How Much EPS Foam Recycling Machine Sales Owners Make at $88M

You’re selling expanded polystyrene (EPS) recycling machines, not running a recycling plant In the supplied five-year planning case, first-year EPS recycling machine sales revenue is $8845M, with owner-pay capacity driven by unit volume, gross margin, overhead, reserves, and after-sale support costs These are planning assumptions before personal taxes, financing terms, and guaranteed distributions

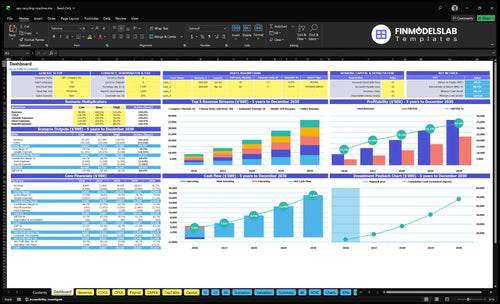

Owner income$4.7MNet margin54%Revenue for target pay$8.8MBusiness difficultyMedium

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner pay depends on volume, margin, payroll, debt, taxes, and reserve policy.

Want the six main income drivers?

1

Annual Units

285-1,005

The model ramps from 285 units in Year 1 to 1,005 in Year 5, so volume is the biggest swing on owner cash.

2

ASP Mix

$310K-$366K

A shift toward higher-priced models lifts weighted ASP from about $310K to $366K, which raises revenue without the same build count.

3

Gross Margin

High

Small gains in build margin flow straight into EBITDA because direct parts, labor, and plant costs sit under every unit.

4

Cash Control

$3.28M

Fixed overhead runs about $3.28M a year, so lease, payroll, software, and utilities must stay tight to protect take-home.

5

Service Revenue

Recurring

Install, training, parts, and field support can add repeat cash after the first sale and smooth income between big orders.

6

Acquisition

$60K

Annual marketing is $60K, and sharper lead spending lowers customer acquisition cost, which matters when sales are technical and slow.

How many EPS recycling machines must I sell to make owner income?

For EPS Foam Recycling Machine Sales, plan on roughly 25 machines before owner income feels safe; pure math shows $205k contribution per machine, but cash timing and support load matter. For KPI tracking, pair this with What Are The 5 Key KPIs For EPS Foam Recycling Machine Sales Business? so sales volume, close rate, and margin stay visible.

Quick math

$310k first-year weighted revenue per machine

$205k contribution after direct selling costs

$3.276M fixed overhead to cover

$175k target CEO salary

Main risk

25 machines gives operating room

285 machines are in the supplied plan

Watch lead flow and close rate

Protect cash timing and support capacity

Can an EPS recycling machine sales business scale profitably?

Yes—but EPS Foam Recycling Machine Sales can scale revenue faster than owner take-home, because each added salesperson, technician, demo unit, inventory deposit, and dealer relationship adds cost before it adds closed deals. With $273k in monthly fixed overhead, $5k in monthly marketing, and a modeled CEO salary of $175k/year (about $14.6k/month), test payroll and working-capital drag before assuming more unit volume improves distributions.

Revenue can rise first

Owner-led selling keeps payroll lean.

Sales staff add cost before deals.

Demo units need cash up front.

Technicians add overhead fast.

Check cash drag first

Fixed overhead is $273k/month.

Marketing adds $5k/month.

CEO pay is about $14.6k/month.

Test inventory deposits before scaling.

What EPS recycling machine sales margin should I watch most?

Watch gross margin first, because it’s the cleanest bridge from machine sales to profit in EPS Foam Recycling Machine Sales, and the plan worksheet is here: How To Write EPS Foam Recycling Machine Sales Business Plan? In the first-year case, gross margin is 77.5% after unit costs and 5% revenue-based COGS; in the mature-year case it rises to 79.0%. One gross-margin point is worth about $88.45k on first-year revenue and $367.55k on mature-year revenue, so small pricing or cost slips matter fast.

Gross margin risks

Watch supplier cost changes first.

Track freight responsibility on every deal.

Charge for installation travel.

Limit warranty exposure in the quote.

Profit protection levers

Price sales commissions into the margin.

Guard against competitive discounting.

Keep gross margin above 77.5%.

Push toward 79.0% in mature years.

Key Takeaways

Machine volume drives the biggest revenue swing.

Mix shifts can lift ASP, but margin matters.

Recurring service income needs installed-base support.

