Factors Influencing Dim Sum Restaurant Owners’ Income

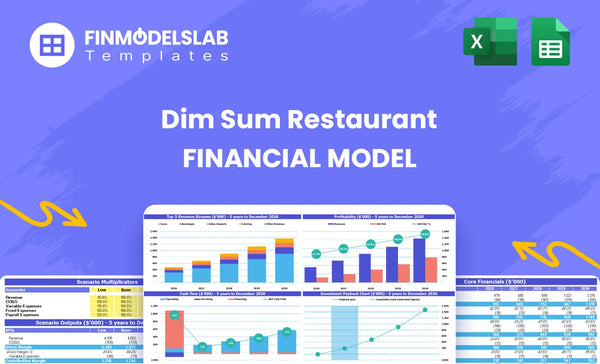

Dim Sum Restaurant owners achieve high margins by controlling Food & Beverage costs (starting at 100% of sales) and maximizing weekend AOV, which is $2500 in 2026 compared to $1800 mid-week The business reaches break-even in 3 months This analysis provides concrete scenarios, benchmarks, and actionable insights to help founders maximize their return on equity (ROE) of 58% and manage the $140,400 annual fixed overhead

7 Factors That Influence Dim Sum Restaurant Owner’s Income

#

Factor Name

Factor Type

Impact on Owner Income

1

Sales Volume and Price Mix

Revenue

Income scales directly by boosting daily covers (158 in Y1) and maximizing the high weekend AOV ($2500).

2

COGS Efficiency

Cost

Every percentage point saved on COGS (dropping from 125% to 97% by Y5) flows straight to EBITDA.

3

Labor Management and Scaling

Cost

Income rises by optimizing staff Full-Time Equivalents (FTEs) against covers, managing the Assistant Manager count from 05 in Y2 to 10 in Y3.

4

Fixed Overhead Control

Cost

Maximizing sales volume dilutes fixed costs of $140,400 annually, especially the $7,500 monthly rent.

5

Sales Channel Contribution

Revenue

Owner income improves by shifting sales away from high-fee Online Orders (150% in Y1) to direct channels.

6

Capital Expenditure and Depreciation

Capital

Lower debt service and minimal maintenance expenses boost net income after the initial $328,000 CAPEX spend.

7

Growth Rate and Margin Improvement

Risk

Income jumps as covers grow from 1,110 to 2,510 weekly by Y5 while margins improve, which defintely leads to $194M EBITDA.

Dim Sum Restaurant Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

What is the realistic owner income potential and growth trajectory?

The projected growth for the Dim Sum Restaurant concept, hitting $194 million EBITDA by Year 5, is aggressive when measured against the $328,000 CAPEX and the required 11% IRR hurdle.

Growth and Investment Check

Hitting $194 million in EBITDA by Year 5 from a $386,000 starting point requires aggressive scaling, and you need to know if your unit economics support that leap; if you're worried about hitting those targets, review how Are Your Operational Costs For Dim Sum Restaurant Staying Within Budget? to ensure efficiency scales with volume.

The required investment is a $328,000 Capital Expenditure (CAPEX), which must generate returns justifying an 11% IRR (Internal Rate of Return, or the expected profit rate).

Verify the path from $386k Y1 EBITDA to the $194M Y5 target.

Confirm the $328k CAPEX covers necessary scaling tech and build-out.

Model the payback period on the initial outlay to confirm the 11% IRR target is achievable.

Owner Compensation Benchmarks

Owner income potential hinges on how much profit you extract versus reinvesting for that massive growth.

You must benchmark your proposed salary plus distributions against what similar-sized restaurant group executives earn in the market.

If the concept hits its targets, the owner's take should reflect a significant percentage of the Year 5 EBITDA, not just a standard CEO salary.

Establish a clear salary band for a restaurant CEO managing this scale of operation.

Define distribution triggers based on clear EBITDA milestones, not just annual guesswork.

How quickly can the business reach profitability and stabilize cash flow?

The Dim Sum Restaurant aims to hit break-even within three months, targeting March 2026, but stabilizing cash flow demands a substantial initial capital buffer of $718,000 before that point. Have You Considered The Best Location To Open Your Dim Sum Restaurant?

Three-Month Stabilization Goal

The operational plan targets reaching monthly profitability by March 2026.

This aggressive timeline assumes immediate traction and efficient cost control post-launch.

Founders must secure at least $718,000 in minimum cash reserves to cover initial ramp-up losses.

