How Much Can A Herbal Tea Production Owner Make On $835K Sales

A herbal tea production owner can take home money only after herbs, packaging, labor, marketing, platform fees, overhead, and cash reserves are covered In the researched first-year assumptions, revenue is $835,000, gross margin is about 890%, and operating profit before owner pay is about $599,400 That is a planning result, not a salary benchmark The model’s fifth-year forecast reaches $348 million in revenue and about $289 million in operating profit before owner pay and reserves

Owner income$599.4kNet margin31.6%Revenue for target pay$380kBusiness difficultyHard

Want to test your own herbal tea income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margins, payroll, reserves, and cash timing.

Want to check owner income in the Herbal Tea Production model?

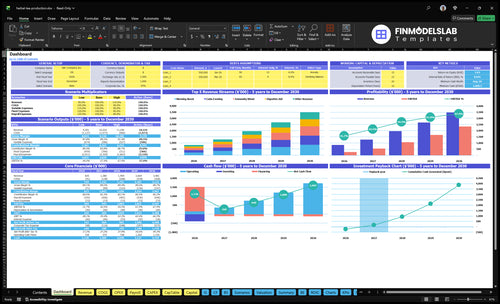

The dashboard in the Herbal Tea Production Financial Model Template shows revenue, gross margin, operating profit, and owner-income scenarios. Assumptions tabs cover units, pricing, batch costs, packaging, channel mix, payroll placeholders, fixed and variable expenses, inventory, and cash flow. Open the model to see the income drivers.

Owner-income model highlights

Revenue: $835k to $348M

Operating profit: $599.4k to $289M

Assumptions drive owner pay

How much can a herbal tea business owner make?

A Herbal Tea Production owner could take home money from profit, but it’s not a guaranteed salary: first-year assumptions show $835,000 revenue and $599,400 operating profit before owner pay, taxes, debt service, and reserves. For market context, see What Is The Current Growth Rate Of Herbal Tea Production?; the fifth-year forecast shows $348 million revenue and $289 million operating profit before owner pay.

Owner Pay Range

Start from $599,400 operating profit

Subtract taxes, debt, and reserves

Pay wages, draws, or distributions

Reinvest cash to fund growth

What Changes Take-Home

Shift channel mix toward higher margins

Control production labor costs

Track marketing spend by sale

Define the owner’s operating role

How much revenue does a herbal tea business need to pay the owner?

Herbal Tea Production needs enough revenue to cover the owner’s pay, $73,200 in first-year fixed overhead, and 85% variable selling costs. Here’s the quick math: revenue target = owner pay + fixed costs divided by contribution margin after COGS and selling costs, and the supplied model says the gross margin is high. What this hides: taxes, debt service, wholesale discounts, and inventory reserves can still drain cash fast.

Core math

$73,200 fixed overhead first year

85% variable selling costs

Owner pay adds to the target

Gross margin drives the gap

Cash risk

Wholesale discounts cut revenue

Inventory reserves tie up cash

Taxes reduce take-home pay

Debt payments lower free cash

Is wholesale or direct to consumer better for herbal tea profit?

For Herbal Tea Production, direct-to-consumer usually protects price better, but wholesale can move more units if you need volume and steadier orders. The tradeoff is simple: direct sales add marketing, payment fees, fulfillment, and customer service, while wholesale lowers your selling price and delays cash collection. Subscriptions can improve repeat revenue if churn stays low, and farmers markets can validate blends but they take owner time.

Direct sales

Protects price on every sale

Adds marketing work and spend

Brings card and payment fees

Requires packing and support time

Wholesale tradeoffs

Moves more units faster

Usually cuts the unit price

Delays cash until invoices clear

Can raise freight and inventory pressure

Repeat revenue

Subscriptions work if churn stays low

Retail accounts can lift volume

Private label can add scale

Higher revenue can still lower profit

Watch the margin

Discounts can eat gross profit

Freight can cut returns fast

Inventory ties up working capital

Labor can rise faster than sales

Want the six drivers behind owner take-home?

1

Channel Mix

$835K

Where the $835K first-year sales land changes fees, cash timing, and how much profit reaches the owner.

2

Gross Margin

890%

A tighter unit margin keeps more of each tea sale after herbs, packaging, labor, and shipping.

3

Capacity

36K

At 36,000 units in year one, output drives how fast fixed overhead gets spread and payback starts.

