Owner incomeNear $0

Owner incomeNear $0Immersive Escape Room Owner Income, Explained

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner incomeNear $0  Net margin-29% to 39%

Net margin-29% to 39% Revenue for target pay$620K+

Revenue for target pay$620K+ Business difficultyHard

Business difficultyHard

Escape room owner income can be $0 in the early ramp-up and rise materially once bookings cover payroll, rent, marketing, and room upkeep In these researched assumptions, the business posts -$110K EBITDA in Year 1, reaches breakeven around Month 25, and reaches $510K EBITDA in Year 5 That EBITDA is not guaranteed owner pay Debt, reserves, taxes, and reinvestment can reduce the owner’s actual take-home

Owner incomeNear $0Net margin-29% to 39%Revenue for target pay$620K+Business difficultyHardWant to test your own escape room pay scenario?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margin, payroll, taxes, debt, reserves, and reinvestment. It is not guaranteed salary, tax advice, or owner distribution advice.

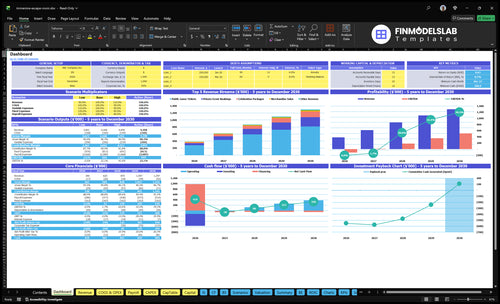

Want to check owner income in the Immersive Escape Room model?

The dashboard shows revenue, margin, costs, reserves, and owner take-home assumptions in the Immersive Escape Room Financial Model Template—open it.

Owner-income model highlights

- Operating profit, draw capacity

- Reinvestment, cash runway

- Revenue climbs $3.845M to $130M

- EBITDA rises -$110K to $510K

- Breakeven, cash need, payback

- Tickets, payroll, capex assumptions

Does adding more escape rooms increase owner income?

Immersive Escape Room can earn more from added rooms only if the extra capacity fills the same rent, front desk, and marketing spend better. Here’s the quick math: a second room can lift revenue per fixed cost, but it also adds reset labor, maintenance, and refresh work. A second location is a bigger bet, with $440K in initial capex, including $150K leasehold improvements, two $80K rooms, $60K technology, and other launch assets, so test the scenario before signing another lease.

One venue first

- Spread fixed rent across more tickets

- Use front desk once, not twice

- Use one marketing budget better

- Add reset labor and upkeep

Second site risk

- Add new rent and payroll

- Pay launch marketing again

- Take buildout risk up front

- Test demand before new lease

What affects escape room profit margin the most?

Gross margin is the first thing to watch in an Immersive Escape Room: it’s squeezed by consumables, prop refresh, merchandise cost, payment processing, and digital marketing, while operating margin is hit by payroll and rent. If you want the launch cost side first, see What Is The Estimated Cost To Open And Launch Your Immersive Escape Room Business? The quick takeaway: marketing falls from 50% in Year 1 to 30% in Year 5, prop refresh drops from 30% to 22%, payroll rises from $2,475K to $3,925K, and rent stays fixed at $10K/month.

Gross margin drivers

- Consumables cut ticket profit fast.

- Prop refresh eats margin over time.

- Merchandise cost lowers add-on profit.

- Payment processing takes a fee on sales.

Operating margin drivers

- Payroll is the biggest swing factor.

- Rent stays fixed at $10K/month.

- Booked slots must match staffing.

- Utilization gains raise owner take-home.

Can you make a living owning an escape room?

Yes, you can make a living owning an Immersive Escape Room, but usually not from day one; under these assumptions, Year 1 EBITDA is -$110K, breakeven lands around Month 25, and What Is The Most Critical Metric To Measure The Success Of Immersive Escape Room Experiences? comes down to booking density. By Year 3, EBITDA reaches $179K, which may support full-time owner income if debt, cash reserves, and room refresh budgets stay controlled.

Owner Pay Reality

- Year 1 EBITDA: -$110K

- Breakeven: around Month 25

- Owner labor lowers cash burn

- Unpaid labor is not true profit

Income Conditions

- Year 3 EBITDA: $179K

- General manager salary: $70K

- Game master payroll still applies

- Full-time pay needs dense bookings

Want the six main escape room income drivers?

1

$368K-$1.25MBooking Utilization

Filling more public tickets, private bookings, and celebration packages is the biggest swing in owner income, and it helps push EBITDA from -$110K in Year 1 to $510K in Year 5.

2

$35-$39Ticket Yield

A higher ticket price drops straight to profit because the room is already built, and private events at $400 to $480 and celebration packages at $550 to $650 add more upside.

3

21KVenue Capacity

More usable slots let you scale public tickets to 21,000 a year by Year 5, which lifts revenue without matching fixed-cost growth.

4

$248K-$393KPayroll Efficiency

Payroll is the biggest controllable cost block, so staffing moves matter fast when annual wages run from about $247.5K to $392.5K.

