How Much Does A Babysitting Service Owner Make? $125K/Month Target

You’re planning owner pay before demand is proven, so treat babysitting service profit as a model output, not a guaranteed salary In the first-year researched case, platform revenue is about $598k/month, planned owner CEO pay is $125k/month, and visible profit capacity is about $204k/month before taxes, reserves, and distributions

Owner income$329kNet margin64%Revenue for target pay$598kBusiness difficultyHard

Want to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

What drives babysitting service owner income most?

1

Booked Hours

4,375/mo

Booked care hours are not provided, so Year 1 monthly orders are the best volume proxy and the biggest swing in commission income.

2

Average Rate

$40-$75

Moving mix toward higher-value bookings lifts average order value from $40 to $75, and that flows straight into take-home revenue.

3

Sitter Spread

15%+$2

The platform keeps 15% of order value plus $2 per order, so a wider spread between family price and sitter cost improves margin fast.

4

Utilization

High

Better scheduling fills more care slots per sitter, so revenue rises without the same jump in labor and support cost.

5

Repeat Families

100-400

Repeat orders growing from 100 to 400 lower CAC drag and smooth monthly income, which helps payback and cash flow.

6

Fixed Costs

$69K

About $69K of fixed overhead sets the breakeven floor, so rent and admin costs decide how fast profit turns positive.

Want to check owner income in the Babysitting Service model?

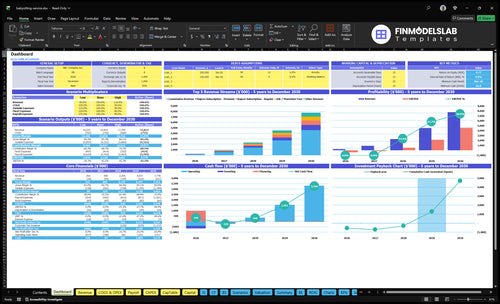

Owner income comes first: the dashboard in the Babysitting Service Financial Model Template shows assumptions, sitter and buyer mix, commission and subscription revenue, costs, payroll, cash flow, and scenarios, with charts for ramp, margin, fixed costs, and pre-tax cash capacity—open it to see $598k revenue, $556k gross profit, $353k operating costs, and $125k owner pay.

Owner-income model highlights

$125k owner pay

Revenue, margin, and costs

Scenarios and cash capacity

What costs affect babysitting service profit?

Labor margin is the biggest profit swing in a Babysitting Service, because each booking only leaves a limited commission and costs like 50% sitter vetting, 20% hosting, 40% performance advertising, and 30% referral incentives stack up fast. For startup cost context, see How Much Does It Cost To Open, Start, Launch Your Babysitting Service Business? Fixed monthly overhead also includes $500 insurance, $300 software, $700 legal and compliance, and $15k base payment processing, so small changes in cancellations, refunds, and admin time hit owner take-home hard.

Main cost drivers

50% sitter vetting

20% hosting cost

40% performance ad spend

30% referral incentives

Fixed monthly pressure

$500 insurance per month

$300 software per month

$700 legal and compliance

$15k payment processing base

Does a babysitting service owner make more by hiring sitters?

If you work every shift yourself, your income is capped by your own hours; if the Babysitting Service hires and coordinates sitters, it can earn commission and subscription revenue beyond the owner’s time. The catch is real: screening, scheduling, coverage, compliance, and quality risk all rise fast. In the research case, 333 first-year sitter acquisitions support about $28k/month in sitter subscription revenue, with a 500% student, 400% experienced, and 100% specialized sitter mix, so scale only works if completed bookings grow faster than support costs.

Owner-led income

Income stops at worked shifts.

No sitter, no booking revenue.

Hours cap monthly growth.

Quality stays easier to control.

Agency model upside

Revenue can outgrow owner hours.

Earn spread, commission, or subscription.

Case uses 333 first-year acquisitions.

Case mix: 500% student, 400% experienced, 100% specialized.

How much revenue does a babysitting service need to pay the owner?

Babysitting Service needs about $598k/month in platform revenue to support $125k/month owner pay in the researched case. That sits on top of $69k in fixed overhead and $242k in visible payroll, so the real test is gross margin per booking, not revenue alone. If cancellations rise or sitter costs sit inside the company, the revenue needed climbs fast.

Repeat families reduce acquisition pressure and stabilize income.

Fixed overhead and payroll set the break-even floor.

