How Much Foreclosure Prevention Counseling Owners Make: $115K Plan

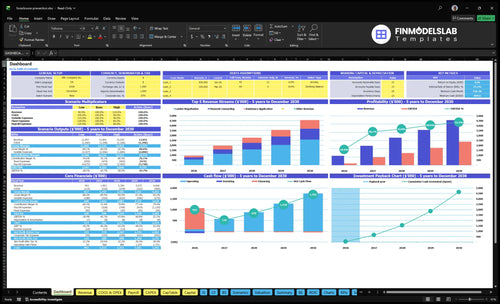

You’re modeling owner take-home before the practice has enough case volume to cover payroll In this researched plan, the owner role is modeled as a $115,000 annual Executive Director salary, but Year 1 revenue is only $158,500 and the business still shows a large operating loss, so distributions are not supported

Owner income$115k salaryNet margin18.9%Revenue for target pay$158.5kBusiness difficultyHard

Want to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

How many foreclosure counseling clients do you need to make money?

For Foreclosure Prevention Counseling, Year 1 breakeven is about 55 acquired households a month. Here’s the quick math: $463,800 in annual payroll, overhead, and marketing divided by $707 contribution after direct costs and $450 CAC equals about 656 households a year. The current plan is only 100 households, so owner pay stays separate from the gross revenue target, and pay gets safer when referral CAC falls.

Breakeven math

55 households per month

656 households per year

$707 contribution each

$450 CAC cuts cushion

What helps the model

Lower referral CAC fast

Keep owner pay separate

Hold fixed costs tight

Grow acquired households

What profit margin can a foreclosure prevention counseling business earn?

If you’re pricing Foreclosure Prevention Counseling, the year 1 gross margin can look strong at 73% after 8% documentation and filing, 4% credit verification, 10% referral commissions, and 5% portal usage. But once you add How Much To Start Foreclosure Prevention Counseling Business?, the operating margin can still turn negative with $324,000 payroll, $94,800 fixed overhead, and $45,000 marketing.

Gross margin view

73% gross margin in year 1

27% total variable cost load

10% referral commissions hit hard

5% portal usage adds drag

Operating pressure

$324,000 payroll is the biggest load

$94,800 fixed overhead sits on top

$45,000 marketing cuts into profit fast

High volume can still mean low owner income

Can a foreclosure prevention counseling business make money?

Yes, Foreclosure Prevention Counseling can make money, but the funding model matters because many homeowners expect free help; see How Much To Start Foreclosure Prevention Counseling Business? before pricing the service. In the Year 1 paid-case model, $158,500 from 100 households is overwhelmed by $324,000 payroll, $94,800 fixed overhead, and $14,400 annual compliance review cost.

Money Model

Earn from compliant client fees

Add grants and nonprofit funding

Use lender or servicer contracts

Offer paid workshops and agency partnerships

Profit Check

Revenue: $158,500 from 100 households

Payroll: $324,000 before overhead

Fixed overhead: $94,800 per year

Never promise foreclosure outcomes or improper advance fees

Want the six drivers that move owner income?

1

Qualified Volume

100 homes

Each qualified homeowner adds a new case path, and the Year 1 plan starts with 100 households.

2

Case Revenue

$1,585

At $1,585 per case, pricing and service mix drive most of the take-home lift.

3

Intake Conversion

73%

Turning more qualified homeowners into active cases protects the 73% gross margin before fixed costs.

4

Counselor Utilization

4.5 hrs

At 4.5 billable hours per active client each month, more counselor time turns into revenue instead of idle labor.

5

Acquisition Cost

$450

Keeping CAC near $450 protects payback and keeps marketing from eating the margin.

6

Compliance Overhead

$94.8K

Annual fixed overhead is $94.8K, plus $1.2K a month for legal compliance, so reserves have to come before owner draws.

Foreclosure Prevention Counseling Core Six Income Drivers

Qualified Homeowner Volume

Qualified Homeowner Volume

Raw leads do not pay the owner; qualified, eligible, serviceable households do. In Year 1, marketing supports 100 acquired households, or about 83 per month. Under the Year 1 cost structure, break-even is about 55 households per month, so volume only lifts owner pay if enough cases convert to billable work.