5

$10K/moOccupancy Costs

The $10,000 rent line sets a hard floor, and utility, insurance, and security costs still sit there before any owner draw, debt, or reserve build.

6

2.2%-3.0%Refresh Discipline

Keeping prop refresh tight protects margin on every sold ticket and event, so small waste here shows up fast in take-home cash.

Immersive Escape Room Core Six Income Drivers

Booking utilization

Booking Utilization

Booking utilization is how many game slots, public tickets, and private events you sell out of the slots you open. When utilization rises, revenue grows faster than rent and other fixed costs, so more of each extra booking turns into owner income instead of just covering overhead. One clean measure is revenue per available game slot, which shows how well open time turns into cash.

The scale-up here is strong: volume moves from 8,000 public tickets and 150 events in Year 1 to 21,000 tickets and 550 events in Year 5. That is about 2.6x more tickets and 3.7x more events. The risk is staffing too many shifts before demand arrives, because empty slots still carry labor and fixed costs.

Track Fill Before You Add Shifts

Here’s the quick math: if bookings rise while fixed costs stay mostly flat, owner draw improves fast. Track booked game slots, public ticket volume, private event count, and revenue per available game slot every week. If a slot stays open, it should be rare, not routine. Empty prime-time slots hurt cash flow because they do not reduce rent or core staffing.

- Count sold slots by daypart.

- Separate public and event bookings.

- Watch revenue per open slot.

- Delay shifts until demand holds.

What this estimate hides: labor can rise before bookings do. So use a staffing plan tied to confirmed demand, not hope. If demand is still thin, keep more hours flexible and push corporate events, weekends, and peak-time sales first. That protects margin and helps the owner pay themselves sooner.

1

Ticket yield

Ticket Yield

Ticket yield is the revenue you get per booking after you blend public tickets, private events, and celebration packages. In this model, public pricing moves from $35 to $39, private events from $400 to $480, and celebrations from $550 to $650. If utilization holds, higher yield lifts revenue, gross profit, and the cash available for owner pay.

Here’s the quick math: a 11.4% increase on public tickets, 20% on private events, and 18.2% on celebrations can add meaningful revenue without adding rooms or staff. But if local buyers push back and bookings fall, the gain disappears fast. The real test is whether higher pricing keeps slots full.

Raise Yield Without Losing Bookings

Track yield by booking type, not just total sales. Measure revenue per session, average players per booking, and the mix of public, private, and celebration sales. Premium themes can support higher prices, but only if conversion and utilization stay steady. One clean rule: raise price only when sold-out slots and waitlist demand show up together.

- Watch revenue per booked slot weekly.

- Test price by day and time.

- Protect peak slots from discounting.

- Compare conversion before and after hikes.

If a price increase lifts yield but drops occupancy, owner income can fall because fixed costs stay in place. If price rises and booking volume holds, the extra margin flows through to profit and draw. That is the whole game here: more dollars per session, not fewer sessions sold.

2

Venue capacity

Venue Capacity

Venue capacity is the hard ceiling on sales: how many room slots you can actually sell and run. For this model, the start point is two initial room builds at $80K each, so capacity grows only if throughput — the number of paid groups you move through each day — stays high on weekends, holidays, and corporate booking windows.

The inputs are simple: room count, game slots, session length, reset time, and operating hours. More slots can lift revenue, but staffing and technical support have to keep pace. If added slots do not sell, the owner carries higher fixed effort without higher take-home pay.

Capacity Planning Tip

Track booked slots per room, peak-day sellout rate, and unfilled weekend capacity. The quick test is whether the extra room can be filled often enough to justify the added operating load. If demand is strongest in corporate booking windows, protect those slots first and avoid overbuilding before the calendar proves demand.

- Measure sold vs. open slots weekly.

- Staff to peak demand, not average demand.

- Map reset time to lost sellable hours.

- Protect weekends and holiday inventory first.

3

Payroll efficiency

Payroll Efficiency

Payroll efficiency is the gap between booked hours and paid labor. In Year 1, payroll is $2,475K, including a $70K general manager, a $50K lead game master, two game masters, and part-time support. By Year 5, payroll rises to $3,925K, so staffing growth has to match slot volume or owner pay gets squeezed.

The key inputs are room count, weekly bookings, event mix, operating hours, and owner shifts. Unpaid owner labor can protect cash flow, but it is still labor, not pure profit. Here’s the quick math: if paid staff hours grow faster than revenue per available game slot, take-home income falls fast, and overstaffing becomes the biggest margin risk.

Staff to Demand, Not Hope

Track labor against booked sessions, private events, and peak-hour volume. Compare payroll by shift to revenue by room, then cut idle time before adding headcount. Use the general manager and lead game master where they improve sales, resets, or guest flow. One rule: staff to demand, not to wishful forecasts.

Test part-time coverage first for weekends and corporate windows. Build each week’s schedule from actual bookings, then watch idle time, reset speed, and overtime. If owner shifts cover slow periods, treat that as a temporary cash fix, not permanent margin. The goal is simple: keep paid labor lined up with slots sold.

