Biogas Production Owner Income: $348M Before Debt And Reserves

Using the researched assumptions, a biogas production business can produce strong plant-level cash flow, but owner income depends on debt service and reserve policy Year 1 revenue is $594M, with $348M of EBITDA before debt, taxes, reserves, and owner pay, a 586% margin after listed costs By Year 5, revenue reaches $1409M and EBITDA reaches $997M, a 708% margin Actual owner take-home is what remains after loan payments, maintenance reserves, working capital, reinvestment, and any approved distributions

Owner income$4.7MNet margin79%–81%Revenue for target pay$5.9MBusiness difficultyHard

Want to test your biogas owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from monthly revenue, gross margin, operating costs, reserves, and target owner pay.

!

Planning note: Research-based planning estimate only. Actual owner take-home is not guaranteed salary, tax advice, or owner distribution advice.

Want to see owner income in the Biogas Production model?

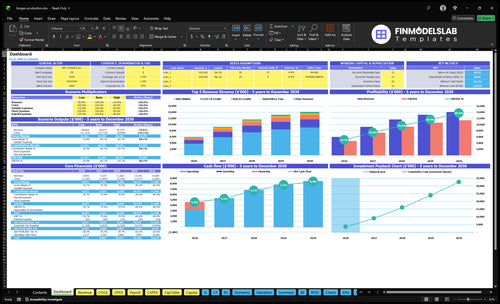

This screenshot in the Biogas Production Financial Model Template shows revenue, EBITDA before debt/reserves, costs, reserves, and owner take-home assumptions; open it.

Owner-income model highlights

Owner cash: scenarios

Charts: RNG, credits, biofertilizer

Charts: costs, margins, cash

Year 1: $594M/$348M

Year 5: $1,409M/$997M

How much can a biogas plant owner make per year?

A Biogas Production plant owner’s yearly take-home is cash left after debt service, taxes, reserves, reinvestment, and any owner pay, not the headline profit number; see What Is The Current Growth Rate Of Biogas Production For Your Business? for growth context. The researched model shows $348M EBITDA in Year 1, $789M in Year 3, and $997M in Year 5, while revenue rises from $594M to $1.409B.

Owner Cash Reality

EBITDA means pre-debt operating profit

Year 1 margin: about 58.6%

Year 5 margin: about 70.8%

Distributions come after required funding

Pay Role Check

Owner-operator may replace management payroll

Listed General Manager role: $150k

Avoid counting both as owner income

Passive owners wait for distributions

How does a biogas production business make money?

Biogas Production makes money by selling RNG, biofertilizer, RIN D3 credits, LCFS credits, and voluntary carbon offsets. In the provided model, Year 1 revenue is $375M RNG, $250k biofertilizer, $630k RIN, $1125M LCFS, and $180k offsets; Year 5 rises to $899M, $567k, $1395M, $2635M, and $500k. Tipping fees can add more revenue if contracted, but they are not included here.

Core sales

RNG: $375M in Year 1

RNG: $899M in Year 5

Biofertilizer: $250k to $567k

Revenue starts at product launch

Credit revenue

RIN D3: $630k to $1395M

LCFS: $1125M to $2635M

Offsets: $180k to $500k

Tipping fees: extra if contracted

How big does a biogas plant need to be to make money?

For Biogas Production, size the plant to lock in enough contracted volume and gas yield to clear operating break-even; with fixed overhead plus the listed payroll at $1,193M and gross margin at 787%, Year 1 break-even before debt and reserves is about $152M of revenue. The quick math is: required revenue = fixed costs + payroll + owner target pay + debt + reserves, then divide by contribution margin. Year 1 planned revenue is $594M, so the core model clears that line, but debt service can change the answer fast.

What sets size

Contracted volume sets the floor

Gas yield drives output

Credit value lifts revenue

Fixed cost sets break-even

What changes the answer

Debt load can move break-even

Reserve policy raises cash need

Owner target pay belongs in the formula

$594M planned Year 1 revenue

Want the six biogas income drivers?

1

Feedstock Volume

150K-310K MMBtu

More contracted waste means more RNG output, and higher run rates spread fixed overhead across more production.

2

Gate Fees

High

Tipping fees add cash before gas sales, so weak gate pricing can wipe out margin fast.

3

RNG Offtake

$3.8M-$9.0M

RNG sales move from 150,000 MMBtu at $25 to 310,000 at $29, so contract price and offtake set the core revenue line.

4

Credit Stack

$1.9M-$4.5M

RIN D3 and LCFS credits scale with output, and that stack adds real EBITDA on top of gas sales.

5

Plant Uptime

$618K

Downtime still burns the $618K annual overhead base, so uptime and maintenance protect take-home cash.