Compare low, base, and high babysitting service income scenarios

Owner income scenarios

Income moves with order volume, customer mix, and staffing load. As orders scale, profit can rise fast, but hiring, scheduling, support, and compliance costs rise too.

Low, base, and high owner income cases for planning.

Scenario

Low CaseDownside case

Base CasePlan case

High CaseUpside case

Launch model

This case assumes first-year volume and a thinner mix, so owner income stays modest.

This case assumes second-year traction, with steadier demand and a stronger mix.

This case assumes third-year scale, with much higher order density and stronger profit capacity.

Typical setup

About 4,375 orders a month, $2.381M booked care value, $598k platform revenue, $556k gross profit, and $353k visible operating costs leave about $125k planned owner pay and $204k pre-tax, pre-reserve profit capacity.

About 12,697 orders a month, $1.842M revenue, and about $1.294M visible profit capacity after the core operating load.

About 30,286 orders a month, $4.482M revenue, and about $3.651M visible profit capacity, but only with heavier staffing and tighter control.

Cost drivers

New customer volume

lower order mix

flat pricing

fixed staffing

compliance overhead

More orders

stronger repeat use

better mix

rising support load

steady CAC

Heavy order volume

premium mix

more repeat bookings

larger support team

compliance and scheduling load

Owner income rangeBefore owner reserves

$125k - $204kOwner pay

$1.29MVisible profit

$3.65MPeak capacity

Best fit

Use this to stress test an early launch with slow scale and tighter margins.

Use this as the main operating plan for a business that is scaling but still managing costs carefully.

Use this to test upside when demand is strong and the team can handle the extra load.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Babysitting Service Core Six Income Drivers

Booked Care Hours

Booked Care Hours

Booked care hours are the paid hours that actually get completed. The source model uses 4,375 first-year monthly orders instead of care-hour counts, so the real income test is how many booked hours turn into finished paid visits. Canceled hours do not pay overhead, but screening, scheduling, and support still cost money.

More completed hours lift booking value and commission revenue on every order. That matters for owner pay because each finished booking adds fixed and variable income, while no-shows and refunds cut margin. With 2,500 acquired buyers and repeat-order assumptions of 100, 250, and 400, completion rate is a direct cash-flow driver.

Track Completed Hours, Not Just Bookings

Track booked hours, completed hours, cancellations, and refund rate by buyer type. A simple control is completed-hours rate = completed paid hours / booked care hours. Watch it by occasional, regular, and premium families so you can see which segment actually turns into cash. If cancellations rise, forecasted commission and owner draw fall fast.

Cut gaps with reminders, backup sitter coverage, and clear cancellation rules. Tie staffing and marketing spend to completed paid hours, not just sign-ups, because failed bookings raise acquisition cost per paid hour. If you want stable take-home income, forecast from completed hours first, then stress-test a higher cancel rate before adding overhead.

Scheduling Efficiency

Scheduling Efficiency

Scheduling efficiency is how well open sitter time lines up with parent demand. In this model, the first year starts with 333 sitter acquisitions and 2,500 buyer acquisitions, so coverage quality decides how much demand becomes paid bookings instead of gaps, refunds, or churn. As the mix shifts from 500% student to 300% and experienced sitters rise from 400% to 550%, more requests should convert.

The effect is medium to high because missed bookings waste marketing spend. If a family cannot book when it needs care, revenue drops now and repeat orders weaken later. Better matching lifts completed revenue, protects gross margin, and helps the owner spread fixed overhead across more paid bookings instead of support tickets and refund work.

Track fill rate by time and zip

Measure fill rate — booked hours divided by requested hours — plus cancellations, time-to-match, and refund rate by hour, day, and zip code. Compare student and experienced sitter coverage against demand, because the shift from 500% student to 300% and experienced from 400% to 550% should improve match speed only if coverage sits where parents actually book.

Push buyer growth only where coverage is strong. If a slot stays thin, add sitters or limit promises before scaling ads. That keeps more bookings completed, lowers churn, and protects owner pay by turning acquisition spend into revenue instead of fixing failed matches.

Sitter Pay Spread

Sitter Pay Spread

Sitter pay spread is the gap between what parents pay and what stays after sitter compensation, vetting, and booking support. If the business pays sitters directly, that payout must be modeled too. The disclosed proxy shows 50% sitter vetting cost in year 1, dropping to 30% by the mature year, plus sitter subscription fees of $0, $15, and $25 by tier.