4

Fixed occupancy costs

Fixed occupancy costs

Rent and fixed overhead set the monthly booking hurdle. Here, commercial rent is $10K per month, and total fixed occupancy costs are stated at about $13.55K per month, including utilities, insurance, office supplies, software, cleaning, and security monitoring. Those bills stay due even when bookings slow, so owner income only starts after the business clears that fixed base.

The quick math is simple: fixed costs / contribution per booking = break-even bookings. If local demand can’t suppo rt enough sessions, cash flow gets squeezed fast and owner draws get delayed. This is the main risk in a lease-heavy model like an immersive escape room: strong demand can cover the space, but weak demand still leaves the same monthly bill.

Track the lease break-even

Build the forecast from the ground up: monthly rent, fixed overhead, then booked game slots and private events. Measure how much each session adds after variable costs, because that tells you how many bookings the venue needs before the owner can pay themselves. If the market can’t cover $13.55K monthly, the lease is too big for current demand.

Keep the space tied to local demand, not hope. Watch weekday fill rates, corporate event volume, and slow-season gaps, then test pricing or promotions before adding space. If occupancy stays low, cut fixed costs early, because every unused month burns cash and pushes break-even, taxes, and owner pay farther out.

- Track booked slots every week.

- Compare demand to fixed bills.

- Renegotiate before cash gets tight.

5

Refresh and reinvestment discipline

Refresh reserve discipline

Prop replacement, tech repairs, puzzle refreshes, and new storylines are not optional in an immersive escape room. The model sets this spend at 30% of revenue in Year 1, easing to 22% by Year 5. That reserve cuts distributable cash, but it protects repeat demand, reviews, and referrals. One stale room can look cheap on paper and still hurt bookings.

Here’s the quick math: if annual revenue is $500,000, a 30% refresh budget means $150,000 kept back in Year 1; at 22%, that falls to $110,000 by Year 5. The key inputs are ticket sales, private events, consumables, repair calls, and how often puzzles or storylines need replacement. Ignore this line and owner pay may rise short term, then drop when guests stop coming back.

Protect repeat demand

Track refresh spend as a percent of revenue, plus prop loss, tech downtime, and room review trends. Set a monthly reserve from each booking, not a leftover amount at month-end. That keeps cash ready for broken locks, worn props, and puzzle resets before guests notice. The goal is simple: keep rooms feeling new without letting emergency fixes eat margin.

Use a refresh calendar tied to game volume, and log every replacement by room. If a room gets heavy repeat traffic, refresh it first so weak reviews do not drag down future bookings. The owner’s take-home income improves when reserve spending stays planned and the room stays sellable, instead of saving cash today and paying for lost demand later.

6

Compare lean, base, and high escape room owner income scenarios

Owner income scenarios

Owner income moves with ticket volume, event mix, and staffing load. A lean launch can run at a loss, while a mature venue can support draws after reserves and debt service.

| Scenario | Low CaseLean case | Base CaseBase case | High CaseUpside case |

|---|---|---|---|

| Launch model | This is the lean launch path, with Year 1-style revenue of about $384.5K and EBITDA around -$110K. | This is the modeled middle path, with Year 3-style revenue of about $870K and EBITDA around $179K before debt, reserves, and owner pay. | This is the stronger maturity path, with Year 5-style revenue of about $1.30M and EBITDA around $510K before deductions. |

| Typical setup | Public games and add-ons are still ramping, while fixed rent and payroll keep the business under pressure. | The venue has steadier public games, more private events, and enough volume to cover core labor and overhead. | Dense demand, higher pricing, and tight staffing leave more room for owner pay and reinvestment. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | No planned drawNo draw | Modest draw possibleDraw possible | Higher draw capacityHigher draw |

| Best fit | Best for launch planning and downside testing. | Best for a stable single venue with steady demand. | Best for dense demand and disciplined staffing. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Immersive Escape Room Porter's Five Forces Analysis

- Immersive Escape Room BCG Matrix

- Immersive Escape Room Business Model Canvas

- Tracking 7 Core KPIs for Immersive Escape Room Success

- Immersive Escape Room Business Plan Template in Pre-Written Word

- Boost Immersive Escape Room Margins with 7 Financial Strategies

- How Much Does It Cost To Run An Immersive Escape Room Monthly?

- Immersive Escape Room Startup Costs: $801K Opening Budget

- Immersive Escape Room Financial Model Template in Excel

- How To Open An Immersive Escape Room In 4 To 8 Months

- How to Write an Immersive Escape Room Business Plan: 7 Steps

- Immersive Escape Room Marketing Mix

- Immersive Escape Room Marketing Plan

- Immersive Escape Room Business Proposal

- Immersive Escape Room PESTEL Analysis

- Immersive Escape Room Pitch Deck Example Editable PPTX

- Immersive Escape Room Business SWOT Analysis

- Immersive Escape Room Value Proposition Canvas

Frequently Asked Questions

Owner take-home can be $0 during ramp-up and may rise after bookings cover costs In this model, EBITDA is -$110K in Year 1, $179K in Year 3, and $510K in Year 5 Actual owner pay comes after debt service, reserves, reinvestment, and personal taxes