This cash buffer bridges the gap until sustained positive operating cash flow arrives.

Cover Volume to Beat Fixed Costs

Monthly fixed overhead stands at $11,700, which must be covered every month.

The primary operational lever is increasing daily customer volume (covers).

You need to calculate the exact daily cover count required to generate $11,700 in gross profit.

If margins are tight, you'll defintely need higher average checks to hit this target quickly.

Which operational levers offer the highest return on effort (ROE)?

For the Dim Sum Restaurant, controlling input costs yields the fastest return on effort, as reducing F&B expenses directly improves gross margin faster than chasing volume shifts or managing fixed labor upfront; for context on initial outlay, review How Much Does It Cost To Open, Start, Launch Your Dim Sum Restaurant?. Labor is a fixed anchor at $350,000 in Year 1, so any revenue growth must significantly outpace that cost base just to maintain current margins. The F&B cost reduction target—moving from 100% down to 80% by Year 5—is a powerful lever because it directly flows to the bottom line, assuming stable pricing.

Cost Control Levers

Labor fixed cost is $350,000 in Year 1.

F&B cost reduction goal: 100% down to 80% by Year 5.

Revenue growth must cover the fixed labor baseline first.

Revenue Mix Trade-Offs

Weekend AOV target sits at $2,500.

Weekday strategy needs consistent volume daily.

High weekend AOV rewards successful large party bookings.

Volume builds coverage for that fixed $350k labor cost.

The trade-off between maximizing high-value weekend transactions and building consistent weekday traffic requires careful modeling. A weekend AOV of $2,500 is substantial, suggesting a focus on large party bookings or high-ticket beverage sales during those peak times. Still, relying solely on these spikes ignores the need for steady daily volume to absorb that fixed $350,000 labor cost throughout the week; you defintely need weekday traffic.

What is the total capital commitment and associated risk?

The total capital commitment for launching this Dim Sum Restaurant is substantial, requiring $328,000 in CAPEX plus necessary working capital, but the high projected 58% Return on Equity (ROE) suggests a rapid recovery of that outlay within 14 months. Understanding how quickly you recoup that initial spend is crucial, which ties directly back to What Is The Most Critical Metric To Measure The Success Of Dim Sum Restaurant?

Initial Capital Structure

Total initial investment starts with $328,000 in Capital Expenditures (CAPEX) for build-out and kitchen equipment.

You must budget for working capital to cover at least three months of overhead until consistent sales volume stabilizes.

The primary operational risk is the deployment of this large upfront cash sum before securing reliable, high-margin sales volume.

If the permitting process drags past 90 days, that delays revenue generation and increases the required working capital buffer.

Payback and Profitability Levers

The model projects an aggressive Return on Equity (ROE) of 58%, showing strong potential return on owner capital.

The payback period to recover the entire initial outlay is estimated at only 14 months.

To hit that 14-month target, daily customer covers must meet projections consistently from the first month.

If the average order value (AOV) drops below projections, the payback timeline extends defintely.

Dim Sum Restaurant Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Key Takeaways

Dim Sum restaurant owners project substantial annual EBITDA growth, starting at $386,000 in Year 1 and potentially exceeding $19 million by Year 5 through successful scaling.

Profitability is achievable quickly, with the business model projecting a break-even point within just three months, provided the minimum operational cash reserve of $718,000 is secured.

Maximizing owner income heavily relies on aggressive Cost of Goods Sold (COGS) efficiency, targeting a reduction from 125% initially down to 97% by Year 5 to directly boost the bottom line.

The initial investment requires $328,000 in CAPEX and working capital, which generates a strong Return on Equity (ROE) of 58% with a payback period of 14 months.

Factor 1

: Sales Volume and Price Mix

Volume and Value Link

Owner income growth hinges on hitting the Year 1 target of 158 average daily covers. You must also protect the high $2,500 weekend Average Order Value (AOV). This pricing and volume mix drives the projected $127 million revenue in Year 1. It's all about density and high-value transactions.

Volume Drivers

Hitting 158 daily covers requires knowing your weekday versus weekend split precisely. If weekends drive the premium $2,500 AOV, you need to track covers per day segment carefully. The total Year 1 revenue projection of $127 million assumes this exact volume and pricing structure holds steady.

Target 158 covers daily.

Protect $2,500 weekend AOV.

Track weekday/weekend split.

Mix Optimization

To maximize owner income, focus on shifting volume to high-yield periods. If weekday covers are lower, use targeted specials to lift that AOV slightly. You can't afford to lose those high weekend transactions; they carry the whole model. Defintely focus marketing spend there.