Overhead and reserves can delay owner distributions.

Scenario objective: Compare low, base, and high EPS recycling machine owner income forecasts

Owner income scenarios

Owner income shifts with machine volume, product mix, and cost control. These low, base, and high cases show how much pool is left for the owner after operating costs.

Low, base, and high owner-income cases for EPS foam recycling machine sales.

Scenario

Low CaseDownside

Base CaseCore

High CaseUpside

Launch model

This is the lean owner-income case with slower sales and a thinner pool for the owner.

This is the modeled middle case with steadier sales and a more balanced owner pool.

This is the stronger owner-income case with higher volume and a larger pool after costs.

Typical setup

Year 1 volume is 285 machines with $8.845M revenue, higher variable selling and delivery costs, and $3.276M fixed overhead.

Year 3 volume is 600 machines with $20.495M revenue and 10.0% variable costs across the operating base.

Year 5 volume is 1,005 machines with $36.755M revenue and 8.5% variable costs at scaled throughput.

Cost drivers

285 machines

$8.845M revenue

11.5% variable selling and delivery costs

$3.276M fixed overhead

owner-led setup

600 machines

$20.495M revenue

10.0% variable costs

Year 3 mix

balanced operating scale

1,005 machines

$36.755M revenue

8.5% variable costs

Year 5 mix

scaled cost control

Owner income rangeBefore owner reserves

$551kLean pool

$1.368MBase pool

$2.559MScaled pool

Best fit

Use this to test an owner-led launch where sales stay modest and cost control matters most.

Use this as the main planning case for a steady operator who wants a realistic middle path.

Use this for a scaled-cost plan that assumes strong throughput and better cost absorption.

!

Planning note: These scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution advice.

EPS Foam Recycling Machine Sales Core Six Income Drivers

Annual Machines Sold

Annual Machines Sold

Annual machines sold is the biggest swing factor for owner income. Each first-year machine averages about $310k in revenue and $205k in contribution after direct and variable selling costs, so volume alone can move the year from about $88.4M at 285 units to about $311.6M at 1,005 units.

This business sells into niche B2B demand, so long buyer approvals and installation capacity can slow throughput. One missed machine is not fatal, but a weak quarter can push cash back and delay owner distributions even when the pipeline still looks strong.

Track units from approval to install

Measure booked units, approved units, shipped units, and installed units separately. That tells you where deals stall. Here’s the quick math: every delayed machine holds back about $310k of revenue and $205k of contribution, so forecast owner pay from installed and collected units, not just signed contracts.

Watch install crew slots, backlog age, and monthly close timing. If demand is there but installs are tight, revenue can slip without warning. Keep a live unit plan so the team knows whether the quarter is on pace for 285 machines or closer to 1,005.

Booked units by month

Days from approval to install

Install crew capacity

Cash collected per unit

Lead Quality And Close Rate

Lead Quality And Close Rate

Lead quality is the filter between activity and cash. For EPS foam recycling machine sales, real leads must come from commercial buyers like warehouses, manufacturers, recyclers, packaging users, and municipalities. Traffic is not revenue; revenue starts only when deals close and deposits clear.

The income hit is mostly in commission and cash timing. The model assumes $5,000 per month for marketing and SEO, with commissions at 50% in year one and 40% later. Since lead cost and close rate are not supplied, the owner should test both before counting any income.

Track Real Buyers, Not Clicks

Measure qualified commercial leads, not raw traffic. Track the number of buyer calls, site visits from target accounts, demos booked, quotes sent, deposits received, and closed deals. If a lead is not a warehouse, manufacturer, recycler, packaging user, or municipality, it should not flow into the sales forecast.

Here’s the quick math: if marketing stays at $5,000 per month, then owner income depends on how many of those dollars turn into closed machines before the 50% commission check goes out. Build the calculator around close rate and deposit timing, because slow closes can turn “sales interest” into dead cash flow.

Count qualified buyer leads only

Track close rate by source

Test deposit timing, not just quotes

Average Selling Price And Configuration Mix

Average Selling Price And Mix

When the mix shifts toward higher-capacity, automated, or installed EPS recycling machines, average selling price (ASP) rises. In the supplied model, weighted ASP moves from $310k to $366k, with first-year prices spanning $85k mobile recyclers to $185k compact thermal units. That lifts revenue per deal, but owner income only improves if gross margin, close rate, and payment timing hold up.

