Direct Primary Care Practice Owner Income: $220K Plus EBITDA

You’re estimating owner take-home from a US direct primary care practice, not treating revenue as salary This model covers a five-year membership ramp, with $987,000 Year 1 revenue, $220,000 physician payroll, Month 7 breakeven, reserves, reinvestment, and exclusions for personal taxes, debt structure, and individual compensation advice

Owner income$220K baseNet margin0% to 60.1%Revenue for target pay$987KBusiness difficultyHard

Want to test your DPC owner income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margins, payroll, taxes, reserves, and timing. It is not guaranteed salary, tax advice, or owner distribution advice. The model also shows Month 7 breakeven and about 552000 in minimum cash need.

Want to pressure-test the full Direct Primary Care Practice forecast?

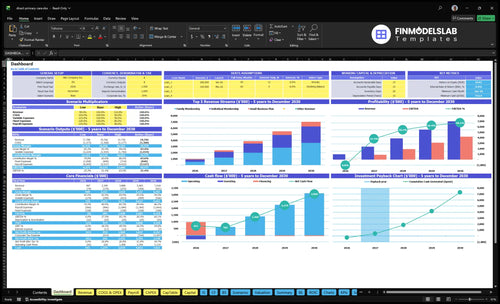

The Direct Primary Care Practice Financial Model Template adds dashboard, assumptions, income statement, cash flow, break-even, payback, and scenario tabs. It tests member ramp, pricing tiers, physician FTE growth, payroll from $490K to $128M, revenue from $987K to $7,018M, EBITDA from $0 to $4,219M, and minimum cash of $552K. Open the model.

Owner pay planning checks

Owner take-home planning

Revenue and margin

Scenario stress tests

How many patients does a direct primary care doctor need?

A Direct Primary Care Practice needs about 706 average active paying members in Year 1, based on $987K revenue ÷ ($116.50 monthly fee × 12); track paying members, not inquiries, and pair this with What Five KPIs Should Direct Primary Care Practice Track?. By Year 5, $7.018M revenue ÷ ($173.30 × 12) implies about 3,375 average memberships; if that is spread across 30 physician FTE, the math is 113 members per physician, not 1,125.

Panel math

706 Year 1 average members

$116.50 weighted monthly fee

$987K Year 1 revenue

Month 7 breakeven depends on ramp

Capacity checks

3,375 Year 5 average memberships

$173.30 Year 5 monthly fee

30 physician FTE capacity base

Churn and access quality cap panels

Can direct primary care replace a physician salary?

Yes—if you're asking whether a Direct Primary Care Practice can pay a physician a $220K annual salary from day one, the model says yes. But Year 1 EBITDA is $0 after payroll, so that cash is salary, not owner distributions. By Year 2, EBITDA reaches $897K, and by Year 5 it reaches $4.219M before taxes, debt service, reserves, and reinvestment; payback is 20 months, so cash planning has to come first.

Cash timing

Month 1 supports salary.

Year 1 EBITDA stays at $0.

Payback lands in 20 months.

Distributions wait for cash build.

Owner economics

$220K is the physician salary.

Year 2 EBITDA reaches $897K.

Year 5 EBITDA reaches $4.219M.

Taxes and reserves cut take-home cash.

What direct primary care operating costs reduce owner income most?

Payroll is the biggest squeeze on owner income in a Direct Primary Care Practice, and the ramp is brutal: it moves from $490K in Year 1 to $128M in Year 5. Even with strong gross margin, take-home stays tight because fixed overhead runs about $14K per month and variable costs start at 135% of revenue before easing to 95% by Year 5.

Biggest cost drains

Payroll is the main pressure point.

Fixed overhead stays around $14K/month.

Rent is $85K, with $25K malpractice.

Utilities add $12K, plus admin costs.

Why income stays tight

Variable costs start at 135% of revenue.

Supplies and telehealth/EHR drive early pressure.

Marketing rises from $120K to $300K.

High gross margin does not mean high take-home.

Direct Primary Care Practice Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six DPC income drivers?

1

Active Members

706-3,375

More enrolled members spread the same clinic base, so owner take-home scales faster than costs.

2

Membership Fee

$116-$173

A higher weighted fee raises cash per member and lifts margin without adding visits.

3

Physician Capacity

10-30 FTE

More physician FTE opens more patient slots, so growth keeps flowing before service slows.

4

Staff Mix

$490K-$1.28M

Payroll is the biggest controllable cost, so the right FTE mix protects take-home as the panel grows.

5

Fixed Overhead

$14K/mo

The $14K monthly overhead line sets break-even, and every extra member above it adds more cash.

6

Enrollment Efficiency

$85->$60

Lower CAC means each new member costs less to win, which shortens payback and raises owner yield.

Direct Primary Care Practice Core Six Income Drivers

Active Paying Member Count

Active Paying Member Count

Each active paying member adds recurring cash, but it also adds visit volume, messaging, and care follow-up. In the provided model, the Year 1 weighted monthly fee is $11,650, and contribution after 135% variable costs is about $10,078 per member per month. That makes member count the main driver of revenue and margin.

