How Much Blockchain Business Owners Make: $180k Salary Plan

You’re modeling founder pay before the business has stable cash flow, so separate salary from profit This five-year US planning view covers $99 to $1,999 monthly pricing, transaction fees, one-time setup fees, $137k in monthly fixed costs, payroll, reserves, and reinvestment It excludes guaranteed salaries, token speculation, investment returns, and tax advice

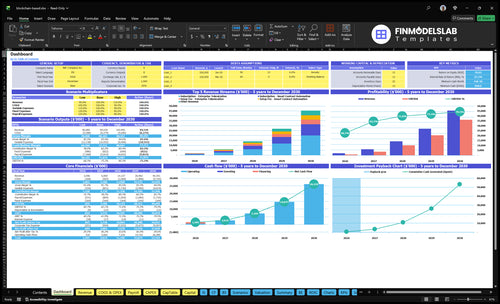

Owner income$0-$180kNet margin47%Revenue for target pay$944kBusiness difficultyHard

Want to test your founder pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margins, payroll, taxes, reserves, and reinvestment.

Want the six main income drivers?

1

Revenue Mix

$409

A $409 weighted monthly price keeps the base strong, and more sales of higher-tier products lifts take-home fast.

2

Acquisition Cost

$250

At a $250 customer acquisition cost, every drop in lead cost improves cash flow before recurring revenue catches up.

3

Margin Mix

91%/82%

Cloud and network costs leave about 91% gross margin, and the full stack still holds about 82% contribution before fixed payroll.

4

Paid Conversion

15%-24%

Better free-trial to paid conversion grows recurring revenue without adding the same CAC to each customer.

5

Compliance Load

$137K/mo

The fixed-cost base runs about $137K a month, including legal, cybersecurity, and R&D, so slow ramp cuts owner income fast.

6

Founder Pay

$180K

The planned $180K CEO salary sits inside about $460K of shown payroll, so owner take-home depends on reinvestment discipline.

How do I check owner income in the Blockchain-Based Business financial model?

Which blockchain business income scenario scales best?

The subscription and enterprise-contract models scale best for a Blockchain-Based Business because revenue repeats. Year 1 pricing can run from $99 to $1,999 per month, with setup fees of $0, $1,500, or $5,000; usage fees at $0.05 to $0.10 per transaction add upside, but one-time consulting is better for early cash than for long-term scale.

Best revenue mix

Subscription revenue repeats.

Enterprise contracts lift ticket size.

$99 to $1,999 monthly plans.

Setup fees: $0, $1,500, $5,000.

Scaling risk

Consulting funds early delivery.

Product scales better long term.

Usage fees: $0.05 to $0.10.

Watch support, security, compliance costs.

How much should a blockchain startup founder pay themselves?

A Blockchain-Based Business founder should cap pay below the modeled $180k/year until recurring revenue covers delivery costs and $137k/month fixed overhead; see What Is The Main Metric That Reflects Blockchain-Based Business'S Growth? before approving owner draws. Here’s the quick math: $180k/year equals $15k/month, and that salary should not drain runway ahead of payroll, security, compliance, reserves, or customer delivery.

Safe founder pay

Use $15k/month only when covered

Protect $137k fixed overhead first

Fund payroll before owner draws

Hold cash if pilots stall

Cash guardrails

Keep delivery costs funded

Preserve compliance and security budgets

Track the $460k core spend

Reinvest if development runs long

How much revenue does a blockchain business need to pay the owner?

If the goal is to pay the owner $180k in year 1, the Blockchain-Based Business needs about $944k in annual revenue at an 82% contribution margin. Here’s the quick math: that margin, after 9% direct costs and 9% variable selling costs, has to cover the full cost stack, so revenue quality matters if churn, delays, or support costs rise.

Revenue math

82% contribution margin

$180k owner pay

$944k revenue target

9% direct costs

Margin watchouts

Churn cuts recurring revenue fast

Delays push support costs up

Usage fees can lift ARPU

Fixed costs must stay tight

Key Takeaways

Subscription mix drives cash more than one-time fees.

Faster acquisition protects payroll and sales capacity.

Low cloud and network costs keep margins high.

Retention and compliance protect founder take-home pay.

Compare lean, base, and high-scale blockchain owner income scenarios

Owner income scenarios

Owner income changes fast here because CAC, conversion, mix, and payroll decide how much cash is left after launch. Lean looks tight; Year 5 has much more room.

