How Much House Sitting Service Owners Make At $100 Per Booking

A house sitting service owner can start paying themselves only after bookings cover direct costs, marketing, fixed overhead, and reserves In the researched first-year model, weighted customer booking value is $635, service revenue is $10025 per order, and contribution margin is 855% before marketing and fixed costs Known fixed overhead is at least $5,000 per month, and first-year acquisition spend is $125,000, so break-even is about 180 orders per month before owner pay and taxes These are planning assumptions, not salary promises or tax advice

Owner income$10.0kNet margin15.8%Revenue for target pay$63.5kBusiness difficultyHard

What drives house sitting owner income?

1

Pricing Mix

$635

Year 1 weighted AOV is about $635, so even small price gains lift each commission check and improve owner take-home.

2

Booking Fill

86%

Filled bookings keep about 85.5% of revenue after variable costs, so empty nights and cancellations hit profit fast.

3

Add-ons

10%-25%

Premium and special-needs jobs rise from 10% to 25% of seller mix by Year 5, which lifts ticket size without a matching jump in fixed cost.

4

Repeat Clients

20%-40%

Short-trip repeat rate doubles from 0.20 to 0.40 by Year 5, which spreads the Year 1 acquisition spend across more revenue.

5

Cost Control

$5.6K/mo

Office, tools, legal, utilities, admin, and marketing software total about $5.6k a month, so waste cuts flow straight to EBITDA.

6

Sitter Leverage

4 FTE

Support, engineering, and ops scale to 4 FTE later, so owner income depends on adding labor only when each hire drives more bookings than they cost.

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This output is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. It excludes taxes, benefits, debt payments, and guaranteed distributions unless you enter them.

Want to see the full forecast for House Sitting Service?

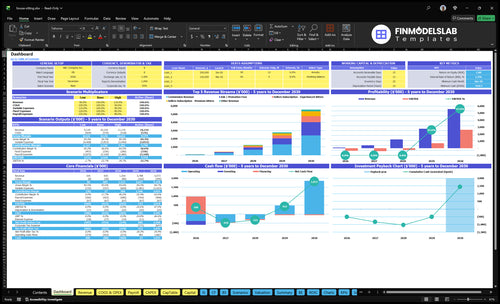

The House Sitting Service Financial Model Template dashboard shows revenue, gross margin, contribution margin, fixed costs, acquisition spend, reserves, and owner compensation. Open the model.

Owner-income model highlights

Trip mix: $300, $1,200, $500

$5 fixed, 15% variable

Break-even, take-home, runway

Charts, tables, sensitivity

What costs reduce house sitting owner income?

If you’re pricing a House Sitting Service, the biggest income drains are customer support at 40% of revenue, sitter vetting and background checks at 30%, payment gateway fees at 25%, platform insurance at 20%, and hosting at 30% in Year 1. For setup context, see How Much Does It Cost To Open A House Sitting Service Business?; fixed overhead adds $5,000/month, and Year 1 acquisition spend is $125,000.

Main income drains

40% customer support

30% sitter vetting

25% payment gateway fees

20% platform insurance

Year 1 drag

30% hosting cost in Year 1

$5,000 monthly fixed overhead

$125,000 acquisition spend in Year 1

Add mileage, licenses, bonding, reserves

Can you make a living house sitting?

Yes, you can make a living with a House Sitting Service, but only if paid booking volume clears overhead and your capacity limit; start by tracking What Is The Main Measure Of Success For Your House Sitting Service?. Here’s the quick math: at $100.25 revenue per order and $85.71 contribution per order, $5,000 in monthly fixed costs needs about 59 orders/month; with first-year acquisition spend included, break-even rises to about 180 orders/month.

What works

Push premium pet care bookings

Build repeat client volume

Keep sitter quality high

Track orders per month

What limits pay

One owner, one home

Add sitters to scale

No salary is guaranteed

Marketing can reset break-even

How much revenue does a house sitting business need?

A House Sitting Service needs about $15,417 in monthly contribution before owner pay, based on $5,000 fixed overhead and $10,417 in monthly acquisition spend. That works out to roughly 180 orders per month, and slow travel months plus cancellations can push the target higher.

