue-based production costs add another 30%, or $18,675. A $0.05 cost increase cuts cash by $9,000 across 180,000 Year 1 units and $50,000 across 1,000,000 Year 5 units.

Cost drivers

$0.30 to $0.40 per unit COGS

$62,550 Year 1 unit COGS

30% added production costs

$18,675 extra cost load

Income impact

$0.05 more per unit cuts cash

$9,000 loss at 180,000 units

$50,000 loss at 1,000,000 units

Minimum runs, shrink, freight matter

Can a non-alcoholic drink production owner pay themselves in the first year?

Yes — Non-Alcoholic Drink Production can pay the owner in Year 1 if cash timing stays healthy, but the draw should come after reserves. The model shows $622,500 revenue from 180,000 units, $78,600 in fixed overhead, and $437,775 in pre-tax cash before owner pay, taxes, debt, reserves, and reinvestment.

Why pay can work

$622,500 revenue supports draw potential

180,000 units spread fixed costs

$437,775 cash before owner pay

Pay after reserve targets are met

What can block the draw

Production deposits can tie up cash

Inventory builds need upfront money

Receivables can delay collections

Launch marketing can drain cash fast

How much revenue does a non-alcoholic beverage company need to pay the owner?

Non-Alcoholic Drink Production needs about $215,000 in Year 1 revenue to support $100,000 owner pay, before taxes, debt, cash reserves, and reinvestment; for market context, see What Is The Current Growth Rate Of Non-Alcoholic Drink Production?. Here’s the quick math: ($78,600 fixed overhead + $100,000 owner pay) ÷ 82.95% contribution margin = $215,310.

Base Case

Target owner pay: $100,000

Fixed overhead: $78,600

Contribution margin: 82.95%

Revenue needed: $215,310

Pressure Points

Production costs near 30% hurt cash

Sales fees near 25% cut margin

Marketing near 15% raises break-even

Freight and reserves push revenue higher

Want the six drivers behind owner income?

1

Volume

180K-1.0M

More bottles sold spreads fixed labor and plant costs, so take-home rises fastest as output moves from 180K units to 1.0M.

2

Unit Price

$3.00-$4.30

A small price lift adds straight to profit because the unit cost stays close to that range.

3

COGS

$0.30-$0.40

Keeping pack, ingredients, and freight near the low end protects gross margin on every case.

4

Cash Reserve

$1.15M

The model hits a minimum cash need of about $1.146M in month 8, so reserve timing and reinvestment drive owner pay.

5

Channel Mix

2.5%-4.0%

Sales and distribution fees plus marketing take 2.5% to 4.0% of revenue, so lower-cost channels keep more cash.

6

Fixed Overhead

$78.6K

Annual fixed overhead matters less at high volume, but it still sets the floor on cash burn.

Non-Alcoholic Drink Production Core Six Income Drivers

Production Volume and Utilization

Production Volume and Utilization

Production volume and utilization are the main spread lever. When annual units rise from 180,000 in Year 1 to 1,000,000 in Year 5, the same $78,600 fixed overhead gets spread across far more bottles, so more revenue can reach owner profit. In this model, fixed overhead falls from 126% of Year 1 revenue to 21% of Year 5 revenue.

But volume only helps if margins hold. Bigger runs need more inventory cash, and discounts or freight can turn scale into losses. The owner’s take-home income rises when each added bottle still leaves positive contribution after direct production and selling costs.

Track volume against cash, not just output

Measure planned units, actual units, yield, freight per unit, discount rate, and inventory days. Here’s the quick check: if higher volume does not lower fixed overhead per unit and improve cash after the next run, slow production before paying out more owner draw.

Units by product and month

Capacity used versus plan

Inventory cash tied up

Freight and discount drag

A simple forecast compares 180,000 units with 1,000,000 units and asks whether gross margin still covers the same $78,600 overhead. If it does, owner pay has room to grow. If not, scale just increases strain on cash.

1

Average Selling Price

Average Selling Price

Average selling price is the net price per unit after discounts, promotions, and distributor deductions. In this model, unit prices range from $300 to $430, with a $346 blended average in Year 1 and $373 in Year 5. That price lands in revenue first, so any cut flows straight to gross profit and owner draw.

Here’s the quick math: at 1,000,000 units, every $0.10 change in realized price moves revenue by $100,000 before costs. The inputs are shelf price, product mix, discounts, promo spend, and distributor deductions. What this estimate hides is timing: strong gross revenue still can’t pay the owner if cash gets eaten by trade terms or markdowns.

Protect Net Price

Track realized price, not list price. Use a simple price waterfall: shelf price minus discounts, promotions, and distributor deductions. Review it by product and channel each month, then compare the blended average to the $346 Year 1 base and $373 Year 5 target. If realized price slips, higher volume alone will not protect owner income.

Test small moves first. Keep pack size, channel mix, and promo depth separate so you know which lever changed profit. The owner should watch:

Realized price per unit

Discount and deduction rate

Unit mix by channel

Revenue per production run

2

COGS and Gross Margin

COGS and Gross Margin

COGS is the direct cost to make and ship each drink unit. In this model, unit COGS runs $0.30 to $0.40, plus 30% of revenue for co-packer fee, packaging design, quality control, ingredient sourcing, and recipe development. With Year 1 gross margin near 87%, owner income depends on keeping those unit costs tight before overhead is even paid.