The scale effect is strong: the model says 100 extra active members add about $101K monthly contribution before payroll and fixed costs. By Year 5, contribution rises to about $15,684 per member per month, so retention matters more than sign-ups. If churn rises or physician capacity fills up, owner pay stops scaling cleanly.

Track member count, not just sign-ups

Measure active members, monthly churn, and members per physician together. Here’s the quick math: more members help only when retained members stay inside physician capacity and access stays strong. If same-day visits slip, churn can erase the extra contribution fast.

Active members by month

Monthly churn rate

Members per physician

Contribution per member

Use that scorecard to decide when to add staff or slow enrollment. Member growth improves owner take-home income only after payroll and fixed costs are covered. If the panel grows faster than care capacity, the business gets busier without giving the owner much more cash.

1

Average Monthly Membership Fee

Average Monthly Membership Fee

Average monthly membership fee is the price each active member pays every month, before any add-ons. Here’s the quick math: the weighted fee rises from $11,650 in Year 1 to $17,330 in Year 5, so revenue per member improves even if headcount stays flat. That lifts cash flow and owner draw, but only if members keep renewing.

Mix matters. Family memberships grow from 30% to 38%, individual plans fall from 45% to 35%, and small business plans move from 25% to 27%. Fee increases help margin only when retention and local value hold; if churn rises, the higher price can backfire.

Track Fee Mix, Not Just List Price

Track monthly fee by plan, active member count, and churn by cohort. Compare realized revenue per active member with the weighted target so you can see whether family plans or employer plans are lifting the average fee. If the average fee rises but renewals slip, take-home income usually falls.

Test price changes in small steps and watch renewals, referrals, and visit use. The key input is not one ideal price; it is the balance between higher monthly revenue and stable retention. Build the forecast around plan mix, because shifts toward families or small business accounts change monthly cash fast.

2

Physician Panel Capacity

Physician Panel Capacity

Physician panel capacity is the ceiling on active members each doctor can safely handle. In the model, physician FTE grows from 10 in Year 1 to 30 in Year 5, and active memberships rise from about 706 to about 3,375. More capacity lifts recurring revenue, but only if access stays fast enough to keep members paying.

Same-day access, longer visits, virtual care, and clinical scope set sustainable panel size. The model also states about 1,125 members per physician by Year 5, so that assumption should be tested against visit volume and retention. If panels get too full, wait times rise, churn can rise, and owner profit can fall even with more members.

Keep the panel tied to access

Track active members per physician FTE, same-day slot fill, telehealth share, visit length, and churn. These inputs show whether capacity is still supporting revenue or starting to hurt it. If a fuller panel lowers renewals, the extra membership revenue can disappear into rework, complaints, and lower take-home pay.

Members per physician FTE

Same-day access

Visit length

Telehealth mix

Churn rate

Clinical scope

Set a panel cap from service math, not from ambition. Test growth until next-day demand, message volume, or renewal rates start to soften. That is the point where income quality weakens, because each added member no longer produces clean margin and stable cash flow.

3

Clinical And Administrative Staffing

Clinical and Administrative Staffing

Staffing is the tradeoff between service quality and owner pay. In Year 1, payroll is $490K across physician, registered nurse, medical assistant, practice manager, and marketing/business development roles, so lean staffing helps margins during ramp. But under-staffing can slow enrollment and raise churn, which cuts recurring revenue and delays the owner’s take-home.

Track payroll against growth

Measure staffing with FTE, active members, churn, and owner workload. The model reaches $128M of payroll by Year 5 as physician, nurse, assistant, and admin FTE expand, so each hire needs to protect access, retention, and enrollment speed. If same-day access slips or the owner is still covering admin work, payroll is too thin for the service promise.

Track payroll per active member.

Watch wait time and churn.

Add staff only when demand supports it.

4

Fixed Overhead And Startup Costs

Fixed Overhead Pressure

$14K in monthly fixed overhead means the practice has to cover rent, malpractice, and admin costs before the owner sees pay. Here’s the quick math: at $987K in revenue, that is about $168K a year, or roughly 17% of sales. At the modeled Year 5 revenue level of $7.018M, the same overhead falls to about 2.4% of sales.

$250K of startup capex for systems, equipment, setup, security, website, and signage is launch cash, not monthly opex. It still affects owner income because it delays payback and can force the business to grow before it can safely pay distributions. If membership ramp is slow, fixed costs create break-even pressure fast.

Track Burn Against Signed Members

Separate one-time capex from monthly operating expense in the forecast. Track cash burn, meaning monthly cash outflow, plus the member count needed to cover the $14K fixed base before owner draw. If rent or malpractice changes, update break-even right away.

Watch fixed cost per active member.

Test ramp speed against cash runway.

Lock launch spend before opening day.

Reforecast when revenue mix changes.