6

Debt Service

$348M-$997M

Debt service, reserves, and reinvestment decide how much of the EBITDA path becomes owner cash.

Biogas Production Core Six Income Drivers

Contracted Feedstock Volume And Utilization

Contracted Feedstock Volume

Steady contracted feedstock is the base load for the digester: more incoming tons means more renewable natural gas (RNG), more biofertilizer, and better spread of the $515k/month fixed overhead. In this model, RNG rises from 150,000 MMBtu in Year 1 to 310,000 MMBtu in Year 5, a 160,000 MMBtu lift, while biofertilizer grows from 5,000 tons to 10,500 tons. That scale-up can lift owner cash before debt and reserves if utilization stays high.

The key inputs are contracted tons, contamination rate, and uptime. Here’s the catch: dirty feedstock can drive more lab tests, hauling, digestate handling, downtime, and rejection risk, which cuts margin even when volume looks strong. More tons only help if they are usable. One clean metric to watch is usable feedstock per operating day.

Track Usable Tons, Not Just Tons

Measure delivered tons, accepted tons, and contamination % by source. Separate farm, food, and municipal loads so you can spot the streams that raise testing and handling cost. If acceptance drops, your model should also lower gas, credits, and biofertilizer output, not just revenue. That keeps cash flow and owner pay from looking better than they are.

Use contracts that define quality specs, rejection rules, and who pays for extra hauling or disposal. If a stream needs more sorting or testing, price that cost in up front. Better feedstock quality usually means fewer shutdowns, steadier utilization, and more cash left after operating costs.

1

Tipping Fee Economics

Tipping Fee Economics

Tipping fees are what waste generators pay to dispose of organic material, and they can add cash before RNG sales start. Because the model does not include tipping-fee revenue, treat it as an editable input, not assumed income. That matters for owner pay, since cash flow can improve well before energy revenue ramps.

Here’s the risk: some manure or organic streams may need procurement, transportation, or handling costs instead of paying a fee. So the real metric is net dollars per ton after hauling, contamination, and contract terms. With fixed overhead at $515k per month, weak gate economics can pressure cash fast.

Measure Net Fee, Not Gross Fee

Track the contract as fee per ton minus hauling cost, contamination penalties, and any procurement or handling cost. Test each stream by contracted tons and contract term, since a long, reliable contract improves forecast quality and reduces cash swings.

Build one sensitivity table with four cases: positive fee, zero fee, negative net fee, and downtime impact. That shows whether the stream helps cover fixed overhead and leave cash for debt, reserves, and owner draw. If the feedstock is dirty, model higher testing, rejection, and rework costs up front.

Fee per ton

Contracted tons

Contamination penalties

Hauling cost

Contract term

2

Gas Yield, Pricing, And Offtake

Gas Yield, Pricing, And Offtake

Your RNG income is simple on paper: MMBtu produced × realized price. Using the model inputs, sales rise from 150,000 MMBtu at $25 in Year 1 to 310,000 MMBtu at $29 in Year 5, so both volume and price matter. The owner’s cash grows only if the plant keeps methane yield high and the offtake buyer takes gas without curtailment.

This driver also depends on methane yield, upgrading choice, interconnection, and offtake terms. Keep RNG, electricity, and heat in separate buckets; pricing and infrastructure differ. Weak yield or curtailment cuts gas sales and credit generation at the same time, which can shrink profit and the cash available for owner pay.

Track Realized RNG Value

Track realized $/MMBtu and gas volume each month, not just contract headline price. Here’s the quick math: 150,000 × $25 = $3.75M; 310,000 × $29 = $8.99M. That spread shows how much income moves with yield and pricing, before fixed costs and reserves. A long, steady offtake usually beats a short deal with volume risk.

Test contracts for minimum volumes, price resets, and who bears interconnection risk. If the plant has to flare or curtail gas, cash drops fast because the molecule never gets sold. One clean line: more usable gas at a locked price pays the owner twice, once in revenue and again in better fixed-cost absorption.

3

Renewable Credits And Incentives

Renewable Credits And Incentives

Renewable Identification Numbers (RINs), California Low Carbon Fuel Standard (LCFS) credits, and voluntary offsets can swing profit fast, but they are scenario inputs, not guaranteed income. Using the model’s Year 1 volumes, credits add about $1.935M before fees: $630k from 225,000 RIN D3 credits, $1.125M from 15,000 LCFS credits, and $180k from 12,000 offsets.

What this estimate hides is the net haircut: policy risk, pathway approval, verification, brokerage, registry fees, and market price drops. By Year 5, the model shows $453M of credit and offset revenue, so even small changes in eligibility or pricing can shift owner take-home more than normal operating savings.