Compare cautious, modeled, and upside owner income cases.

Scenario

Lean CaseLean Case

Base CaseBase Case

High CaseHigh Case

Launch model

A lean launch stays below the revenue needed to cover salary, payroll, marketing, and platform costs.

The modeled launch converts Year 1 traffic with $250 CAC and a $409 weighted monthly subscription per customer.

The upside case uses Year 5 pricing and CAC, with stronger mix, higher margin, and a much larger marketing budget.

Typical setup

Revenue stays under roughly $944k, so an 82% contribution margin does not fully absorb the $180k CEO salary, $460k payroll, $164.4k fixed costs, and $150k marketing budget.

Year 1 marketing can fund about 600 customers, with a mix led by Secure Data Ledger and a 15% trial-to-paid rate.

Year 5 assumes $180 CAC, a $15M marketing budget, an $886 weighted monthly subscription price, 94% gross margin, and 87% contribution margin before overhead.

Cost drivers

Revenue density

payroll load

marketing spend

fixed costs

contribution margin

CAC efficiency

trial conversion

product mix

subscription price

marketing budget

Lower CAC

larger marketing budget

higher price mix

gross margin

contribution margin

Owner income rangeBefore owner reserves

Below salary supportLean Case

Salary plus modest drawBase Case

Reserve-adjusted upsideHigh Case

Best fit

Use this to test a cautious launch with slow traction and tight cash.

Use this as the core operating plan for Year 1.

Use this to test upside cash generation after scale, reserves, and reinvestment.

!

Planning note: Ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Blockchain-Based Business Core Six Income Drivers

Revenue Model And Pricing

Pricing Mix Drives Owner Pay

Stable pricing funds owner pay. The Year 1 monthly plans are $99 for secure data ledger, $499 for smart contract automation, and $1,999 for enterprise tokenization. With that mix, weighted subscription revenue is about $409 per customer per month before one-time and transaction fees, so each retained account matters more than raw logo count.

The mix shift matters. If enterprise tokenization rises from 10% to 25% of the mix and renewals hold, revenue quality improves because more cash comes from high-price recurring accounts. What this hides: if renewals slip, a higher sticker price does not protect owner pay, because billed revenue still has to be collected.

Track Cash, Not Just Sales

Measure the pricing stack, not just total sales. Track customers by tier, monthly cash collected, renewal rate, and one-time or transaction fees. A simple check is whether collected recurring revenue stays near the $409 weighted monthly average per customer; if it falls, owner pay pressure shows up fast.

Review tier mix monthly

Protect enterprise renewals

Bill and collect on time

Test upsells only when support and uptime stay clean. Higher-priced enterprise accounts can lift monthly revenue fast, but they also raise renewal risk if service slips. Keep the forecast on cash collected, not booked sales, because that is what pays owner draw and leaves anything left for distributions.

Founder Role, Payroll, And Reinvestment

Founder Payroll

Payroll can decide whether profit becomes take-home. In Year 1, the core team is a $180k CEO, a $160k lead blockchain developer, and a $120k senior enterprise sales manager, for $460k before any added hires. That cost has to be covered by recurring subscription cash, or the owner’s draw gets squeezed.

The key split is owner labor replacement cost versus true distributable profit. If the founder personally covers developer, sales, support, or compliance work, cash pay may look better, but the workload gets heavier and missed execution can hit renewals, uptime, and sales conversion.

Track Payroll Against Cash Collection

Measure payroll as a share of collected recurring revenue, not booked sales. Here’s the quick check: compare the $460k base payroll, plus any added hires, with monthly cash in from subscriptions and fees. If collections lag, founder pay should wait; if headcount grows before renewals are stable, burn rises fast.

Track founder role hours by function.

Separate salary from profit draw.

Model replacement cost by hire.

Test hiring only after renewals hold.

What this estimate hides: support load, compliance work, and sales follow-up can quietly land on the founder. If one person becomes the backup for too many jobs, the business may save payroll on paper but lose speed, quality, and cash discipline.

Security, Legal, And Compliance Burden

Security, Legal, and Compliance Costs

This driver cuts into owner income because it is real overhead, not optional polish. Here, the base burden is $1,200 per month for cybersecurity and compliance plus $1,500 per month for legal and accounting retainers, or $2,700 per month before audits, incident response, insurance, and regulatory reviews.