Here’s the quick math: a higher ASP adds more top-line dollars per win, so the same sales effort can fund more profit and salary draw. But bigger configurations can also mean longer approvals, more install work, and slower payments. If the mix rises but discounts, warranty cost, or receivables rise too, take-home cash can stay flat.

Track Mix, Not Just Price

Measure ASP by model, plus the attach rate for automation, installation packages, and accessories. Keep a simple quote log that shows list price, discounts, deposit %, and days to collect. That tells you whether a higher-priced deal is truly better, or just slower and riskier. One clean rule: don’t celebrate ASP if cash lags.

Track ASP by machine type.

Watch close rate by quote size.

Match deposits to build timing.

Test discount limits by segment.

If larger configs close slower, keep a split view in the forecast: booked revenue, shipped revenue, and collected cash. That protects owner pay when a $366k mix looks strong on paper but lands late in the bank.

Gross Margin Per Machine

Gross Margin Per Machine

This driver is the profit left after unit cost and variable selling costs on each EPS recycling machine. With supplied unit costs of $315k to $162k and 5% revenue-based COGS, gross margin is the bridge between the sale and owner pay, not the pay itself. If landed cost rises, take-home falls even when revenue holds.

The supplied model states first-year gross margin at 775% and mature-year gross margin at 790%. That gap can shrink fast if freight, tariffs, warranty claims, installation overruns, discounts, or weak payment terms pile up. The quick check is simple: gross profit per machine minus fixed overhead and reserves is what funds distributions.

Control Landed Cost

Track each machine’s landed cost by model: factory price, freight, tariffs, install labor, warranty reserve, and sales discount. Then compare it to the signed price before you book the deal. One clean number matters: gross profit per machine.

If you sell faster but give up margin on rush orders or bad terms, owner income still drops because cash is tied up longer and paybacks slip. Tighten quoting rules, cap discounting, and price freight and installation separately so gross margin stays intact when volume rises.

Service, Parts, And Installation Revenue

Service, Parts, and Installation Revenue

This driver is the money after the first machine sale: installation, training, parts, preventive maintenance, and service agreements. The supplied model does not show a service revenue line, so don’t treat it as automatic income. In year one, installation and training travel can run 25% of first-year revenue; in mature years, that drops to 15%.

The key inputs are installed base size, service attach rate, parts usage, and technician capacity. More contracts can lift cash flow, but only if support is staffed. If recurring revenue is booked before the team can respond, owner pay gets squeezed by callbacks, warranty work, and travel.

Build Support Income Safely

Track revenue per installed machine, ticket count, and average response time. Model parts and maintenance from the live fleet, not from hopeful demand. One clean rule: no support capacity, no recurring revenue.

Installed base by machine model

Service attach rate and contract price

Technician hours and travel miles

Parts usage and preventive visits

Price service to cover labor and travel. Watch 25% of first-year revenue for install and training travel, then 15% in mature years. If technician time is tight, limit contract sales until the backlog clears.

Overhead, Reserves, And Working Capital

Overhead, Reserves, And Working Capital

Overhead is the cash you must cover before owner pay starts: payroll, office, sales admin, insurance, rent, software, and similar fixed costs. Here, fixed overhead is $273k per month, or $3.276M per year, before the $175k CEO salary. So sales can look strong, but distributions still get squeezed if cash sits in inventory deposits, freight, demo units, commissions, warranty reserves, or receivables.

The key input is the reserve plan, not just profit. Set a reserve percentage for working capital, then hold cash back until deposits clear, delivery is done, and receivables age down. If you include the CEO salary, fixed cash load is about $287.6k a month. Owner take-home falls fast when reserves are too thin and the business funds growth with cash meant for tax, freight, or support.

Set A Reserve Floor

Track inventory deposits, freight, demo units, commissions, warranty reserves, and receivables reserve each month. Build a simple cash bridge: opening cash + collections - overhead - reserve adds - distributions. If the reserve rate is not set, do not pay out excess cash yet. The business can be profitable and still run short on cash if collections lag or installs slip.

Set one reserve percentage.

Separate tax and operating cash.

Hold back before distributions.

Review aged receivables monthly.

Use a 13-week cash forecast to test slow deposits, late customer payments, and warranty hits. If the reserve keeps dropping below the overhead run rate, cut owner draws first, not support spend. That protects payroll, freight, and service capacity, which protects future sales and the owner’s paycheck.