Lift weekday AOV slightly.

Prioritize weekend marketing spend.

Avoid discounting weekend slots.

Revenue Leverage

Revenue is the base for covering your $140,400 annual fixed overhead. Every cover above 158 reduces the burden of that rent and utilities cost. High sales volume directly dilutes fixed costs, improving overall operating leverage quickly.

Factor 2

: Cost of Goods Sold (COGS) Efficiency

COGS Impact

Your gross margin hinges entirely on controlling ingredient and packaging costs. Moving COGS from 125% in Year 1 down to 97% by Year 5 is the single biggest lever for profitability. Every point saved directly boosts your final EBITDA result.

What COGS Covers

Cost of Goods Sold covers direct costs for the artisanal Dim Sum and beverages sold. You need precise tracking of raw food inventory costs, packaging expenses, and waste rates. This metric directly impacts the gross profit margin before labor and overhead hit.

Track ingredient purchase prices daily.

Calculate waste percentage per batch.

Monitor packaging unit cost.

Cutting Ingredient Costs

Reducing COGS requires discipline in sourcing and kitchen execution. Since volume grows from 1,110 to 2,510 weekly covers by Year 5, leverage that scale for better supplier terms. Watch out for quality drift when cutting costs, though.

Negotiate bulk pricing early.

Standardize portion control strictly.

Review high-cost specialty ingredients.

The EBITDA Link

The projected margin improvement is huge: going from 125% COGS down to 97% is key to hitting the $194M EBITDA target in Year 5. This defintely shows that operational excellence in the kitchen directly translates to owner wealth creation.

Factor 3

: Labor Management and Scaling

Labor Cost Control

Wages cost $350k in Year 1, making labor a primary expense driver. To boost owner income as volume increases, you must tightly manage Full-Time Equivalents (FTEs) against daily covers. Scaling management correctly, like moving Assistant Manager FTE from 0.5 in Y2 to 1.0 in Y3, directly impacts profitability.

Staffing Cost Inputs

The initial $350,000 wage expense covers all operational staff needed to handle projected volume. Estimating this requires knowing the required staff-to-cover ratio for peak and off-peak times, plus projected annual salary rates for each role, including the Assistant Manager. You need precise headcount planning.

Staffing ratio per cover

Annual salary rates per FTE

Projected weekly covers

Managing FTE Growth

Optimize labor by linking staffing levels directly to projected covers, not fixed schedules; overstaffing early kills cash flow. If onboarding takes 14+ days, churn risk rises, slowing your ability to adjust staffing levels quickly. You must defintely match labor spend to revenue reality.

Avoid scheduling based on desire

Monitor staff utilization hourly

Adjust schedules weekly

Management Scaling Risk

Scaling management capacity is key; the planned increase in Assistant Manager FTE from 0.5 in Y2 to 1.0 in Y3 must align with cover growth. If volume doesn't support that second manager hire, you add fixed payroll unnecessarily, hurting margins before you hit target volume.

Factor 4

: Fixed Overhead Control

Fixed Cost Anchor

Your fixed overhead totals $140,400 annually, or $11,700 per month. Since rent alone eats up $7,500 monthly, owner income only improves when you aggressively push sales volume to dilute these non-negotiable costs. That fixed base is high.

Overhead Components

Fixed costs cover non-negotiable expenses like the $7,500 monthly rent for the physical location and associated operating costs. You estimate these at $140,400 annually, regardless of how many Dim Sum baskets you sell. This number is the baseline cost of keeping the doors open every day.

Rent: $7,500/month.

Total Fixed: $11,700/month.

Diluting the Base

You can't easily cut the $7,500 rent, so focus on dilution. If monthly revenue needs to cover $11,700 in overhead plus variable costs, increasing covers spreads that $11,700 thinner across more transactions. Avoid signing long leases with steep early escalators, which is a common mistake.

Boost daily covers fast.

Maximize weekend AOV.

Volume is the Lever

Getting to $127 million in Y1 revenue is the direct countermeasure to this overhead pressure. Every dollar above the break-even point, driven by higher sales volume, directly fattens owner income because the $11,700 monthly anchor doesn't move. That’s how you make the fixed cost structure work for you.

Factor 5

: Sales Channel Contribution

Shift Sales Mix Now

Owner income improves significantly by moving volume away from high-fee online orders toward direct sales channels. Reducing platform fees from 15% in Year 1 down to 7% by Year 5 directly boosts your retained earnings. That’s pure margin gain.

