How Much Does an Awning Cleaning Service Owner Make? $85k+ Model

You’re trying to turn route work into owner income, not compare yourself with an employee cleaner This model separates $139k to $196M in service revenue, gross profit, EBITDA, reserves, and the modeled $85,000 founder salary before personal taxes

Owner income$85kNet margin39%Revenue for target pay$732kBusiness difficultyHard

Want the six income drivers?

1

Pricing Mix

$50-$325

A bigger share of premium cleans and add-ons lifts average ticket fast, so more revenue reaches owner take-home.

2

Repeat Base

$180-$100

More quarterly and bi-annual commercial accounts cut CAC from $180 to $100 and make cash flow steadier.

3

Route Density

31 mo

More jobs on each route spread setup and fuel over more sales, which pushes more profit into take-home.

4

Labor Load

$85K

The founder's $85K pay and technician mix decide how much gross profit survives payroll.

5

Cost Stack

21%-15.5%

Keeping variable costs near 21% and moving them toward 15.5% protects EBITDA on every clean.

6

Capacity Plan

56 mo

If crews sit idle in slow months, breakeven slips past Month 31 and payback stretches toward 56 months.

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay for an awning cleaning service.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want the full income model for Awning Cleaning Service?

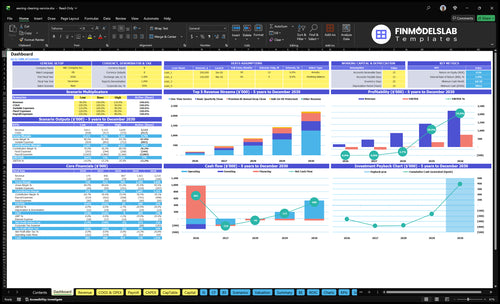

Dashboard shows revenue build, service mix, pricing assumptions, recurring contracts, add-ons, labor, fixed and variable costs, capex, cash flow, EBITDA, and owner pay. Scenario tabs show revenue from $139k to $196M, EBITDA from -$145k to $754k, and Month 31 break-even. Open the Awning Cleaning Service Financial Model Template.

Owner-income model highlights

Revenue, costs, cash flow

Recurring plans and add-ons

Break-even and owner pay

What is the profit margin for an awning cleaning service?

For an Awning Cleaning Service, the margin picture starts strong; see What Is The Estimated Cost To Open And Launch Your Awning Cleaning Service Business? for the cost base behind it. On the model, contribution margin before payroll, fixed overhead, and marketing is 790% in Year 1, then 803%, 817%, 832%, and 845% by Year 5. The catch is that operating margin is lower once payroll, rent, insurance, marketing, and founder salary are included.

Direct cost pressure

Cleaning agents fall from 80% to 60%.

Tool consumables fall from 20% to 15%.

Referral fees fall from 70% to 50%.

Fuel and maintenance fall from 40% to 30%.

Margin reality

Contribution margin climbs from 790% to 845%.

Operating margin is lower after overhead.

Payroll and rent reduce cash left over.

Insurance and marketing also compress profit.

Is awning cleaning a seasonal business?

Yes—Awning Cleaning Service is seasonal because demand moves with weather windows, outdoor dining traffic, storefront visibility, and property manager schedules, so monthly revenue won’t stay flat. The model can smooth that with recurring maintenance contracts, but it still shifts from 300% premium deep cleans in Year 1 to 450% in Year 5, while one-time service drops from 400% to 200%. Here’s the quick math: cash reserves matter because minimum cash need is modeled at $390k, and payback takes 56 months.

Why demand changes

Weather opens and closes job windows

Restaurants need clean awnings for curb appeal

Storefront visibility drives timing

Property managers schedule around vacancies

What helps smooth revenue

Recurring contracts reduce monthly swings

Premium deep cleans rise over time

One-time jobs shrink in the mix

$390k cash helps cover slow periods

How much can a solo awning cleaning business owner make?

Price complex jobs correctly or field hours turn unprofitable.

Recurring contracts lower customer acquisition costs and stabilize scheduling.

Route density cuts fuel, maintenance, and unpaid drive time.

Plan for Year 1 losses and Month 31 break-even.

