How Much Cross-Border Transportation Owners Can Make From $9326K

A cross-border transportation business owner can make money only after trip costs, platform costs, overhead, debt, and reserves are covered Using the researched first year assumptions, revenue is about $9326k, listed variable costs are 130%, fixed overhead is $972k, and marketing is $2500k That leaves about $4642k before owner pay, payroll, debt, taxes, and reserves In the high case using Year 5 assumptions, revenue reaches $312M, but actual owner take-home still depends on fleet size, drivers, reinvestment, and cash retained in the business

Owner income$4.6MNet margin-30% to -10%Revenue for target pay$9.3MBusiness difficultyHard

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want the six income drivers?

1

Lane Pricing

$80-$1.2K

Orders range from $80 to $1.2K, so mix and lane price drive the biggest swing in owner profit.

2

Vehicle Utilization

0.5x-6.0x

More loaded miles per vehicle spread fixed overhead and lift cash without much extra headcount.

3

Backhaul Rate

130%-110%

Backhaul, or the return leg, cuts empty miles and keeps more margin on each trip.

4

Border Efficiency

Month 18

Faster customs and handoffs keep vehicles moving and help the business reach breakeven sooner.

5

Direct Costs

130%-110%

A lower variable cost load drops straight into EBITDA, so small savings matter.

6

Compliance Burden

$2.4K/mo

Legal, insurance, and licensing sit in fixed overhead, so a lighter burden trims the monthly burn.

Want to see the income model for Cross-Border Transportation?

How much can you make with one cross-border transportation vehicle?

One-vehicle income for Cross-Border Transportation can’t be proven from the model because active vehicles, trips, fuel, driver pay, tolls, and maintenance aren’t provided; the cited $9,326k is first-year total business revenue, not one-vehicle revenue, as covered alongside What Is The Current Growth Trend Of Cross-Border Transportation?. Per-vehicle revenue = total revenue ÷ active vehicles, and if one vehicle had to absorb $972k fixed overhead plus $2,500k marketing, utilization must be strong before safe owner pay.

Use This Formula

Start with $9,326k total revenue

Divide by active vehicle count

Subtract fuel, tolls, maintenance

Subtract driver pay, unless owner-operated

Watch The Risk

Vehicle count is not provided

Trips per week are not provided

Fixed overhead totals $972k

Marketing adds $2,500k

How much revenue does a cross-border transportation business need to pay the owner?

For Cross-Border Transportation, the owner needs about $3.991M in Year 1 revenue to cover fixed overhead, marketing, and a target owner pay, before payroll, debt, taxes, and reserves. Here’s the quick math: $3.472M in fixed overhead plus marketing, divided by the stated contribution margin, gets you to the break-even base, and owner pay pushes it higher. Separate accounting profit from cash, because you still need money for claims, repairs, permits, insurance, and working capital.

Revenue floor

$3.472M fixed overhead + marketing

~$3.991M with owner pay

Before payroll, debt, taxes

Before reserves and cash buffer

Cash planning

Keep cash separate from profit

Reserve for claims and repairs

Reserve for permits and insurance

Reserve for working capital

Is a cross-border transportation business more profitable as an owner-operator or fleet owner?

For Cross-Border Transportation, the owner-operator model usually looks better early because one person can cover driving, dispatch, and customer work without adding payroll. A fleet owner can grow revenue faster, but profit only improves if extra vehicles stay loaded, border delays stay controlled, and reserves are funded before distributions. On acquisition, scale can help too: seller CAC falls from $500 to $350, and buyer CAC drops from $75 to $45.

Owner-operator edge

One person covers more functions

Fewer payroll costs at launch

Lower fixed cost pressure

Cash stays simpler to manage

Fleet profit test

Added trucks must stay loaded

Insurance and repairs rise fast

Compliance work adds overhead

Debt risk can squeeze cash

Scaling helps Cross-Border Transportation only if the new volume lowers CAC and the operation keeps enough cash on hand. If border delays or empty miles rise, the fleet can grow revenue and still lose profit.

Key Takeaways

Lane choice depends on customer type and repeat demand.

Underused vehicles quickly erode margin under high overhead.

Backhaul and customs delays directly lift or cut take-home.

Variable costs must stay below revenue to pay owners.

Compare lean, base, and high owner-income scenarios using sourced assumptions

Owner income scenarios

Owner income moves with seller and buyer volume, ad spend, and the cost load on each shipment. The lean, base, and high cases show how much cash is left before owner pay.

Compare lean, base, and high cash before owner pay.

