How Much Dry Cleaning Pickup Owners Make At $4950 AOV

Owner take-home is not the same as dry cleaning pickup and delivery revenue it comes after cleaner payouts, route costs, software, marketing, reserves, and taxes In the provided first-year assumptions, the model uses a $4950 weighted average order value, a 15% variable commission plus $2 per order, and $120,000 buyer marketing at $45 CAC These ranges are planning assumptions, not guaranteed earnings, tax advice, or fixed owner distributions

Owner income-$42kNet margin-192%Revenue for target pay$1.83MBusiness difficultyHard

Want to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

How do you check owner income in one forecast view?

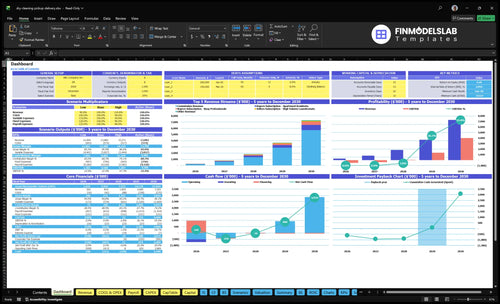

This Dry Cleaning Pickup and Delivery Service Financial Model Template shows owner income, revenue, costs, reserves, and scenarios in one view. It tracks active buyers, orders, AOV, gross margin, operating profit, cash reserve, and owner draw, with Year 1 to Year 5 inputs from $4,950 to $5,700 AOV, 15% to 18% commission, $45 to $25 CAC, and $120,000 to $850,000 marketing. Use it for planning support, not the main promise.

Owner-income model highlights

Owner draw and reserves

Revenue and margin charts

Scenario tests by year

How do you scale a dry cleaning pickup and delivery service?

Scale the Dry Cleaning Pickup and Delivery Service by staying owner-operated at first, using tight pickup windows and a small cleaner partner base, then adding drivers and dispatch only after repeat orders, route density, and support can handle more volume. Buyer marketing can rise from $120,000 in Year 1 to $850,000 in Year 5, while CAC falls from $45 to $25; that only works if orders repeat and routes stay full. Seller mix also shifts toward scale, with high-volume laundromats rising from 50% to 60% and boutique dry cleaners falling from 40% to 20%. Adding drivers, dispatch, claims handling, and working capital can grow revenue, but owner take-home may drop until density catches up.

Start lean

Use owner-operated routes first

Keep pickup windows tight

Work with a small cleaner base

Fill repeat orders before hiring

Scale with care

Lift marketing from $120k to $850k

Watch CAC fall from $45 to $25

Shift sellers toward laundromats

Expect slower take-home at first

Can you make money with a dry cleaning pickup and delivery service?

Yes, a Dry Cleaning Pickup and Delivery Service can make money if repeat orders and tight routes cover cleaner costs, delivery labor, marketing, software, and reserves; track the core numbers in What Are The 5 KPIs For Dry Cleaning Pickup And Delivery Service?. Year 1 unit math shows $49.50 weighted AOV, 2.44 orders per buyer per month, $9.43 commission revenue per order, and $11.99 weighted buyer subscription revenue.

What drives profit

Cluster pickups by building or zip code

Keep buyers ordering 2.44 times monthly

Protect $9.43 commission per order

Add subscriptions without raising churn

What cuts margin

Paid drivers reduce owner take-home

Dispatch adds daily management work

Insurance raises delivery overhead

Quality misses trigger refunds and churn

How much revenue does a dry cleaning pickup and delivery service need?

A Dry Cleaning Pickup and Delivery Service needs enough monthly revenue to cover gross margin, route costs, fixed overhead, reserves, taxes, and owner pay. In Year 1, the buyer-side math points to about $3,499 per active customer per month before churn and overhead, and the acquisition plan implies about 2,667 buyers from $120,000 at $45 CAC plus 30 partners from $15,000 at $500 CAC.

Revenue target

$3,499 per active buyer monthly

244 orders in the Year 1 math

Commission plus subscription revenue

Back out route cost, overhead, reserves, taxes

Acquisition plan

2,667 buyers from $120,000

$45 CAC per buyer

30 partners from $15,000

$500 CAC per partner

Want the six drivers that decide owner income?

1

Order Volume

$262K-$7.3M

More orders spread fixed payroll, rent, and software across more trips, so owner take-home moves from a Year 1 loss to a Year 5 profit.

2

AOV Mix

$49.50

A higher average order value lifts commission and subscription income on the same pickup, which raises cash per stop without much extra cost.

3

Cleaner Margin

40%

If Year 1 platform COGS stays near 60% before route costs, the leftover margin has to cover delivery labor and overhead before the owner gets paid.

