How Much Glass Recycling Owners Can Make: $127M Year 1

Key Takeaways

More accepted tons spread fixed costs.

Fees stabilize cash before resale.

Cleaner glass boosts saleable yield.

Uptime converts volume into income.

Owner incomeN/ANet margin69.8%Revenue for target pay$12.7MBusiness difficultyHard

Want to test your glass recycling profit calculator?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

How do you check owner income in the Glass Recycling model?

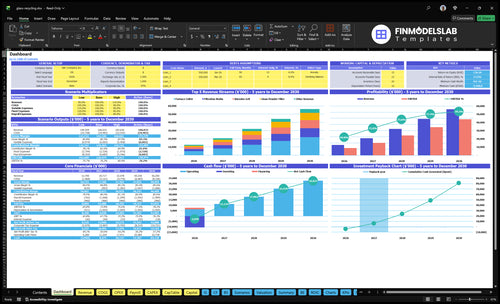

The dashboard in the Glass Recycling Financial Model Template shows revenue by product, processed volume, gross margin, known variable costs, owner pay, break-even volume, and cash reserve logic. Year 1 to Year 5 ramps from $127M and 95,000 units to $562M and 360,000 units, so you can test pricing, tonnage, freight, uptime, reserves, and owner draw—open the model.

Owner-income model highlights

Owner pay and draw

Revenue, margin, and volume

Scenarios, reserves, and uptime

Can you make money recycling glass?

Yes, you can make money in Glass Recycling, but only when clean supply, signed buyers, tight processing costs, and hauling economics work together; see What Is The Main Goal Of Glass Recycling Business? for the operating lens. The researched case needs a unit check: $127M revenue and $197M direct COGS would mean a $70M gross loss, while an 84.5% gross margin would imply direct COGS near $19.7M, before $635k in commissions and outbound logistics.

What makes money

Lock B2B contracts first

Keep inbound glass clean

Process tons with low waste

Sell higher-value glass products

What can kill profit

Heavy freight eats margin

Contamination raises labor cost

Maintenance drains cash fast

Debt reduces owner pay

What is the glass recycling cost per ton?

Glass Recycling cost per ton depends on product mix, sorting quality, contamination, hauling, labor, energy, and maintenance. For the startup cost side, see What Is The Estimated Cost To Start Your Glass Recycling Business?; in Year 1, direct COGS averages $2,072 per unit, including $1,671 unit COGS and $401 revenue-based COGS. Product-level direct cost runs from about $450 for construction aggregate to $13,400 for glass powder filler before sales and outbound costs, and known variable cost averages about $2,740 per unit. Contamination rates are not supplied, so keep them editable.

Cost drivers

Product mix changes cost fast.

Sorting quality cuts rejects and labor.

Hauling and maintenance add drag.

Energy rises with processing intensity.

Year 1 numbers

$2,072 direct COGS average.

$1,671 unit COGS plus $401 revenue-based COGS.

$450 to $13,400 cost range.

$2,740 known variable cost average.

How much revenue can a glass recycling business make?

Glass Recycling can make very different revenue depending on scale and product mix, but the model here shows $127M in Year 1 on 95,000 units and $562M in Year 5 on 360,000 units. Here’s the quick math: Year 1 average revenue is about $13,368 per unit across furnace cullet, construction aggregate, filtration media, abrasive grit, and glass powder filler. The known contribution is about $10,628 per unit before fixed overhead, so owner pay, reserves, and fixed costs all have to be covered from that spread.

Year 1 revenue

$127M on 95,000 units

$13,368 average per unit

Multi-product sales drive value

Revenue is scenario-based

What drives break-even

$10,628 contribution per unit

Add owner pay to fixed costs

Include cash reserves too

Divide by contribution per unit

Want the six main glass recycling income drivers?

1

Supply Volume

95K-360K

More tons processed push revenue from 95,000 units in Year 1 to 360,000 in Year 5, so throughput is the main owner-income lever.

2

Contract Pricing

$40-$880

Sale price per product swings from $40 for construction aggregate to $880 for glass powder filler, and every rate change drops straight into revenue.

3

Product Mix

51%-53%

A larger share of filtration media, abrasive grit, and glass powder filler keeps more revenue in higher-value lines and lifts take-home profit.

4

Yield Control

0.4%

Cleaner input and better sorting protect the 0.4% quality control load and the $0.20 per-unit waste cost, which keeps COGS from creeping up.

5

Uptime

3.0%

Higher equipment uptime spreads the 3.0% processing cost stack over more sellable output and improves owner take-home.