Scenario

Lean CaseEarly ramp-up

Base CaseScaled marketplace

High CaseMature year

Launch model

This is the lower-earnings path with early volume and heavy launch spend.

This is the modeled middle path with stronger volume and better cost absorption.

This is the stronger-earnings path with mature volume and tighter listed cost load.

Typical setup

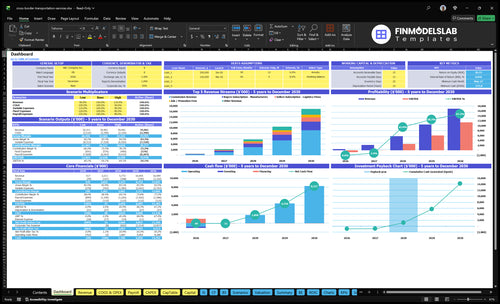

Year 1 uses 200 sellers and 2,000 buyers, with $9,326k revenue, 130% listed variable costs, $2.5M marketing, and $972k fixed overhead before owner pay.

Year 3 uses 1,000 sellers and 12,727 buyers, with $1,049M revenue, 118% listed variable costs, $11M marketing, and $972k fixed overhead before owner pay.

Year 5 uses 2,000 sellers and 28,889 buyers, with $3,123M revenue, 110% listed variable costs, $20M marketing, and $972k fixed overhead before owner pay.

Cost drivers

Seller volume

buyer volume

130% variable costs

$2.5M marketing

$972k fixed overhead

Seller volume

buyer volume

118% variable costs

$11M marketing

$972k fixed overhead

Seller volume

buyer volume

110% variable costs

$20M marketing

$972k fixed overhead

Owner income rangeBefore owner reserves

$4.6MLean cash

$805MBase cash

$2.57BHigh cash

Best fit

Use this to stress-test launch risk and slow ramp-up.

Use this as the main operating plan for a scaled marketplace.

Use this to test upside if the platform reaches mature scale.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Cross-Border Transportation Core Six Income Drivers

Lane Mix And Pricing Power

Lane mix and pricing power

Lane mix decides whether the platform earns fast, repeat commission or slow, one-off volume. In Year 1, sourced AOV can be about $80 for individuals; by Year 5, manufacturers can reach $1,200. Higher AOV lifts commission dollars, but manufacturers repeat less often than e-commerce retailers, so revenue quality can fall if the lane is too sparse.

No one lane is best. US-Mexico, US-Canada, regional, long-haul, freight, and passenger lanes each change price, trip length, and border complexity, which shifts gross profit and cash before owner pay. A lane with strong pricing power can fund growth sooner, but weak repeat demand leaves fixed costs to the owner.

Price by lane, not by hope

Track AOV, repeat orders, border complexity, and margin by lane and customer type. The quick test is simple: if a lane brings bigger orders but fewer repeats, it still may lose to a lower-AOV lane with steady reorder flow.

Segment by customer type

Compare AOV and repeat rate

Test commissions by lane

Watch cash before owner pay

Use the lane that covers fixed costs fastest. If pricing power rises but repeat demand drops, commission revenue can look good on paper while take-home income stays thin.

Border Delays And Customs Efficiency

Border Delays And Customs Efficiency

Border delays hit owner pay by cutting trips per week and pushing up driver time, fuel burn, and detention charges. The real cost is the lost contribution on each missed load, so the model should track average wait time, paperwork error rate, missed pickup windows, and trips lost per vehicle. The sourced data does not give a wait-time cost, so treat customs wait time cost as an editable input.

Here’s the quick math: if a vehicle sits at the border, the business loses the revenue from that trip and still carries some of the cost. That means profit drops twice, first from lower utilization and then from extra operating expense. Better documentation and dispatch keep the same fleet moving, so cash stays available for overhead and owner draw instead of getting stuck in delay time.

Track Delay Cost Per Trip

Measure delay cost as (trips lost × contribution per trip) plus detention, fuel, and driver overtime. Track it by lane and by carrier, because a lane with short transit time can still be weak if border processing is slow. If paperwork errors rise, the owner should expect lower margin and weaker cash flow, even when booked volume looks fine.

Average wait time by lane

Paperwork errors per shipment

Missed pickup windows each week

Trips lost per vehicle monthly

Test tighter document checks before adding vehicles. If dispatch and customs prep cut even one lost trip per week, utilization improves without new capital spend, and that lifts the cash left for owner pay.