Owner pay gets easier only when recurring revenue stays ahead of overhead. If the practice reaches scale fast, fixed costs shrink as a share of sales; if it doesn’t, every slow month pushes profit and take-home down.

5

Retention And Enrollment Efficiency

Retention and Enrollment Efficiency

In a membership clinic, income comes from active members who stay paid, not just sign-ups. Better retention keeps monthly cash predictable, and better enrollment efficiency lowers customer acquisition cost (CAC) from $85 in Year 1 to $60 in Year 5, so the same marketing dollar buys more members. If churn rises, revenue still slips and owner pay gets less stable.

Here’s the quick math: at $120K marketing spend and $85 CAC, you can acquire about 1,412 members; at $300K and $60 CAC, that rises to 5,000. That only turns into durable income if onboarding, employer contracts, referrals, and reputation keep those members active. Lifetime value can’t be measured well without churn data, and it isn’t provided.

Track churn before you scale ads

Measure new sign-ups, active members, churn rate, and CAC every month. Use a simple funnel: leads, consultations, paid members, then retained members at 30, 90, and 180 days. If CAC improves but retention weakens, the marketing budget buys short-lived revenue, not dependable cash flow.

Track retention by cohort month.

Split individual, family, employer plans.

Compare CAC to first-year gross margin.

Test onboarding touchpoints in week one.

Use referrals to lower paid CAC.

The owner wins when each acquired member stays long enough to cover acquisition cost and keep paying monthly. If onboarding takes 14+ days or access is slow, churn risk rises and marketing spend turns into temporary revenue instead of steady profit and draw.

6

Direct Primary Care Practice Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high DPC owner income scenarios

Owner income scenarios

Income shifts with enrollment speed, CAC, and membership mix. The model reaches Month 7 breakeven, needs a $552K cash floor, and builds EBITDA from $0 to $4,219K by Year 5.

Compare conservative, modeled, and upside owner income paths.

Scenario

Low CaseLow Case

Base CaseBase Case

High CaseHigh Case

Launch model

Owner income stays thin until enrollment improves and reserves stay high.

Owner income follows the modeled ramp and starts to open up after breakeven in Month 7.

Owner income improves faster when enrollment ramps early and more cash clears reserves.

Typical setup

Revenue ramps slower than planned, CAC stays above $85, the mix skews to lower-fee memberships, and cash stays locked to protect the $552K floor.

Revenue runs from $987K in Year 1 to $7,018K in Year 5, EBITDA moves from $0 to $4,219K, and the $552K cash floor limits early distributions.

The practice gets a stronger family and employer mix, CAC trends toward $60, provider capacity scales sooner, and more EBITDA becomes available for distributions.

Cost drivers

Slower enrollment

CAC above $85

lower-fee mix

higher reserves

delayed distributions

Modeled enrollment

Month 7 breakeven

EBITDA growth

$552K cash floor

20-month payback

Faster enrollment

CAC near $60

stronger family/employer mix

added provider capacity

earlier distributions

Owner income rangeBefore owner reserves

Minimal distribution poolLow Case

Modeled draw pathBase Case

Expanded distribution poolHigh Case

Best fit

Use this to test a slow start with tight cash and little owner payout.

Use this as the working case for owner pay and cash timing.

Use this to test upside if growth outpaces the base plan and capacity expands sooner.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or actual distributions.

In this model, an owner-physician can plan around a $220,000 physician payroll role, with distributions depending on profit and reserves EBITDA is $0 in Year 1, then $897,000 in Year 2 and $4219 million in Year 5 That profit pool is before personal taxes, debt service, and retained cash decisions

The researched model reaches breakeven in Month 7 and payback in 20 months Minimum cash need is $552,000 in Month 6, which means the early ramp still needs funding even with recurring membership revenue Year 1 revenue is $987,000, but EBITDA is modeled at $0 after operating costs

This model is built around membership revenue, not traditional insurance billing Prices include $99 individual, $199 family, and $49 small business monthly plans in Year 1 The economics depend on active paying members, pricing mix, operating costs, and retention, not claims reimbursement assumptions

The biggest drivers are active member count, fee mix, staffing, fixed overhead, physician capacity, and enrollment efficiency Year 1 payroll is $490,000, fixed overhead is $14,000 per month, and marketing is $120,000 Variable supplies and software costs equal 135% of revenue in Year 1, then decline to 95% by Year 5

Improve member density before adding heavy overhead In this model, CAC drops from $85 to $60 while weighted monthly fee rises from $11650 to $17330 Keep staffing matched to panel size, protect access quality, and reserve cash before taking distributions The practice needs enough runway to cover the Month 6 cash low point

About the author

Michael Porter

Entrepreneurship Researcher

Michael Porter is an entrepreneurship researcher at Financial Models Lab who helps founders opening a new small business turn big questions into clear planning steps. He focuses on expense and revenue planning for the first year, keeping attention on useful numbers and realistic expectations. His work gives business plan writers practical guidance without sugarcoating the challenges ahead.

Choosing a selection results in a full page refresh.