Track the net credit stack

Model credits by type, then strip out every fee before you count cash for the owner. Here’s the quick math: gross credit value matters, but the real number is verified volume × market price - brokerage - registry - verification - compliance. If a pathway is late or a batch fails verification, the cash hit shows up right away.

Track gross and net by credit type.

Separate eligible from verified volume.

Update prices monthly, not yearly.

Forecast fee drag before owner draws.

4

Uptime, Maintenance, And Downtime

Uptime And Downtime

Reliability protects revenue and margin. If the plant is down, RNG (renewable natural gas) sales, biofertilizer output, RIN credits, LCFS credits, and offsets all fall at once, but labor and overhead keep running. The main inputs here are utilization, unplanned downtime, contamination, and process stability, because they drive both output and the maintenance load.

Here’s the quick math: with $515k per month of fixed overhead, one idle day costs about $17.2k before you count lost sales or extra repair work. Add variable operating costs like gas upgrading chemicals, grid injection fees, testing, utilities, digestate processing, verification, brokerage, legal, and reporting fees, and downtime hits cash flow fast.

Measure Downtime By Lost Output

Track hours lost, contamination rate, maintenance spend, and the lost RNG MMBtu and biofertilizer tons tied to each outage. If process instability rises, lower the utilization assumption and raise maintenance cost in the model right away. That keeps owner profit and draw estimates honest.

Log downtime by cause.

Separate planned and unplanned stops.

Test contamination on every inbound stream.

Forecast lost credits with outages.

Use those logs to set reserve levels for repairs and compliance timing. If downtime starts cutting output more than once a month, the business is not just losing revenue; it is burning through the fixed cost base faster and shrinking what is left for owner pay.

5

Debt Service, Reserves, And Reinvestment

Debt service, reserves, and reinvestment

EBITDA is not owner pay. Year 1 EBITDA before debt, taxes, reserves, and owner pay is $348M, and Year 5 is $997M. Cash to the owner only comes after loan payments, replacement reserves, working capital, taxes, and reinvestment, so a strong EBITDA line can still leave thin distributable cash.

The model needs editable fields for the debt schedule and maintenance reserve, because neither is provided. That matters when equipment replacement, compliance timing, credit verification delays, or cash swings hit. If reserves are too light, owner draws look fine on paper but fail in a repair month.

Pay the owner last

Use a cash waterfall: EBITDA → debt service → reserves → taxes → reinvestment → owner draw. Track monthly principal and interest, minimum cash, and reserve funding so distributions only happen after the floor is met. One missed reserve can turn a good month into a cash gap.

Stress test debt payment size, reserve rate, and credit timing. Set a buffer for equipment replacement and verification lag, then tie owner pay to the cash left after those uses. If credit cash lands late, the reserve should keep maintenance and compliance funded without forcing a draw cut.

6

Compare low, base, and high biogas owner income scenarios

Owner income scenarios

Owner income moves with plant ramp, credit sales, and staffing. These cases compare Year 1, Year 3, and Year 5 operating levels.

Three planning cases for pre-debt owner income.

Scenario

Low CaseLow Case

Base CaseBase Case

High CaseHigh Case

Launch model

This is the lower earnings path, tied to the Year 1 ramp and early production mix.

This is the modeled middle path, tied to Year 3 output and steadier plant use.

This is the stronger earnings path, tied to Year 5 output and fuller plant capacity.

Typical setup

Year 1 output is 150,000 RNG MMBtu, 5,000 biofertilizer tons, 225,000 RIN credits, 15,000 LCFS credits, and 12,000 offsets, with $5.94M revenue, $618k fixed overhead, $575k payroll, and 58.6% EBITDA margin.

Year 3 output reaches 275,000 RNG MMBtu, 9,000 biofertilizer tons, 412,500 RIN credits, 27,500 LCFS credits, and 22,000 offsets, with $11.66M revenue, $618k fixed overhead, $815k payroll, and 67.6% EBITDA margin.

Year 5 output reaches 310,000 RNG MMBtu, 10,500 biofertilizer tons, 465,000 RIN credits, 31,000 LCFS credits, and 25,000 offsets, with $14.09M revenue, $618k fixed overhead, $815k payroll, and 70.8% EBITDA margin.

Cost drivers

RNG output

credit mix

feedstock handling

fixed overhead

payroll load

Higher volume

stronger credit pricing

fixed overhead

added staff

compliance load

Peak utilization

better credit pricing

overhead dilution

full staffing

compliance and brokerage

Owner income rangeBefore owner reserves

$4.7MLow income

$9.3MBase income

$11.4MHigh income

Best fit

Use this to stress-test the first operating year before debt and reserve needs.

Use this as the main operating case for planning, lenders, and investor talks.

Use this to test upside if pricing holds and the plant runs near capacity.

!

Planning note: These are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.