Platform Fee Cost

Platform fees are the commission paid to third-party sellers for orders they process, hitting your gross profit hard. In Year 1, these fees are set at 15% of online revenue. You calculate this cost by multiplying your projected online sales volume by this fee rate. This expense must be managed closely.

Online Sales Volume forecast

Fee Rate (15% in Y1)

Total Fee Expense calculation

Driving Direct Sales

To maximize owner income, you must actively reduce reliance on high-cost channels, even if online orders are 150% of volume initially. Focus on building direct customer relationships that bypass third-party commissions entirely. The goal is reaching the 7% fee rate benchmark by Year 5. Don't let convenience kill your margins.

Create direct ordering incentives

Track online vs. direct split daily

Target 7% fee rate by Y5

The Margin Difference

Since online sales dominate early volume at 150% in Year 1, the immediate action is steering customers toward direct ordering. Shifting just one dollar from the 15% fee bucket to a direct transaction saves you 8 cents in immediate profit. This optimization is key before scaling labor costs.

Factor 6

: Capital Expenditure and Depreciation

CAPEX Sets Owner Cash Flow

The initial $328,000 capital outlay sets the depreciation schedule, which directly impacts taxable income. Because this investment covers necessary build-out, focusing on lean maintenance and manageable debt service ensures more cash flow remains as net owner income. That initial spend is your foundation for profitability.

Initial Spend Breakdown

This $328,000 CAPEX covers three main buckets: the commercial kitchen build-out, necessary furnishings for the modern dining area, and leasehold improvements to the physical space. To estimate this accurately, you need firm quotes for equipment installation and contractor bids for the tenant improvements. This is the upfront cost before opening day.

Kitchen equipment installation

Dining room furnishings

Leasehold improvements quotes

Controlling Ongoing Costs

You can’t cut the initial build-out, but you control the depreciation method and ongoing upkeep. Choose a shorter depreciation schedule to accelerate tax deductions, though it may increase reported expenses initially. Keep maintenance costs low by specifying durable, commercial-grade fixtures from the start. If maintenance runs high, owner income suffers defintely.

Select durable, commercial-grade assets

Review tax depreciation schedules

Budget for low post-opening repairs

Depreciation vs. Debt Service

Depreciation is a non-cash expense that lowers taxable income, which is good. However, high debt service payments on financing used for that $328k spend eat real cash flow. The goal is to structure financing so that the depreciation shield outweighs the debt drain, maximizing the cash flow available to the owner.

Factor 7

: Growth Rate and Margin Improvement

Volume Drives Profitability

Volume growth combined with sharp COGS reduction is the primary driver of owner wealth creation. As weekly covers scale from 1,110 to 2,510 by Year 5, efficiency gains slash Cost of Goods Sold (COGS) from 125% down to 97%. This operational leverage results in a projected $194M EBITDA in Year 5.

COGS Input Scaling

COGS efficiency hinges on managing raw material purchasing and waste as volume explodes. The model assumes COGS starts at an unsustainable 125% of revenue in Year 1, requiring immediate intervention. To hit the 97% target by Year 5, you must secure better supplier pricing or drastically reduce spoilage once you pass 2,000 weekly covers. That initial 125% is defintely not sustainable.

Volume Lever Impact

Owner income accelerates sharply because fixed costs get absorbed faster while contribution margins improve. Weekly volume must climb from 1,110 to 2,510 covers to dilute the $140,400 annual overhead. The 28 percentage point drop in COGS (125% down to 97%) is the real profit multiplier here, so keep pushing covers.

Volume growth absorbs fixed overhead.

COGS reduction boosts unit economics.

Year 5 EBITDA reaches $194M.

Margin Floor Check

Focus relentlessly on procurement contracts to lock in lower food costs early. If COGS stabilization stalls above 105%, the projected $194M EBITDA target becomes unachievable, regardless of hitting 2,510 weekly covers. This margin floor is non-negotiable for owner success.

Based on projections, owners can expect EBITDA of $386,000 in the first year, rising rapidly to $1,083,000 by Year 3 This income depends heavily on achieving the projected 1,110 weekly covers and maintaining low 125% COGS

This model projects a quick 3-month timeline to break-even (March 2026) The business requires a minimum cash investment of $718,000 to cover initial CAPEX ($328,000) and working capital during the ramp-up phase

Choosing a selection results in a full page refresh.