Here’s the quick math: inputs like packaging, ingredients, yields, shrink, and co-packing labor move gross profit on every bottle. If yield slips or packaging gets pricier, margin drops right away and less cash is left for payroll, debt, and owner draw. One point of gross margin loss can wipe out a lot of take-home income at scale.

Tighten unit cost control

Track COGS per unit, not just total spend. Break it into ingredient cost, packaging, co-packer labor, freight, and shrink, then compare each run to the $0.30 to $0.40 range. If one line drifts, fix that before the next batch so margin does not leak across every case shipped.

Use a simple check: gross profit = net revenue minus COGS. Review yields, spoilage, and minimum run sizes before you order. If a co-packer change or packaging upgrade lifts cost without a price increase, the owner’s pay falls fast because the hit lands on every unit sold.

Track cost per bottle every run.

Measure yield and shrink weekly.

Compare actuals to quoted COGS.

3

Channel Mix and Distribution Costs

Channel Mix and Distribution Costs

Channel mix changes how much of each dollar reaches the owner. In this model, sales and distribution fees fall from 25% of revenue in Year 1 to 15% in Year 5, and marketing and promotion drop from 15% to 10%. That cuts channel cost from 40% to 25% before production and overhead.

Distributor-heavy growth can raise volume, but it can also lower net price and slow collections. Direct or local accounts may lift margin, yet they add fulfillment, service, and marketing work. The owner’s draw depends on net cash per unit, not just shipped units, so a strong sales month can still feel tight if cash comes in late.

Measure Net Cash per Unit

Track channel share, fees as % of revenue, promo spend, and days to collect cash. Here’s the quick math: if channel cost is 40% in Year 1, the business keeps $60 per $100 of revenue before production and overhead; at 25%, it keeps $75. That gap is what funds owner pay.

Test mix by account type, not just by total sales. Push the channel that gives the best net cash per unit after freight, commissions, promo, and service time. If a local account pays better but needs more hands-on fulfillment, price that work in or the owner ends up financing growth out of personal cash.

4

Fixed Operating Overhead

Monthly Fixed Overhead

Fixed overhead is the cash floor the business pays even when bottle volume slows. With $3,500 rent, $800 utilities, $600 insurance, $400 software, $1,000 legal and accounting, and $250 website costs, total overhead is $6,550/month or $78,600/year. That comes out before owner pay, taxes, and reserves.

Here’s the quick math: at $622,500 Year 1 revenue, overhead is 12.6% of sales; at $3,728,000 in Year 5, it drops to 2.1%. With volume rising from 180,000 to 1,000,000 units, fixed overhead falls from about $0.44 per unit to $0.08. Scale helps only if sales cover that base cleanly.

Hold the Cash Floor Down

Track each fixed line monthly and keep it flat unless sales can absorb it. The inputs are simple: rent, utilities, insurance, software, legal and accounting, and website spend. If any line rises, owner draw gets squeezed fast because the same $78,600 still has to be covered.

Watch overhead per bottle.

Review fixed costs monthly.

Protect reserves before owner pay.

A clean rule: if fixed overhead grows faster than units sold, margin turns into admin drag. Set a target for overhead per bottle, then compare it with actual production and revenue every month. The goal is simple: let volume dilute the $6,550/month base, not force deeper cash calls from the owner.

5

Working Capital and Reserves

Working Cash and Reserve Draws

Cash flow can lag profit in drink production. Owners pay for raw materials, bottles, labels, co-packer labor, shipping, deposits, receivables, and the next run before they can pay themselves, so pre-tax profit is not the same as spendable cash.

The model shows strong pre-tax cash before reserves, but it does not set a reserve rate. A good calculator should let users set inventory reserve, debt service, and reinvestment buckets, because if receivables stretch or minimum runs rise, owner draw should shrink first.

Set the Cash Guardrails

Track the cash gap between production spend and collection. In this model, the key question is not just margin; it is how much cash stays after the next run is funded and receivables clear.

Use a simple reserve test and keep it visible every month:

Measure cash tied in inventory.

Track days sales outstanding.

Hold debt service cash first.

Delay owner draw when cash tightens.

That keeps distributions tied to real cash, not paper profit.

6

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Owner income rises as unit volume and pricing scale, but fixed overhead, staffing, and shipping still take a bite. Early years need tighter reserves; Year 5 has the widest cushion.

Low, base, and high cases show how volume and cost control change owner income.

Scenario

Low CaseLow Case

Base CaseBase Case

High CaseHigh Case

Launch model

This is the lower earnings path and assumes a cautious launch.

This is the modeled core-case earnings path.

This is the stronger earnings path if scale keeps building.

Typical setup

Year 1 runs at 180,000 units and $622,500 revenue, with the leanest staffing mix and a smaller cash cushion before reserves.

Year 3 reaches 550,000 units and $1,966,000 revenue, with a fuller team and a more stable margin structure before reserves.

Year 5 reaches 1,000,000 units and $3,728,000 revenue, with full staffing and the strongest cash build before reserves.

Cost drivers

Co-packer fees

packaging costs

quality control

ingredient sourcing

shipping

Higher production volume

full-time operations and sales staff

packaging and shipping

quality control

marketing spend

Peak production volume

full staffing

shipping load

quality control

marketing and distribution

Owner income rangeBefore owner reserves

$437,775Low Case

$1,573,958Base Case

$3,095,860High Case

Best fit

Best for founders stress-testing launch demand, reserve needs, and a slower sales ramp.

Best for the core plan once repeat orders and throughput are steady.

Best for testing upside if production stays tight and costs hold at scale.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.