That is $32,400 a year before any project-based legal work. For a subscription platform, these costs reduce distributable cash even when sales look strong, so owner pay should be set after these controls are funded, not before. If they are skipped, reported profit can overstate safe take-home pay.

Track The Full Compliance Run Rate

Measure this as a fixed monthly run rate plus event-based costs. Track cybersecurity and compliance, legal and accounting retainers, smart contract audits, insurance, and incident response separately, then roll them into the cash forecast. The key test is simple: can recurring revenue cover these costs before owner draws?

Use a release and deal checklist. Every major contract, code change, or regulatory shift should trigger review cost, not surprise cost. If a new enterprise deal needs extra legal review, price it into the contract or treat it as lower-margin revenue. That keeps owner pay tied to cash left after required protection spend.

$2,700 monthly base overhead

$32,400 annual base overhead

Budget audits and incident response separately

Link owner pay to free cash, not gross sales

Customer Acquisition And Contract Conversion

Customer Acquisition And Contract Conversion

Delayed sales delay payroll safety. With a $150k Year 1 marketing budget and $250 CAC, the model can fund about 600 customer acquisitions if CAC holds ($150,000 / $250). The real test is not traffic alone; it’s turning visitors into trials at 30% and trials into paid contracts fast enough to bring cash in before payroll and support costs hit.

By Year 5, CAC improves to $180, visitor-to-trial reaches 45%, and trial-to-paid reaches 240% as supplied in the model. Better conversion lowers selling cost per customer and raises cash collection speed, which gives the owner more room for salary and distributions. Slow closes do the opposite: they push revenue out and squeeze take-home pay.

Track CAC, close rate, and cash timing

This driver includes marketing spend, CAC, visitor-to-trial conversion, trial-to-paid conversion, sales cycle length, and cash collection timing. Here’s the quick math: if spend stays at $150k and CAC drops from $250 to $180, the same budget buys more customers and faster payback. That means more cash left after sales effort and less pressure on owner pay.

Measure CAC by channel monthly.

Track trial close lag in days.

Watch cash collected vs. booked sales.

Test offer changes on trial-to-paid.

What this hides: if leads are cheap but contracts collect slowly, reported growth can overstate cash safety. Tighten follow-up, shorten approvals, and price the sales effort into the forecast so owner pay is based on collected cash, not just pipeline value.

Gross Margin And Infrastructure Cost

Gross Margin and Infrastructure Cost

Cloud, node, network, API, DevOps, and support costs hit before owner pay. Here’s the quick math: Year 1 direct costs are 6% cloud plus 3% blockchain network fees, so gross margin is 91%. That margin is strong, but only if delivery costs stay tied to usage and not fixed overhead.

By Year 5, direct costs drop to 4% cloud and 2% network fees, lifting gross margin to 94%. Track revenue, active customers, transaction volume, and support load so you can separate true delivery cost from rent, tools, legal, R&D maintenance, admin, and cybersecurity. If delivery spend creeps up, owner pay shrinks first.

Track Delivery Cost Per Dollar of Revenue

Measure gross margin as revenue minus direct delivery cost. Use the right inputs: cloud spend, blockchain fees, API calls, support tickets, and DevOps time. If those costs rise faster than subscription revenue, the business may still look busy while take-home income stalls.

Watch cloud cost as a percent of revenue.

Watch network fees per transaction.

Separate support and overhead every month.

Keep a clean line between variable delivery costs and fixed overhead. That way, a 91% to 94% gross margin target stays real, and you can see how much profit is left before owner salary, reinvestment, and reserve build-up.

Retention And Recurring Revenue

Recurring Cash From Renewals

When renewals hold, owner pay is safer because cash keeps arriving each month. This model depends on $409 of weighted subscription revenue per customer per month, while one-time fees are only $0, $1,500, or $5,000 by product line. If churn, uptime issues, support load, or failed renewals rise, the cash that funds the $180k CEO salary and distributions shrinks fast.

Here’s the quick math: subscriptions drive repeat cash, but setup fees do not repeat. The key inputs are active customers, renewal rate, churn, and support cost per account. High sales with weak retention still leaves a thin cash base, so booked revenue can look fine while take-home pay gets less secure.

Protect Renewal Cash

Track gross retention and failed renewals by product line, then watch uptime and ticket volume weekly. If support load climbs, churn usually follows. Tie forecasts to collected recurring cash, not booked setup fees, because the owner’s draw depends on what actually renews and clears.