Compare lean, base, and high owner income cases

Owner income scenarios

Owner income depends on route density, pricing, and how fast labor and truck costs are covered. Early years stay cash-tight; later years open room for draws.

Low, base, and high owner income paths for the cleaning business.

Scenario

Low CaseCash-constrained

Base CaseBreak-even

High CaseScaled route network

Launch model

The owner stays salary-funded while the business absorbs a Year 1 loss and builds demand.

The business reaches Month 31 break-even, so the owner can pay salary and start taking limited distributions.

A scaled route network pushes EBITDA higher and creates room for meaningful owner draws after reinvestment.

Typical setup

About $139k revenue and -$145k EBITDA keep the business in ramp mode with startup cash covering the $85k founder salary.

About $732k revenue and $23k EBITDA point to a steadier run rate with a salaried founder and limited draw room.

Year 5 scale with $754k EBITDA, more technicians, and wider route coverage creates the strongest owner income.

Cost drivers

High CAC

one-van capacity

fixed rent and insurance

payroll load

fuel and supply costs

Better route density

recurring clean mix

lower CAC

modest add-on sales

controlled overhead

Higher route density

more technicians

stronger add-on attach

lower CAC

fixed costs spread wider

Owner income rangeBefore owner reserves

$85k salarySalary funded

$85k salary + small drawSmall draw

$85k salary + larger drawProfit share

Best fit

Use this to stress-test the first operating year and cash burn.

Use this as the most likely operating case once the route base is established.

Use this to test upside if recurring accounts and add-ons keep scaling.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Awning Cleaning Service Core Six Income Drivers

Pricing And Average Ticket

Pricing and Average Ticket

Average ticket is the price per job, and it drives how fast owner pay grows. For this service, quote for awning size, material, stains, height, access, travel, and service type. Year 1 model prices are $75 for basic clean, $125 for premium deep clean, $300 for one-time service, and $50 for UV protectant.

Higher ticket size helps route economics only if labor time does not rise as fast. If a complex job gets priced like a simple one, billable work turns into low-margin field hours, and that cuts gross margin, cash flow, and the money left for owner draw. The key math is simple: revenue per job minus labor and travel cost.

Quote Every Job by Complexity

Track quoted price vs. actual labor minutes on every job. If a premium deep clean takes much longer than a basic clean, raise the quote before it starts eating profit. Also track travel time, because long drives lower effective hourly revenue even when the sticker price looks fine.

Use a short pricing sheet with these inputs: size, stain level, height, access, travel, and service type. One clean rule: if the job adds risk, add price. That protects margin and keeps the average ticket high enough to support wages, fuel, and owner pay.

Average ticket = total revenue ÷ jobs.

Watch labor minutes per job.

Charge more for hard access.

Price travel as part of the quote.

Seasonality And Market Demand

Seasonal Demand

Markets with steady storefronts, restaurants, and property managers make monthly revenue more predictable than one-off residential calls. That matters here because EBITDA is negative in Year 1 and Year 2, so weak weather or a slow retail month can delay owner pay. Break-even is not modeled until Month 31, so cash reserves have to cover the gap.

Revenue quality improves as recurring contracts and premium deep cleans rise, since those jobs smooth the schedule and reduce selling pressure. The risk is seasonality: rainy periods, slow retail months, and outdoor dining swings can cut volume fast. What this estimate hides is how much margin is lost when crews sit idle between routes.

Track Demand by Month

Track booked recurring accounts, monthly cancellations, and weather-hit weeks by route. Separate one-time jobs from contracts, then compare revenue per labor hour and cash burn by month. If a month’s fixed costs and payroll outrun cash, slow hiring and keep reserves before taking draws.

Count recurring sites by property type.

Watch rain-related reschedules weekly.

Stress-test low-season revenue monthly.

Hold cash through Month 31.

Direct Cost And Overhead Control

Cost Control

If direct and variable costs run at 210% of revenue in Year 1, the business is cash negative before payroll and owner pay. Even by Year 5, costs at 155% of revenue still leave no room for distributions unless job cost, travel, and rework drop fast.