4

Route Density

30mo

Dense routes cut wasted drive time and help the model hit breakeven in month 30, which protects owner cash while volume is still ramping.

5

Labor Model

10%-8%

Last-mile payouts that fall from 10.0% to 8.0% by Year 5 leave more gross profit in the business and less in delivery costs.

6

Retention Rank

2.5-5.0x

Repeat orders from higher-retention buyers improve payback on the $45 CAC and keep active customers coming back without fresh ad spend.

Dry Cleaning Pickup and Delivery Service Core Six Income Drivers

Order Volume And Repeat Demand

Repeat Orders

Order volume and repeat demand drive income because each returning buyer raises revenue without paying for a new customer every time. Year 1 weighted repeat demand is 244, based on busy professionals at 250, apartment residents at 180, and corporate accounts at 400; by Year 5 it rises to 280. More repeat orders lift cash flow, but they also push route scheduling, tracking, and support harder.

Here’s the risk: if missed pickups or late returns rise with volume, retention drops and the order engine slows. That hurts gross margin and owner pay because the business spends more on service recovery while collecting less from the same buyer base. In this model, reliability is part of revenue, not just operations.

Track Repeat Rate

Measure repeat orders by customer segment and by route. Watch repeat orders per buyer, missed pickup rate, late return rate, and reorder time. If apartment residents or corporate accounts are below plan, fix service issues before buying more ads. Repeat demand only helps income when the next order arrives on time and clean.

Split repeat demand by segment

Track missed pickups weekly

Log late returns by route

Review churn after service errors

Use volume forecasts to staff dispatch, customer service, and garment tracking. As orders rise, add buffer time to routes and tighter handoff checks. That protects revenue quality and keeps owner income from getting eaten by refunds, rework, and extra labor.

1

Average Order Value And Service Mix

AOV and Service Mix

Average order value, or average ticket, is what you collect per pickup. A higher ticket lifts revenue per stop, but owner pay only rises if the extra sales beat the added cleaner cost, handling time, and claim risk. The model’s weighted AOV input is $4,950 in Year 1 and $5,700 in Year 5, driven by $45 busy professionals, $35 apartment residents, and $120 corporate accounts.

Raise Ticket Without Killing Margin

Track AOV by customer type, item mix, and repeat order. Price suits, dresses, coats, comforters, household bundles, and specialty care so the higher ticket also covers more labor and claims exposure. Here’s the quick math: if a bigger order adds revenue but also adds cleaner payout, driver time, or rework, the margin may not improve. Use the mix that raises contribution per stop, not just sales.

2

Cleaner Partner Cost And Gross Margin

Cleaner Cost and Margin

Your take-home rises only if the spread between customer markup and partner cost stays wide. This model assumes you do not own a dry cleaning plant, so gross margin depends on negotiated cleaner pricing, turnaround time, claims handling, and seller mix. Commission revenue starts at $2 plus 15% of order value in Year 1 and moves to $3 plus 18% by Year 5.

Here’s the quick math: on a $100 order, commission is $17 in Year 1 and $21 in Year 5. That looks better on paper, but poor quality can still create refunds and churn, so cheap wholesale rates do not equal strong profit. The mix also shifts from 40% boutique dry cleaners, 50% laundromats, 10% leather care to 20% / 60% / 20% by Year 5.

Track Margin by Seller Type

Measure margin per order by cleaner type, not just total revenue. Track partner bill, markup, turnaround days, refund rate, and claim rate for each seller group. If one cleaner saves $2 but causes more refunds, it can cut owner pay fast.

Track margin by boutique, laundromat, leather care.

Flag refunds and remake costs weekly.

Test markup by order size and urgency.

Drop sellers that miss turnaround.

Use these inputs in the forecast: order value, partner pricing, markup, claims, and seller mix. The owner’s profit draw improves when cleaner cost stays stable and quality stays high, because fewer refunds mean more cash left after fulfillment.

3

Route Density And Cost Per Stop

Route Density and Cost Per Stop

Dense routes make convenience profitable. When pickups are clustered in the same neighborhoods, apartment buildings, or corporate routes, the business spends less on labor, mileage, fuel, parking time, and insurance exposure, so more order revenue reaches contribution margin and owner pay. The model should keep delivery cost per stop editable because the source data gives demand, AOV, and CAC, but not the delivery math.

Track Cost Per Stop

Measure stops per route, failed stops, and cost per stop by route type. Apartment buildings and scheduled pickup windows should cost less than scattered residential stops, and failed stops need their own line because driver time is spent with no order revenue. If this cost creeps up, the owner pays for convenience twice: once in labor and again in lost margin.