Here’s the quick math: more booked hours help only if sitter payouts and support costs stay below gross booking revenue. Inputs needed are booked care hours, average hourly rate, sitter pay rate, vetting cost, and tier mix. If pay rules are loose, owner income shrinks fast because every booking carries labor cost before fixed overhead is covered.

Track payout margin by sitter tier

Measure gross margin per booking and split it by sitter tier, since the $0, $15, and $25 subscription fees change net revenue differently across groups. Watch the share of bookings that need higher vetting, because the model’s proxy falls from 50% to 30% only if screening gets cheaper or more automated.

Keep a simple rule table for sitter pay, vetting, and booking support, then review it with counsel and an accountant. One bad payout rule can turn booked hours into thin cash flow. If direct pay rises faster than booking value, owner draw gets squeezed even when revenue looks strong.

Average Hourly Billing Rate

Average Hourly Billing Rate

Average hourly billing rate is the price parents accept per booking, and it only helps owner income if bookings still close and sitter pay still feels fair. In year one, the model uses $40 occasional, $55 regular, and $75 premium; by the mature year those move to $44, $63, and $87. Higher rates lift revenue and cash flow only when demand holds.

The key inputs are completed orders, tier mix, acceptance rate, and sitter compensation pressure. If premium mix grows from 100% to 150%, blended order value rises, but a rate hike that slows bookings or squeezes sitter pay can cut volume and reduce the owner’s draw even while posted prices look stronger.

Track rate acceptance before you raise prices

Watch booking conversion, tier mix, and sitter fill rate by zip code and time slot. Raise prices first on scarce premium hours, then compare completed bookings and repeat use over the next 30 days. If families accept the higher rate but sitters churn, the gain is short-lived because supply tightens and refunds or cancellations can rise.

Here’s the quick math: orders × average rate × accepted hours drives gross revenue, then sitter pay and support costs decide what reaches owner profit. Use small rate tests, not a blanket increase, and document where the higher price is coming from: real demand, better service, or a tighter sitter mix.

Track accepted vs. posted rate.

Test premium first, not all tiers.

Check sitter pay after each increase.

Measure repeat bookings by tier.

Fixed Operating Costs

Fixed Overhead

Fixed overhead is the monthly cost base that must be paid before the owner can take more than planned salary. In this model it is $69k/month, including $25k rent, $15k base payment processing, and smaller lines for insurance, software, legal and compliance, utilities, supplies, and professional services. The itemized lines shown add to $43.9k, so every recurring bill needs tracking.

If visible payroll for the CEO and CTO adds $242k/month, the cash load rises to $311k/month before any extra owner draw. That means booked care hours have to clear a much higher hurdle, and weak pricing or missed bookings hit take-home pay fast. Keep sitter pay and transaction costs separate so break-even stays clean.

Measure the monthly burn

Track fixed overhead as a separate monthly line. Use one check: fixed overhead + visible payroll versus monthly contribution after sitter pay and transaction costs. If bookings grow but the fixed base does not fall, owner pay stays trapped until the business clears the full cash burn.

$69k core overhead target

$242k executive payroll if booked

Separate variable sitter costs

Review rent and processing fees

Set approval rules for new recurring spend. Every tool, service, or lease line should show how many extra completed bookings it must support. That keeps fixed costs from eating the margin that should fund owner income.

Repeat Family Bookings

Repeat Family Bookings

When families book again, the business needs fewer new parents to hit the same revenue. In year one, repeat orders are assumed at 100 for occasional buyers, 250 for regular buyers, and 400 for premium buyers. By the mature year, that rises to 120, 310, and 500, so the owner gets steadier cash flow and less pressure on ad spend.

This driver also improves forecast quality because the buyer mix shifts from 400% combined regular and premium buyers to 600%. That matters for profit, since repeat bookings usually cost less to win than first-time families. The key inputs are repeat order rate, buyer mix, completion rate, and referral rate. Trust, safety screening, reliability, and parent referrals are what make the math work.

Track Repeat Rate by Buyer Tier

Measure repeat bookings by occasional, regular, and premium families, not just total orders. If premium families are not moving toward 500 repeat orders by the mature year, the model will lean too hard on new customer acquisition and owner pay will be less predictable.

Test what drives return use: faster rebooking, better sitter matches, and simple parent referrals. Keep an eye on first-year repeat assumptions of 100, 250, and 400, then compare them with actual monthly cohorts. If repeat booking lags, marketing costs stay high and margin stays thin.