Monthly target

$15,417 monthly contribution needed

$5,000 fixed overhead

$10,417 acquisition spend

Owner pay sits after that

Volume drivers

Target about 180 orders monthly

Seasonality raises the bar

Cancellations cut realized revenue

Peak travel months help fill gaps

Key Takeaways

Pricing drives revenue, but only if demand holds.

About 59 monthly orders cover fixed overhead.

Add-ons and repeats raise value without extra churn.

Hiring sitters boosts scale but weakens margin control.

Compare lean, base, and high owner income scenarios

Owner income scenarios

Owner pay moves fast with order volume because commission revenue has high contribution, but payroll, marketing, and acquisition spend can still hold cash back.

Low, base, and high cases show how order volume changes owner pay.

Scenario

Low CasePart-time

Base CaseFull-time

High CaseTeam-based

Launch model

Volume stays below break-even, so owner pay is limited or paused.

Order volume reaches about 180 a month, which covers core costs before owner pay.

Volume moves above break-even and leaves room for reserves, staff, and owner pay.

Typical setup

The business runs under the base volume, so contribution mostly covers fixed payroll and acquisition spend.

Volume lands near 180 orders a month, so the business covers core costs before owner pay.

Volume stays above 180 orders a month and the business can support a larger team and cash buffer.

Cost drivers

Below break-even orders

85.5% contribution margin

$5,000 monthly fixed overhead

$125,000 Year 1 acquisition spend

owner draw deferred

About 180 orders/month

85.5% contribution margin

$5,000 monthly fixed overhead

$125,000 Year 1 acquisition spend

tight owner pay

Above 180 orders/month

lower CAC over time

premium and extended stays

reserve cash for staff

owner pay can scale

Owner income rangeBefore owner reserves

No owner payPart-time fit

Thin owner payFull-time fit

Owner pay plus reservesTeam-based fit

Best fit

Use this to test a lean solo setup with weak demand.

Use this as the main planning case for a steady owner wage with tight cost control.

Use this only if you are planning a larger ops team and want to stress-test upside.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

House Sitting Service Core Six Income Drivers

Average house sitting pricing

Pricing per booking

Pricing is the main revenue lever. In Year 1, short trips average $300, extended stays $1,200, and special-needs stays $500. The weighted AOV is $635, so the trip mix matters as much as the sticker price. Higher rates only work when pet care complexity, home security needs, location, reviews, and service quality support them.

Here’s the quick math: the model uses $5 plus 15% and shows service revenue of $10,025 per order. What this hides is demand risk: if higher pricing cuts booked nights, take-home can fall even when AOV rises.

Price by trip type

Track bookings by short trip, extended stay, and special-needs work, then test price changes one segment at a time. The inputs that matter are trip mix, base fee, the 15% uplift, and the work behind the stay: pet care, home security, location, and reviews.

Watch close rate after price changes.

Compare booked nights, not just AOV.

Document service scope before quoting.

If a higher rate lifts AOV but lowers nights, owner pay can still drop. The best price protects both margin and occupancy.

Operating cost control

Operating Cost Control

When direct and variable costs run hot, owner pay shrinks fast. The model says Year 1 direct and variable costs are 145% of revenue, so every booking has to be watched against pay fees, support, mileage, insurance, and supplies. That cost mix hits cash flow before the owner can take profit.

The fixed load is $5,000 per month. If the travel radius stays tight and repeat clients cut admin and mileage, margin holds better; if not, the same revenue can still leave very little for the owner.

Cut Cost Drag

Track cost per booking, mileage per sit, support time, and insurance reserve levels. Here’s the quick math: fixed overhead of $5,000 must be covered before the owner sees real pay, so small leaks in payment fees, software, legal, or admin matter fast.

Keep the service area narrow, push repeat clients, and review background check, insurance, and supply spend every month. Underfunded insurance or reserves can turn one claim into a much larger loss later.

Pet care and home-care add-ons

Pet and home-care add-ons

Pet and home-care add-ons lift average booking value when they reflect real work, not padding. In this model, special-needs bookings are $500 in Year 1 and stay at 10% of buyer mix, so even a small share can move revenue. The key inputs are booking volume, add-on price, and the extra labor or check-in time each request creates.