Here’s the catch: every extra household needs intake, document collection, counselor time, and compliance records. If qualification is weak, counselor hours get burned on dead-end files and CAC rises, which cuts cash flow before revenue shows up.

Measure Qualified Volume, Not Raw Leads

Track inquiry-to-qualified household rate, qualified households per month, and cases closed per counselor. The key test is simple: if qualified volume stays under 55 per month, fixed costs and payroll pressure owner draw. Better screening protects margin by filtering out ineligible or unserviceable cases before staff spends time on them.

Keep the intake checklist tight: mortgage status, hardship proof, contactability, and willingness to share documents. If document collection slows or compliance notes fall behind, volume looks good on paper but cash collection and fee billing slip. More households help only when the team can process them cleanly.

1

Average Revenue Per Case

Average Revenue Per Case

Average revenue per assisted household is the clearest pricing lever in this model. Year 1 is $1,585: $375 financial counseling, $910 lender negotiation at 65% allocation, and $300 assistance application at 40% allocation. If the mix shifts toward higher-rate work, Year 5 rises to $2,255.

This driver lifts gross margin and owner pay because each case helps cover fixed labor and overhead faster. The catch is fee rules: review what can be billed before charging homeowners. Grants, contracts, workshops, and partnerships can make cash flow steadier, but weak pricing or the wrong service mix cuts profit fast.

Improve Case Revenue Mix

Track revenue by service line, then compare it with the share of cases using each service. The main inputs are case mix, billed hours, approval rates, and fee rules. With 100 assisted households, a $100 lift in average revenue adds $10,000 a year before costs.

Measure revenue per counselor file.

Watch negotiation and application shares.

Price higher-touch work with care.

Document every billable step.

If negotiation work or application help takes more time, pricing and staffing need to rise with it. Otherwise, average revenue may look stable while margin slips. Keep the mix lean, and use grants or contracts to smooth cash without leaning on homeowner fees alone.

2

Intake Conversion And Completion

Intake Conversion and Completion

Intake conversion is the share of consultations that turn into active, billable cases. This model starts from acquired households, not raw inquiries, so weak screening wastes counselor hours and cuts revenue fast. If a case never becomes billable, the owner still pays for intake time, follow-up, and compliance work, but gets no fee back.

The key inputs are consultation-to-active-case rate, completed documents, hardship urgency, lender communication, and follow-up speed. Better fit protects families and margins. More volume only helps when the file is ready, because completed cases create the billable hours that pay payroll and support owner draw.

Screen for ready cases

Track consultation-to-active-case rate, document completion rate, and cases closed per counselor. If Year 1 acquisition reaches 100 households, every lost conversion reduces revenue and raises labor cost per closed file. Pressure selling is the wrong lever; confirm hardship, documents, and lender contact before enrollment.

Check mortgage status first.

Verify income and expense proof.

Log lender response dates.

Use a tight follow-up process so incomplete files do not sit idle. When documents are missing, cash collection slows and counselor time gets trapped in rework instead of billable work. Clean intake lifts margin because the same payroll produces more completed cases, not just more conversations.

3

Counselor Capacity And Labor Cost

Counselor Labor Cost

If counselor staffing runs hot, owner take-home drops fast. Year 1 payroll is $324,000, or about $27,000 per month, across a $115,000 executive director, $75,000 senior counselor, $82,000 loss mitigation specialist, and $52,000 intake coordinator. That cost has to clear before the owner pays themselves, so the real test is how many files each role can handle without hurting service.

Owner-handled files cut cash payroll, but the labor still exists as unpaid owner time. It shows up in supervision, training, case notes, quality control, and compliance review. The key inputs are active files, hours per case, and staff coverage. If caseload grows faster than review capacity, profit can look fine on paper while owner pay gets squeezed.

Track Files Per Counselor

Track completed cases per counselor, not just incoming leads. Tie staffing to active files, average time per file, and how much review each file needs. When a counselor can take more files only by skipping notes or compliance checks, labor stops creating clean revenue and starts creating rework. Keep a weekly count of open files, closed files, and overdue documentation.

Test whether adding staff really lifts take-home income. If a new hire adds capacity, it should also reduce owner supervision time and raise completed cases enough to cover the extra payroll. If not, the hire is just fixed cost. A simple rule helps: do not expand headcount until file load, note quality, and compliance review all stay current.