6

Cost Control

$94.8K/mo

Keeping logistics, labor, utilities, and maintenance tight protects the monthly fixed base of about $94.8K before output growth kicks in.

Glass Recycling Core Six Income Drivers

Consistent Inbound Glass Volume

Inbound Glass Volume

Accepted tons are the real driver here, not just what gets collected. The model scales from 95,000 processed units in Year 1 to 360,000 in Year 5, so more clean inbound volume can spread fixed costs, support owner pay, and steady cash flow. One clean rule: volume only helps when the plant can turn it into saleable output.

Track collected tons, accepted tons, and saleable tons separately after contamination and processing loss. Here’s the quick math: saleable tons × selling price − fixed costs. Extra inbound glass can hurt cash if buyer demand, crusher throughput, labor, or storage lag behind. Then you pay to handle more material without turning it into revenue.

Measure Accepted Tons, Not Just Loads

Use a weekly dashboard for received tons, rejected tons, and saleable yield. That shows whether more inbound volume is actually feeding profit or just adding handling cost. If contamination rises, the business may look busier while owner income falls.

Match supply contracts to outlet demand before chasing more tons. If the crusher, labor schedule, or storage fills up first, revenue quality drops fast. The best volume is steady volume that the plant can process, sell, and collect cash on without bottlenecks.

1

Collection Fees And Contract Pricing

Collection Fees and Contract Pricing

When cullet prices fall, collection fees, drop-off fees, municipal contracts, and commercial service pricing keep cash coming in. The key number is fee per accepted ton, because heavy glass can make hauling costly; Year 1 outbound logistics already run about 30% of revenue, so weak service pricing can wipe out owner pay fast.

Model fee mix, customer type, rejected load charges, and payment timing. Municipal and commercial contracts usually stabilize income better than spot resale, but only if route density is high and contract terms cover transport, sorting, and downtime. One weak clause on rejected loads can turn a profitable route into a cash drag.

Price the route, not just the ton

Track what each customer pays per accepted ton, how much volume is tied to municipal vs commercial work, and how fast invoices turn into cash. The quick test is simple: if service fees do not cover hauling, labor, and disposal before cullet sales, the route is underpriced.

Separate accepted and rejected tons

Log payment days by contract

Charge for contaminated loads

Review route density monthly

2

Cullet Sale Price And Buyer Demand

Buyer-Spec Pricing

Cullet sale price is the price per ton you get after processing glass into a buyer-ready product. In Year 1, modeled prices run from $40 for construction aggregate to $800 for glass powder filler, with $100 furnace cullet, $300 abrasive grit, and $500 filtration media. Better color, purity, and freight terms lift revenue per ton, so owner income improves without the same jump in fixed cost.

This driver depends on saleable tons, product mix, buyer requirements, region, and haul distance. If a ton is downgraded from $500 media to $100 furnace cullet, gross margin drops fast even if processing cost barely changes. Weak specs or long freight can push volume into lower-value outlets and cut the owner’s take-home pay.

Track Mix, Specs, And Freight

Price the same ton by outlet, not by “glass” as one bucket. Track accepted tons, saleable tons, product grade, and realized price per ton by buyer, then compare that against freight and rework cost.

Measure price by product line.

Log buyer spec failures.

Watch freight per mile.

Test higher-value outlets first.

Use buyer quotes, color sort results, and purity tests to forecast cash. If a higher-grade outlet needs cleaner feed, price that extra sorting into the sale. That keeps contribution per ton rising instead of letting shipping and rejected loads eat the owner’s profit.

3

Contamination Rate And Cullet Quality

Contamination Rate And Cullet Quality

Cleaner inbound glass raises saleable yield and cuts disposal cost. When loads carry ceramics, trash, metals, mixed-stream contamination, or poor color separation, a ton can be rejected or downgraded, so revenue per processed ton falls while labor and hauling still happen. The model already includes waste disposal unit costs, but contamination rate should be an editable input.

The main inputs are accepted tons, contamination rate, downgraded tons, saleable yield, and disposal cost per rejected ton. If contamination rises, owner take-home drops because the same collection and processing work produces fewer furnace-ready tons. Even a small shift hurts cash flow when fixed labor and route costs stay in place.

Track Rejects At The Gate

Log rejected tons and downgraded tons by source, color, and load type. If one supplier or route creates more trash or mixed colors, tighten specs or charge for sorting. That keeps bad material from eating margin before it reaches the plant.