Multiple pets

Medication

Special feeding routines

Plant care

Pool checks

Mail handling

Extended monitoring

Here’s the quick math: every add-on should pay for the extra time it creates. If the fee covers the added work, it raises revenue and owner draw; if it does not, it cuts margin and ties up support. Simple packages book faster, while too many fee lines can slow conversion and raise admin cost.

Price the extra work cleanly

Track attach rate by add-on type, meaning how often buyers choose it. Then compare added revenue per booking against the extra minutes of care, messages, and issue handling. If special-needs requests are clustered near 10% of bookings, they need a clear price and a clear scope, or they will quietly eat profit.

Use one short menu and pre-set rules for each add-on. That makes quoting faster, helps buyers understand what they are buying, and keeps support time down. For the owner, the goal is simple: more paid work per booking, with no surprise labor that drags down cash flow or pushes profit below the level needed to pay yourself well.

Booked nights and order volume

Booked Nights and Orders

Utilization is the income switch here: more booked nights or orders turn pricing into cash. The model should use booked nights or orders as a user input, since the source does not give a direct volume figure. At $8,571 contribution per Year 1 order, volume drives owner pay more than price alone.

Here’s the quick math: about 59 orders per month covers $5,000 of known fixed overhead, and about 180 orders per month covers fixed overhead plus first-year acquisition spend. A full calendar at low rates can still leave weak take-home if cancellations, gaps, or slow seasons cut the actual stay count.

Track Nights, Not Just Leads

Measure filled nights, booking count, cancellation rate, and seasonal gaps by market. If nights rise but cancellations also rise, cash flow stays thin and owner draw stays shaky. The key is usable occupancy, not inquiry volume. One clean rule: a booked calendar only helps if it actually closes and stays on the books.

Watch the mix of short trips, long stays, and special-needs jobs, because each one changes realized contribution. If volume is light, push repeat clients and referrals before adding more spend. If fixed overhead is $5,000 per month, forecast owner pay from booked orders only, then stress test slow months so you do not overdraw in low season.

Owner capacity versus hired sitters

Owner Capacity vs. Hired Sitters

A solo owner gives tight control, but it also caps income because one person can stay in one home at a time. So revenue depends on booked nights the owner can physically cover, not just demand. When the business adds sitters, gross revenue can grow faster, but take-home pay can shrink if sitter pay, support, and quality control rise faster than booking volume.

The model shifts from 60% casual and 10% premium in Year 1 to 25% casual and 25% premium by Year 5. That mix can widen capacity, but it also adds recruiting, vetting, scheduling, check-ins, insurance review, and contractor or payroll cost. The key metric is gross profit per booked night after sitter cost.

Scale Capacity Without Losing Margin

Track booked nights per sitter, sitter pay rate, support time, and cancellation rate. Here’s the quick math: if more sitters do not lift nights enough to cover added labor and admin, owner pay falls even when top-line revenue grows. A solo model is simpler; a multi-sitter model needs tighter controls.

Set pay before recruiting.

Vet sitters before activation.

Review insurance with each hire.

Monitor quality after every stay.

Use a weekly dashboard for fill rate, sitter mix, and gross margin. If scheduling gaps or rework rise, the business may add revenue but still miss cash for the owner’s draw.

Repeat clients and referrals

Repeat Clients and Referrals

Repeat bookings turn one paid client into several paid stays. In Year 1, buyer CAC is $100 and seller CAC is $150, so every return booking cuts marketing waste and helps cash flow. Repeat assumptions rise from 20% to 40% for short trips, 5% to 13% for extended stays, and 10% to 20% for special needs.

This driver depends on trusted sitters, strong reviews, pet familiarity, and clear check-in routines. Track repeat rate by trip type, referral share, and churn after the first stay. One clean handoff can be worth more than a discount. If return bookings slip, the calendar gets patchy and owner pay gets less steady.

Track Return Rate by Stay Type

Measure repeat rate separately for short trips, extended stays, and special needs, then compare it to the CAC you paid to win that client. If a booking brings referrals, count those too, because they usually cost less to acquire and close faster. Keep booking notes and check-in steps consistent so the same client can rebook without friction.

To improve it, document sitter profiles, pet routines, and message templates. Ask for reviews right after each stay, since reviews raise trust and help the next booking convert. A simple routine usually beats more marketing spend when the goal is higher margin and a steadier owner draw.