How Much Can a Commercial Glazing Contractor Owner Make at $1047M Revenue

You’re planning owner pay in a business with large glass packages, labor swings, and slow construction cash flow Using the researched model, first-year revenue is $1047M, direct gross margin is about 801%, and owner income depends on job mix, labor productivity, overhead, reserves, and reinvestment This is planning math before personal taxes, not a guaranteed salary

Owner income$7.0MNet margin67%-73%Revenue for target pay$10.5MBusiness difficultyHard

Want to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

Want the six income drivers that matter most?

1

Bid Accuracy

$300K-$800K

On $10.5M Year 1 revenue, small bid misses can wipe out six figures because price, field labor, and a 3.5% sales and bonding load hit every job.

2

Field Productivity

$250K-$700K

Faster crew output lowers labor hours and rework, so more of each contract turns into take-home profit instead of jobsite waste.

3

Project Mix

$400K-$1.0M

More curtain walls and structural glass lift ticket size, while a heavier storefront mix usually means lower dollars per job and thinner income.

4

Backlog Depth

$500K-$1.2M

A steadier backlog keeps crews, trucks, and cranes busy, which protects revenue flow and spreads fixed costs over more installed work.

5

Overhead Load

$250K-$500K

The $144K annual rent plus fleet, software, insurance, and office payroll come out before profit, so overhead discipline feeds owner income fast.

6

Cash Reserves

$100K-$300K

Strong cash reserves help cover retainage delays and project spikes, so the company can buy materials and keep work moving without borrowing stress.

Want to check owner income in the Commercial Glazing Contractor model?

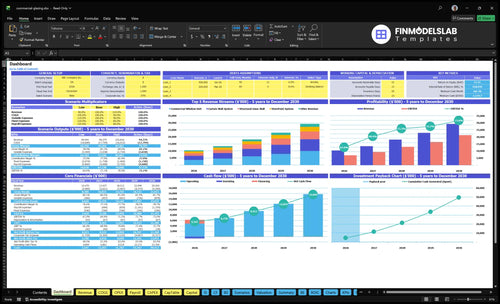

Commercial Glazing Contractor can be profitable, but only if it protects bid margin, labor productivity, backlog quality, and cash reserves. The researched model shows revenue rising from $1,047M in Year 1 to $2,926M in Year 5, with gross profit climbing from $839M to $2,392M. That can support owner income, but slow general contractor payments can still turn accounting profit into cash stress.

Profit drivers

Protect bid margin on every job.

Keep crews productive on site.

Keep backlog quality high.

Fund estimators and project managers.

Cash pressure points

Bonding costs can tie up cash.

Deposits help fund early work.

Retainage delays final collections.

Slow payments can strain working capital.

How much revenue does a commercial glazing contractor need to pay the owner?

If you’re setting pay for a Commercial Glazing Contractor, use target-pay math, not salary averages: owner pay plus overhead, reserves, debt, and non-owner management cost, divided by contribution margin. Using the provided Year 1 contribution after direct COGS, sales commissions, and bonding at 766% of revenue, a $250k owner-pay target before personal taxes points to about $326k of revenue before fixed overhead and reserves. Keep base compensation separate from profit distributions.

Target-pay math

$250k owner-pay target

766% contribution rate

About $326k revenue

Before overhead and reserves

What to add next

Fixed overhead still sits above this

Keep reserves separate from pay

Include debt service in the model

Split compensation from distributions

How much can a small commercial glazing contractor owner make?

A small Commercial Glazing Contractor owner’s take-home can’t be pinned down from revenue alone; in the Year 1 model, the business shows $1.047M revenue, $208k direct COGS, and $802k contribution before fixed overhead, reserves, taxes, and owner pay. For setup context, see How Do I Launch A Commercial Glazing Contractor Business?, but the real answer depends on whether the owner is still estimating, supervising, and closing out jobs.

Owner Pay Drivers

Start with $802k contribution

Subtract fixed overhead next

Hold cash for materials

Watch retainage and timing

Scale Risks

Bigger jobs need PMs

Insurance costs rise

Lifts tie up cash

Revenue does not equal take-home

Key Takeaways

Small scope misses can erase gross profit fast.

Labor overruns hit cash before taxes or reserves.

Better backlog beats busy backlog on margin.

Cash reserves must fund retainage and warranty risk.

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Owner income rises fast when project mix shifts from windows to curtain walls and higher-value glass systems. The spread between low, base, and high cases is mostly volume, pricing, and overhead.

Scenario view of owner income by operating scale.