Track stops per route daily.

Separate failed stops from normal stops.

Compare apartment and suburban routes.

Batch corporate pickups on fixed days.

Update owner draw after delivery cost.

Use clustered pickup windows, building access notes, and fixed-day service for larger accounts to lift density. That cuts dead miles and missed pickups, which protects cash flow and makes profit more predictable even when order frequency rises.

4

Labor Model And Owner Role

Owner-Run Delivery

If the owner handles pickups and dispatch, the business can keep more cash because paid delivery and dispatch labor moves onto the owner’s time. That can raise take-home early on, but it also means more driving, more customer messages, more issue resolution, and fewer hours left for sales. Separate wages for work done from profit draw.

A managed setup adds driver payroll, dispatch coverage, customer support, insurance, and quality checks. Those costs can cut operating profit before volume supports the team. The model needs editable payroll, driver cost, and support labor fields so owner pay is not confused with labor paid to the business.

Track The Labor Split

Use three buckets: owner labor, employee labor, and profit. Log miles, stops, message time, failed pickups, and claim handling so you can see what the route really costs. One clean rule: if a task steals time from sales, it has an owner-income cost.

Owner hours by task

Driver pay per stop

Support labor and claim time

Test when the owner should stop being the main driver. If service work starts crowding out sales, add paid help and forecast the drop in owner draw before hiring. That keeps the model honest: pay the owner for work performed, then pay the owner again from business profit only after labor is covered.

5

Customer Retention And Marketing Efficiency

Customer Retention

Retention matters because it spreads the $45 Year 1 buyer CAC across more orders, then lowers it toward $25 by Year 5. That only lifts owner income if households, professionals, apartment residents, and corporate accounts keep reordering after the first pickup, so marketing turns into recurring contribution instead of one-time spend.

Here’s the quick math: buyer marketing rises from $120,000 to $850,000, so churn gets expensive fast. Late deliveries, garment claims, refunds, service errors, weak reviews, and poor cleaner quality push CAC up again, because every lost customer forces the business to buy replacement demand.

Track Repeat Orders

Measure repeat rate, churn, and CAC by segment. The key inputs are new buyers, orders per buyer, ad spend, refund rate, and complaint rate, because those show whether paid marketing is turning into stable revenue and owner draw.

Use simple controls: watch first-order to second-order conversion, log every late delivery and claim, and compare cohort retention for recurring households versus one-off users. If repeat orders rise while CAC falls from $45 to $25, the same marketing budget buys more profit. One clean system beats more ads.

Track CAC by customer segment

Monitor repeat order rate monthly

Flag late deliveries and claims

Test retention by route and cleaner

6

Compare lean, base, and high owner-income scenarios without promising results

Owner income scenarios

Owner pay moves with buyer count, order density, commission mix, and route efficiency, so the same service can stay thin early and improve as repeat use rises.

Low, base, and high owner-income cases for a pickup and delivery dry cleaning model.

Scenario

Low CaseLow Case

Base CaseBase Case

High CaseHigh Case

Launch model

This is the lower earnings path, where demand builds slowly and owner pay stays under pressure.

This is the modeled case, where volume and repeat orders support a steadier owner draw.

This is the stronger earnings path, where better repeat use and denser routes lift owner income.

Typical setup

The model runs with 244 monthly orders, a $4,950 AOV, 15% plus $2 commission, $1,199 buyer subscription, and a $45 CAC, while payroll and overhead absorb most margin.

The business reaches 280 monthly orders, a $5,700 AOV, 18% plus $3 commission, $1,749 buyer subscription, and a $25 CAC as the model moves toward breakeven.

The mature case keeps 280 monthly orders, a $5,700 AOV, 18% plus $3 commission, $1,749 buyer subscription, and a $25 CAC, with more room after reserves and reinvestment.

Cost drivers

244 monthly orders

$4,950 AOV

15% plus $2 commission

$1,199 buyer subscription

$45 CAC

280 monthly orders

$5,700 AOV

18% plus $3 commission

$1,749 buyer subscription

$25 CAC

280 monthly orders

$5,700 AOV

18% plus $3 commission

$1,749 buyer subscription

$25 CAC

Owner income rangeBefore owner reserves

Negative to near-zeroLow Case

Modest positive take-homeBase Case

Strong positive take-homeHigh Case

Best fit

Use this to stress-test early traction, weak route density, and slower repeat use.

Use this as the most balanced case for planning hiring, reserves, and owner pay.

Use this to test upside from better retention, lower CAC, and tighter route economics.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.