Accepted tons by supplier

Reject rate by load type

Downgraded tons by color mix

Disposal cost per rejected ton

Test the model with a 1 to 3 point drop in contamination. The gain shows up twice: more saleable cullet and less disposal spend. That protects cash flow and makes owner pay steadier because fixed labor and hauling are spread across more usable product.

4

Processing Capacity And Equipment Uptime

Processing Capacity And Uptime

When the plant is down, contracted glass still sits in the yard, but it doesn’t become revenue. This driver matters because higher equipment utilization spreads lease, labor, insurance, and maintenance across more saleable tons, and the model ramps from 95,000 processed units in Year 1 to 360,000 in Year 5.

Here’s the quick math: maintenance and repairs are set at 0.6% of revenue, rising from $762k to $3.372m across that ramp. Downtime cuts income even when buyers exist, so low uptime hurts cash flow twice: fewer billable tons and more cost per ton. Uptime turns contracted volume into billable output.

Track Uptime, Not Just Volume

Measure scheduled hours, running hours, tons per hour, and unplanned downtime. Uptime is the share of planned time the line actually runs, and it should be tied to billable tons, not just inbound receipts.

Track planned vs. unplanned stops.

Log tons lost per outage.

Watch repair cost per processed ton.

Match labor to line hours.

If maintenance slips, output falls fast and fixed costs stop spreading. Use a weekly uptime target, compare it to accepted tonnage, and keep spare parts ready for the bottlenecks that stop throughput first.

5

Logistics, Labor, Utilities, And Maintenance Control

Logistics and plant cost control

Heavy glass can turn profit into freight spend fast. In this model, outbound logistics runs at 30% of revenue, or $381k in Year 1, and processing energy is 8% of revenue, or $1,016k. Direct processing labor is already inside unit COGS, so the owner’s take-home depends on how well routes, shifts, power use, and machine wear are controlled.

Here’s the quick math: shorter hauls, fuller trucks, tighter labor scheduling, and fewer breakdowns raise contribution per ton. If route density drops or fuel rises, margin falls before sales do. The risk is simple: moving glass too far or too often can eat the cash that should fund owner pay.

Track cost per ton, not just total spend

Measure haul miles per ton, fuel per route, kWh per processed ton, labor hours per shift, and downtime by machine. Split costs by accepted ton, saleable ton, and rejected ton so you can see where profit leaks. If a lane is thin or a shift is idle, fix that before you add volume.

Pack routes to cut deadhead miles.

Match shifts to inbound volume.

Track maintenance before breakdowns.

Compare energy use by product line.

What this hides: the same ton can cost very different amounts to move and process. If outbound freight stays near 30% of revenue, owner draw stays tight; if cleaner scheduling lowers that cost, more gross profit stays in the business and can be paid out.

6

Compare lean, base, and high glass recycling income scenarios

Owner income scenarios

Owner income rises with volume, product mix, and plant use. Higher-value output helps, but debt, taxes, reserves, and owner pay still decide what the founder can actually take home.

Low, base, and high cases for the recycling plant.

Scenario

Low CaseEasier start

Base CaseBalanced case

High CaseCapacity heavy

Launch model

This is the lower earnings path if the plant stays near first-year volume.

This is the modeled middle path once the plant is running at a steadier Year 3 pace.

This is the stronger earnings path if Year 5 capacity and product mix hold.

Typical setup

Year 1 runs 95,000 units, about $12.7M revenue, and roughly $1.6M direct unit COGS before fixed overhead and owner pay.

Year 3 reaches 220,500 units, about $32.1M revenue, roughly $3.8M direct unit COGS, and a fuller plant and sales team.

Year 5 reaches 360,000 units, about $56.2M revenue, roughly $6.4M direct unit COGS, and more staffing to keep the plant full.

Cost drivers

Low throughput

raw material acquisition

direct processing labor

facility rent

outbound logistics

Higher utilization

product mix

direct processing labor

sales commissions

outbound logistics

Full capacity

higher-value products

direct processing labor

sales commissions

outbound logistics

Owner income rangeBefore owner reserves

About $8.9M EBITDA proxyYear 1 proxy

About $24.3M EBITDA proxyYear 3 proxy

About $44.0M EBITDA proxyYear 5 upside

Best fit

Use this to stress-test early plant ramp, lean sales, and the first year of owner take-home.

Use this as the planning case for a steady plant, fuller utilization, and normal sales coverage.

Use this to test upside if throughput, pricing, and staffing all scale cleanly.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.