4

Pricing Mix

$21-$28

The $21 to $28 price band lets mix shifts lift profit without adding much factory load.

5

Acquisition

$70.98K

The $70.98K variable selling cost base moves with ads and payment fees, so retention helps protect take-home.

6

Owner Reserves

$599.4K

After $73.2K fixed overhead and $599.4K operating profit before owner pay, the draw and reserve plan decides what cash the owner keeps.

Herbal Tea Production Core Six Income Drivers

Channel Mix

Channel Mix

Channel mix is the split across DTC, wholesale, retail, subscriptions, markets, and private label. It changes gross margin, cash timing, marketing spend, and fulfillment load. For direct-to-consumer sales, first-year digital marketing can run 60% of revenue and platform plus payment fees another 25%, so price stays stronger, but cash can get tight fast.

The key inputs are orders by channel, average selling price, discounts, freight, fees, and labor. Owner take-home improves only when each added order still leaves contribution after those costs. Wholesale or retail can lift volume, but slower payment and extra handling can erase the gain if the channel mix is not controlled.

Track Contribution by Channel

Measure each channel on a per-order basis, not just on sales. Here’s the quick math: $100 in DTC revenue can lose $60 to digital marketing and $25 to platform and payment fees before freight or labor. Compare that with wholesale, retail, subscriptions, and market sales using the same cost buckets.

Test one change at a time. Use subscriptions to steady cash, use bundles to raise average order value, and use private label only if the extra volume still covers lower price and added handling. If a channel does not pay for discounts, freight, fees, and labor, it helps revenue but not owner income.

1

Gross Margin Per Unit

Gross Margin Per Unit

Herbal tea gross margin is the first filter before owner pay. On the provided model, $835,000 in revenue produces $743,575 of gross profit, or about 89.0% gross margin before overhead. That only works if unit COGS stay close to the stated $185 to $210 for herbs, spices, tins, sachets, boxes, and direct blending labor.

Here’s the quick math: gross margin per unit equals selling price minus unit COGS, then minus any revenue-linked production cost. A 25% production cost load, plus packaging upgrades, organic premiums, shrink, or freight bumps, cuts the cash left for payroll, reserves, and owner distributions. That’s why margin loss hits take-home income fast.

Track unit margin before owner pay

Track gross margin by blend, package, and order type. Use selling price, unit COGS of $185 to $210, the 25% production cost load, shrink, and freight as your core inputs. If a nicer tin or organic claim lifts cost faster than price, owner pay drops even if revenue grows.

Review margin by SKU monthly

Split freight from ingredient cost

Price upgrades before adding them

Hold cash for payroll and reserves

What this estimate hides is timing. If ingredients or packaging are bought before the tea sells, cash leaves early, so thin margin feels worse than the P&L shows. Keep a simple forecast for units sold, unit COGS, and gross profit so you know when distributions are actually safe.

2

Production Scale And Capacity

Production Scale And Capacity

This driver is about how many herbal tea units the plant can make and sell without breaking quality or cash. Volume rises from 36,000 units in year one to 138,000 units in year five, while fixed overhead stays at $73,200. That pushes overhead per unit down from about $2.03 to $0.53, which can raise owner profit if sales keep pace.

Here’s the catch: scaling only helps when demand, quality control, inventory turns, labor scheduling, and cash flow keep up. If output outruns sales or a bad batch hits, the owner still pays the same overhead and may have less cash for pay or distributions.

Track Output Before You Add Volume

Measure units produced, units sold, reject rate, labor hours, and days inventory on hand. Use the fixed overhead base of $73,200 to test how each added unit lowers cost per unit and improves the cash left for the owner.

Watch batch yield and scrap daily.

Match labor to forecasted orders.

Keep inventory turns moving.

Hold cash for herb and packaging buys.

Before pushing volume, confirm the team can ship the next step up without missed checks or stockouts. If production runs ahead of sales, the owner funds inventory instead of taking home profit.

3

Pricing And Product Mix

Pricing And Product Mix

Pricing and product mix set how much cash each tea order brings in before marketing and fulfillment. In year 1, unit prices range from $2,100 to $2,600, with a $2,319 weighted average. By year 5, the range rises to $2,300 to $2,800. If the mix shifts toward premium blends, bundles, and subscriptions, average order value rises and more revenue stays available for owner pay.