Scenario

Low CaseLow Case

Base CaseBase Case

High CaseHigh Case

Launch model

This is the Year 1 scale case, with about $10.47M revenue, 80.1% gross margin, and 3.5% sales commission plus bonding.

This is the Year 3 scale case, with about $18.21M revenue, 81.0% gross margin, and 3.3% sales commission plus bonding.

This is the Year 5 upside case, with about $29.26M revenue, 81.7% gross margin, and 3.0% sales commission plus bonding.

Typical setup

The owner stays active in estimating and field oversight while the business handles 120 curtain wall systems, 800 commercial window units, and lighter first-year volume.

The business supports 200 curtain wall systems and 1,300 commercial window units, with more project management, design, and coordination capacity.

The company reaches 300 curtain wall systems and 2,000 commercial window units, with a larger project team and more owner focus on bigger bids.

Cost drivers

Year 1 volume

80.1% gross margin

3.5% commission plus bonding

hands-on owner oversight

fixed payroll and fleet costs

Year 3 volume

81.0% gross margin

3.3% commission plus bonding

added PM and design staff

overhead and reserves

Year 5 volume

81.7% gross margin

3.0% commission plus bonding

larger project team

higher reinvestment needs

Owner income rangeBefore owner reserves

$6.3M - $7.7MLow range

$11.7M - $14.3MBase range

$19.2M - $23.5MHigh range

Best fit

Use this to stress-test a first-year team where the owner is still in the field and sales cycle stays moderate.

Use this as the mid-case planning point for a growing contractor with repeat work and a fuller office team.

Use this when testing larger backlog, tighter execution, and enough cash to keep crews, equipment, and bonding capacity ahead of growth.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Commercial Glazing Contractor Core Six Income Drivers

Estimating Accuracy And Bid Margin

Bid Accuracy

When a fixed-price bid misses glass systems, hardware, sealants, lifts, labor hours, freight, or install complexity, the error hits gross margin first. Gross margin is the money left after direct project costs. In this model, Year 1 gross profit is about $839M on $1047M revenue, so every margin point is worth about $1047k. Bad scope cuts owner take-home fast.

Curtain wall systems at $25,000 and structural glass walls at $45,000 need tight takeoff control. Missed exclusions and weak change orders turn revenue into unpaid work, and unpaid work still uses labor, freight, and lift time. One clean rule: if it is not in the bid, it is not in the margin.

Scope and Change Order Control

Track the inputs that change bid margin: unit counts, quoted labor hours, freight, lift days, sealant and hardware allowances, and every exclusion. If the estimate is fixed-price, build in a written change-order path, the formal price bump for scope changes, before work starts. That is where owner pay gets protected.

Compare bid vs. actual labor hours.

Separate material and freight allowances.

Price install complexity by job.

Document exclusions before award.

Issue change orders fast.

If change orders lag, the crew keeps working while cash stays trapped in the job. That is how a strong quote turns into weak take-home.

Working Capital, Retainage, And Reserves

Working Capital, Retainage, And Reserves

Accounting profit is not cash. In commercial glazing, the owner often pays for glass, aluminum, freight, shop drawings, lifting, protection, and warranty items before the general contractor cash arrives. That means retainage, slow pay, deposits, debt service, and warranty risk can eat take-home income even on profitable jobs.

Model the real cash load by project type. Use 20% project-specific insurance for curtain wall work and a 5% warranty reserve for storefront systems. If those costs are not funded before distributions, owner pay becomes a timing gamble, not a profit share.

Fund Cash Before Owner Draw

Track cash by job, not just gross margin. Build a simple forecast for each contract: contract value, retainage, deposit timing, direct costs, insurance, warranty reserve, and debt service. If the job is “profitable” but cash-negative, skip owner draws.

Hold back distributions until each project has covered its funded costs and reserve targets. Watch the jobs with the most front-loaded spend, because curtain wall work can tie up more cash than smaller storefront work. That control protects pay, keeps vendors current, and lowers the odds that one delayed GC payment hits the whole business.

Project Mix And Contract Size

Project Mix And Contract Size

Project mix is the share of work you sell by contract size and product type: $45,000 structural glass walls, $25,000 curtain wall systems, $12,000 skylight assemblies, $9,000 storefront systems, and $4,500 commercial window units. Bigger jobs can add more gross profit dollars, but they also need more engineering, logistics, insurance, and cash tied up before payment.