Direct Operating Cost Control

Direct Operating Cost Control

Track direct operating cost per trip and per mile, not as one monthly lump. The sourced variable-cost ratio starts at 130% of revenue in Year 1, then eases to 122%, 118%, 114%, and 110% by Year 5. That means every $1.00 of sales still carries $1.10 to $1.30 of variable cost before fixed overhead and owner pay.

Include fuel, driver wages or contractor rates, tolls, maintenance, repairs, roadside downtime, and claims. If one lane runs hot on border time or repairs, it can wipe out cash that looked available for distributions. Revenue growth helps only after the cost ratio moves down.

Track Cost Per Lane

Build a lane sheet with revenue per load, cost per mile, and cost per trip. Split each cost line so you can see which lane is eating margin before owner pay. If a lane stays above 100% variable cost to revenue, reprice it, cut empty miles, or stop taking it.

Watch the inputs that move fastest: miles, border delay, fuel burn, labor rate, and claim frequency.

Trips by lane

Cost per mile

Downtime hours

Claims per month

Backhaul And Empty Miles

Backhaul And Empty Miles

Backhaul revenue is paid work on the return leg. It matters because the same vehicle, driver time, insurance, and permits can support more revenue per round trip, so gross margin improves when the truck is not running empty. If the model assumes weak return loads, owner take-home falls even when outbound pricing looks strong.

This driver depends on backhaul rate, empty-mile share, loaded trip count, and revenue per vehicle. The model does not provide a backhaul rate, so it has to be an editable assumption. Here’s the quick math: higher return-leg pay raises revenue per round trip and lowers empty-mile drag; lower return-leg pay does the opposite.

Track Return Loads, Not Just Outbound Price

Measure backhaul revenue per trip, empty miles, and revenue per vehicle each month. Also track how often a vehicle returns with no paid load, because that is where margin leaks out. If return loads weaken, cash for owner pay drops fast even before fixed overhead and operating costs are fully visible.

Test scenarios with a higher and lower backhaul assumption before you set owner draw. Use inputs like loaded miles, return miles, trip volume, and pay per return leg. If backhaul improves, you can spread the same trip cost over more revenue; if it slips, reduce draw plans early so profit does not get squeezed later.

Track paid return miles monthly.

Compare empty miles by lane.

Model backhaul as editable input.

Fleet Utilization And Trip Volume

Fleet Utilization

Fleet utilization is the share of active vehicle time that turns into paid, loaded trips. More loaded trips per vehicle spread fixed overhead and lift cash before owner pay. The model assumes repeat orders rise from 400 to 600 for e-commerce retailers, 200 to 350 for manufacturers, and 50 to 80 for individuals, so underused vehicles leave too much cost on each trip.

Track Trip Density

Measure loaded trips per active vehicle, border wait time, maintenance days, driver hours, and dispatch gaps. Those inputs set real utilization. If downtime rises, you need more vehicles just to hold the same trip count, and $972k of fixed overhead and marketing spend can absorb margin fast. One clean test: compare cash per active vehicle before and after cutting idle time.

Track loaded trips weekly.

Split downtime by cause.

Log border wait minutes.

Watch repeat orders by segment.

Fill dispatch gaps same day.

Use segment-level repeat order forecasts first, then layer in downtime and driver-hour limits. That gives a better read on revenue per vehicle and owner draw. If active vehicles stay underused, fixed costs stay flat while cash available to the owner drops.

Compliance, Permits, And Insurance Burden

Permits, Insurance, And Compliance Cost

Cross-border permits, licensing, insurance, and filings push up the monthly break-even point before the owner sees any draw. With $81k per month in fixed overhead, including $20k for legal and accounting retainers, the business must clear that base load first. Every added compliance dollar raises the revenue needed to pay the owner.

This burden changes cash flow fast because delays, missing documents, or local rule gaps can stop shipments and still leave the fixed bill due. Here’s the quick math: if compliance or insurance costs rise by $5k a month, break-even rises by $5k a month too. Regulatory filings, commercial insurance, licensing, documentation, and safety rules should be verified locally; this is planning input, not legal advice.

Track Compliance Cost Per Lane

Measure compliance by lane, country, and shipment type so you can see which routes protect margin and which ones eat owner pay. Track policy premiums, permit fees, filing time, document rework, and any shipment holds. The key test is simple: does each lane still cover its share of $81k monthly fixed overhead after compliance costs?

Build a monthly checklist for renewals, filings, and insurance limits, then tie it to forecasted shipment volume. If a lane needs extra filings or higher coverage, price it up or reduce exposure. Owner income improves when compliance cost stays predictable, not when it surprises you after the freight is booked.