4

Client Acquisition Cost And Referrals

Client Acquisition Cost and Referrals

This driver is the cost to turn a qualified homeowner into an active client. At $450 CAC in Year 1, and $1,157 gross profit per household, acquisition leaves about $707 before overhead and owner pay. By Year 5, CAC falling to $325 lifts that cushion to about $832.

Inputs are acquired households, channel mix, referral share, and close rate. Trusted referrals from lenders, legal aid, nonprofits, churches, real estate professionals, and housing agencies usually cost less than paid ads, but only if intake stays compliant and non-predatory.

Track CAC by source, not just total spend

Measure CAC as marketing and sales cost divided by new active households, then split it by channel. That shows whether referrals are beating paid ads and whether one partner source is sending better-fit cases. A simple target is lower CAC with no drop in completion rate or file quality.

Track CAC by partner

Count active, qualified households

Review close rate monthly

Document referral sources

Keep scripts compliant

What this estimate hides is labor waste from bad-fit leads. If screening is weak, counselor time rises and contribution falls fast. So protect margins by qualifying hardship, service fit, and document readiness before any deep work starts.

5

Overhead, Compliance, And Reserves

Fixed Overhead, Compliance, And Cash Buffer

Fixed overhead is $7,900 per month, or $94,800 per year, before any owner pay. That covers $4,500 rent, $800 software, $650 liability insurance, and $1,200 legal compliance and audit services. In a fee-for-service model, this cost base hits take-home income fast, so the business needs enough completed, billable cases just to stay ahead of fixed spend.

Reserves are a planning buffer, not leftover profit. The model also shows $810,000 minimum cash in Month 2, and early capex totals $83,700. That cash need matters because it protects payroll, compliance, and client service when collections slow or intake slips. If reserves are thin, owner draws should wait until cash is stable, not just until the P&L looks positive.

Track Run-Rate And Cash Before Drawing Profit

Watch three inputs every month: fixed overhead, completed billable cases, and cash on hand. Overhead includes rent, software, insurance, and compliance work, so it should stay mapped to a monthly run-rate, not managed as a one-time bill. If case volume softens, the overhead ratio rises and owner income falls even when lead flow looks healthy.

Use a simple rule: keep reserves separate from profit and separate from capex. Track whether cash stays above the $810,000 Month 2 minimum after paying the $83,700 early build-out costs and monthly fixed spend. If compliance reviews or audit support start slipping, that is a margin leak, not a back-office detail.

Review overhead against monthly case volume.

Reserve cash before owner distributions.

Protect compliance spend every month.

6

Compare low, base, and high owner-income cases

Owner income scenarios

Owner income moves with households served, CAC, and fixed payroll. At 100 households, the model can support a $115,000 salary line, but distributions stay at zero.

Low, base, and high owner pay cases for a foreclosure prevention counseling model.

Scenario

Low CaseLow Case

Base CaseBase Case

High CaseHigh Case

Launch model

Lower case flow leaves the business loss-making and owner pay funding dependent.

Modeled case flow supports the planned salary line but leaves no distribution.

Stronger volume reaches breakeven and can support owner pay beyond the salary line.

Typical setup

Below 100 households a year at about $1,585 revenue per case, the fixed payroll and overhead run ahead of margin.

At 100 households, the model shows $158,500 revenue, 73% gross margin, a $115,000 salary line, and $0 distributions.

At about 656 households a year, the model reaches breakeven under Year 1 CAC, fixed overhead, payroll, and reserve needs.

Cost drivers

Sub-100 households

Year 1 CAC $450

$7,900 fixed overhead

heavy payroll

reserve strain

100 households

$158,500 revenue

73% gross margin

$115,000 salary line

$810,000 cash need

656-household breakeven

Year 1 CAC $450

fixed overhead

payroll growth

reserve needs

Owner income rangeBefore owner reserves

Loss-makingLow Case

$115,000 salary onlyBase Case

Breakeven upsideHigh Case

Best fit

Use this to stress-test funding needs when case flow stays below 100 households a year.

Use this for a funded plan built around 100 households and salary-only owner pay.

Use this to test upside if volume clears breakeven and funding still covers reserves.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.