Fixed overhead starts near $3,750 per month before benefits, so small misses hit income hard. The $130k in vans, cleaning systems, website and brand work, plus tools and inventory reserve, also ties up cash before the owner can take money out.

Track Cost Per Job

Measure cost per visit, monthly overhead, and the reserve for replacement gear. Here’s the quick math: if one service call costs too much against the invoice, owner pay shrinks even when revenue grows. Break results out by job type so a deep clean does not get priced like a basic clean.

Set a hard rule for distributions: don’t pay yourself until the month covers overhead and leaves cash for replacement spend. One clean test helps: if the job does not cover its share of direct cost plus overhead, it is taking income from the owner, not creating it.

Recurring Commercial Contracts

Recurring Awning Contracts

Recurring contracts make cash flow steadier because the owner is not chasing every job. In this model, the mix shifts away from one-time work, from 400% in Year 1 to 200% in Year 5, while premium deep-clean share rises from 300% to 450%. That can lift average revenue per account and reduce customer acquisition pressure, if the route is built well.

Here’s the catch: contract revenue is not profit by default. If each visit adds travel, setup, and labor hours faster than the fee grows, take-home pay stays tight. CAC falls from $180 to $100, so marketing gets easier, but margin still depends on service frequency, route density, and crew time.

Track Hours, Not Just Renewals

Measure jobs per route, labor hours per clean, travel time, CAC, and retention. A recurring contract only improves owner income if the monthly fee covers the full service cycle and the team can finish more billable work without extra drive time.

Price by visit frequency.

Cap travel between stops.

Track deep-clean share.

Review labor by account.

If contract work starts to crowd out higher-margin jobs, raise minimums or bundle more service per stop. That protects gross margin and keeps recurring revenue from turning into busy, low-pay field hours.

Job Volume And Route Density

Job Volume And Route Density

This driver is about how many billable awning jobs crews finish on one route. When drive time and setup time shrink, more of each shift turns into paid labor, so owner income rises even if ticket size stays flat. The model’s revenue grows from $139k in Year 1 to $732k in Year 3 and $196M in Year 5, so density has to keep up with scale.

Here’s the quick math: tighter routes support the cost drop in fuel and maintenance from 40% to 30% of revenue. That lifts margin and cash for owner pay, but the gain fades if weather, parking, access limits, or crew gaps push jobs off-route. One missed cluster can turn a full day into paid miles and unpaid waiting.

Track Route Density

Track jobs per route, billable hours per crew day, and drive plus setup minutes per job. Group work by zip code and service date, not just by lead date. If the same crew can stack nearby cleanings, more revenue stays available for overhead and owner draw.

Stack jobs within one zone.

Record unpaid travel separately.

Hold weather backup slots.

Flag access and parking limits early.

Protect the route plan with backup crews and same-day resequencing. If a site blocks access, move nearby jobs into that slot so the day still bills well. That keeps labor productive and stops route drift from eating gross profit.

Labor Productivity And Owner Role

Labor Productivity And Owner Role

This driver is the split between owner-led field work and hired crew hours. The model carries a $85k founder salary, $58k lead technician salary, and $42k cleaning technician salary in Year 1, then grows to 3 lead technicians and 8 cleaning technicians by Year 5. More crew scale revenue, but every added headcount raises payroll, training, quality control, scheduling, and rework risk.

Owner-operated work can protect early cash flow because the founder fills labor gaps instead of paying for them. But that also caps capacity. If labor productivity slips, the business keeps paying wages without enough billable output, and the owner’s take-home drops fast. That matters more when EBITDA is negative in Year 1 and Year 2 and break-even is not modeled until Month 31.

Track Billable Hours, Not Just Headcount

Measure this with billable hours per tech, jobs per route, rework rate, and owner hours in the field. The key inputs are staffing mix, service time, travel time, and how often the crew must return for fixes. More billed hours per paid hour lifts margin; more idle time or rework turns payroll into cash burn.

Set a simple weekly rule: if the founder is still doing core field work, track whether each new hire increases completed jobs more than it increases payroll. Document the standard clean process, train to it, and price for access, stain level, and height so complex jobs pay for the extra labor. That’s what keeps owner pay from getting squeezed.