Here’s the quick math: higher-priced gift sets, seasonal collections, and bulk packs can lift margin, but only if discounts, packaging, and compliance costs stay in line. Avoid unsupported health claims, because that can force price cuts or legal cleanup. One clean rule: price the story, not just the leaf.

Measure Mix Before You Price

Track units sold, average order value, discount rate, and contribution margin by product type. You need those inputs to see whether a bundle or premium blend really adds profit after packaging, shipping, and fees. A higher ticket that adds no margin does not help the owner’s draw.

Test mix changes in small steps: premium blends, subscriptions, gift sets, and bulk packs. Watch which offers raise cash per order without pushing return risk or compliance risk higher. If a $2,600 unit sells slowly, but a $2,319 weighted mix turns faster, the faster seller may fund payroll and reserves better.

Track price by SKU.

Compare margin by bundle.

Measure repeat purchase rate.

Log packaging cost per unit.

Review claims before launch.

4

Customer Acquisition And Repeat Purchase

Repeat Purchase and Customer Acquisition

Repeat purchase and customer acquisition cost decide how much herbal tea revenue turns into owner pay. Using the stated assumptions, digital marketing is 60% of revenue, or $50,100 on $835,000 sales, and platform and payment fees add 25%, or $20,875. By year five, those rates fall to 30% and 15%, so the owner keeps more cash only if email, reviews, subscriptions, and owned channels lower paid spend per order after fulfillment and fees.

Measure CAC and Repeat Rate

Track new customers, repeat purchase rate, average order value, CAC (customer acquisition cost), and fee per order. If one new order costs more than its contribution after fulfillment, discounts, and fees, it hurts owner income even when sales rise. Use email flows, review requests, bundles, and subscriptions to shift demand toward owned channels and reduce paid traffic dependence.

5

Owner Role And Cash Reserves

Owner Pay vs Cash Reserves

Owner income here comes from the split between wages for labor and profit draws from cash left after operations. If the owner blends, packages, sells, handles compliance, and manages the business, payroll stays lower, but capacity tops out at one person’s hours. Hiring can grow output, but only if added labor creates more gross profit than it costs.

Cash reserves also cut into what can be paid out. The business must keep cash for herbs, packaging, inventory, quality control, and seasonal demand, so not all profit is distributable. On $835,000 of first-year revenue, reported gross profit is $743,575, but the owner still needs a cash buffer before taking a draw.

Separate Pay, Profit, and Reserve Cash

Track owner hours by task and put a value on each one: blending, packaging, sales, compliance, and management. If the owner is doing work a staffer or vendor could do, convert that time into a paid role only when the added output covers the extra payroll. Keep owner wage and profit draw separate.

Set a reserve rule before paying distributions. Hold cash for the next herb purchase, packaging run, quality checks, and seasonal spikes, then pay the owner only from excess cash after those needs are covered. If owner pay forces delayed buying or extra borrowing, reserves are too thin and take-home income is overstated.

6

Compare lean, base, and growth owner-income scenarios

Owner income scenarios

Owner income moves with unit volume, price, and fixed overhead. These cases show how much cash can reach the owner before reserves, taxes, debt payments, and reinvestment.

Lean, base, and upside owner take-home cases.

Scenario

Low CaseLean case

Base CaseBase case

High CaseUpside case

Launch model

This is the lean case built on first-year volume and pricing.

This is the modeled middle case built on third-year scale.

This is the stronger case built on fifth-year scale and fuller capacity use.

Typical setup

First-year operations at 36,000 units, $835,000 revenue, 890% gross margin, and $73,200 fixed overhead.

Third-year operations at 81,000 units, $196 million revenue, 894% gross margin, and $155 million operating profit before owner pay.

Fifth-year operations at 138,000 units, $348 million revenue, 897% gross margin, and $289 million operating profit before owner pay.

Cost drivers

First-year volume

fixed overhead

raw material cost

packaging costs

marketing spend

Third-year scale

price mix

overhead spread

marketing efficiency

production use

Fifth-year scale

strongest unit volume

better price mix

overhead dilution

lower fee drag

Owner income rangeBefore owner reserves

$599,400 before reservesLow income

$155M before reservesCore income

$289M before reservesUpside income

Best fit

Use this to stress-test cash if sales start slow or costs stay sticky.

Use this as the main planning case for budgets, hiring, and cash needs.

Use this to test upside if demand, pricing, and throughput all land well.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.