For the owner, the mix changes take-home income through margin and cash timing. A book full of large packages can look strong on revenue, but slow billing and higher working capital can delay draws. Smaller storefront and window work can turn faster, but only if volume stays high enough to cover fixed overhead and field time.

Track Mix By Dollar And Cash Need

Measure contract count, average contract size, gross margin by job type, and days to bill. Here’s the quick check: compare revenue mix against the cash you must fund for drawings, freight, lifts, and labor before the GC pays. If large jobs stretch cash, they can support profit on paper but still squeeze owner pay.

Separate large and small job margins.

Watch change order coverage closely.

Forecast cash by project type.

Keep volume discipline on small work.

Use mix to set a floor on owner draw. If the backlog shifts toward $45,000 and $25,000 contracts, keep more reserves for insurance, engineering, and delayed collections. If it shifts toward $4,500 to $9,000 work, protect margin with tight scheduling and low rework.

Overhead And Equipment Burden

Overhead Must Be Recovered

$12,000/month rent means $144k/year is due before the owner sees real take-home. Add 20% sales commissions and 15% bonding fees in Year 1, and overhead starts eating margin fast. The key inputs are billed revenue, contract count, commission rate, bonding cost, and how much each job must carry in support costs.

Revenue only helps if the work finishes with enough gross profit to cover overhead. As the team scales, estimators, project managers, office staff, vehicles, tools, safety compliance, insurance, licenses, and lift rentals can push fixed burden up faster than sales. If a job doesn’t pay for that load, the owner’s draw shrinks even when topline grows.

Track Burden Per Job

Measure overhead recovery on every project, not just at month-end. One clean rule: if the job can’t pay its share of rent, commissions, bonding, and equipment support, it is not helping owner income.

Track overhead as % of revenue.

Separate direct job cost from burden.

Budget lift rentals by project.

Review staffing before hiring.

Price work to cover support hours.

Watch for thin-margin work that looks busy but leaves no cash after overhead. If billing slows or change orders slip, fixed costs still land on the business, so the owner pays the price first.

Field Labor Productivity

Field Labor Productivity

Field labor productivity is the share of paid crew time that turns into installed work, and it sits inside direct labor cost of goods sold (COGS). In this model, Year 1 labor allowance is $1,500 per curtain wall system, $200 per commercial window unit, $1,200 per structural glass wall, $500 per skylight assembly, and $400 per storefront system. If rework, overtime, site delays, poor access, or weak supervision push actual labor above those amounts, gross margin and owner pay drop fast.

Here’s the quick math: a 10% labor overrun adds $150 per curtain wall system, $20 per window unit, $120 per structural glass wall, $50 per skylight assembly, and $40 per storefront system. The key input is labor variance versus the unit allowance. What this estimate hides is stacking losses across multiple crews and days, so small misses can drain cash before taxes and reserves.

Track Labor by Unit Type

Measure labor by system type, not just by project. Track installed units, crew hours, overtime hours, rework hours, and delay time against the $1,500, $200, $1,200, $500, and $400 allowances. If access is blocked or drawings are late, stop the crew or change the schedule instead of paying for idle time.

Budget hours per unit type

Log rework the same day

Price delay claims fast

Review foreman variance weekly

Use one rule for owner income: if a crew needs overtime twice on the same scope, the plan, site readiness, or supervision is off. The fix is tighter daily production targets and faster change orders, because every labor overrun cuts gross profit before the owner can draw cash.

Backlog And GC Relationships

Profitable Backlog and GC Relationships

Backlog is signed work left to build. For a commercial glazing contractor, income depends less on being busy and more on having a profitable backlog with repeat general contractor (GC) work. When the book includes 120 curtain wall systems, 800 commercial window units, 40 structural glass walls, 60 skylight assemblies, and 150 storefront systems, steady GC relationships help smooth revenue timing and make owner pay more predictable.

What matters is quality, not just volume. A full backlog with weak terms, poor site readiness, or high closeout risk can still trap cash and force unpaid rework. Clean GC relationships also cut bid waste and usually improve change order discipline, so more of each contract turns into gross profit instead of free extras.

Track the backlog before you count it

Score every job on margin, payment terms, site readiness, and closeout risk. If a GC pays slowly, changes scope often, or can’t release the site, that backlog is not really strong. It may look busy, but it can still delay cash and shrink the owner’s draw.

Rank jobs before signing.

Favor repeat GC accounts.

Document change orders fast.

Drop thin, slow-pay work.

Keep a live backlog by start date and bill date. That lets you forecast crew load, progress billing, and cash needs, so you can tell when the book is healthy and when it only looks full.