International Freight Forwarding Owner Income: $202K Year 1 Before Payroll

You’re estimating owner pay from a US business that arranges international shipments for client companies Using the provided first-year assumptions, the model shows $699,775 in retained revenue and about $202,000 before payroll, income taxes, debt service, and reserves

Owner income$202KNet margin16.2%Revenue for target pay$1.25MBusiness difficultyHard

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from monthly revenue, gross margin, labor, fixed costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. It excludes startup CAPEX and one-time opening costs.

Want the six drivers that move owner income?

1

Shipment Volume

31-542/mo

More shipments spread fixed labor and software over more jobs, so owner take-home improves fastest as volume moves from 31 to 542 orders a month.

2

Gross Profit

$213/ord

At about $213 of Year 1 commission revenue per order, every extra shipment adds real contribution before overhead.

3

Customer Mix

30%-50%

E-commerce brands rise from 30% to 50% of buyers, and their higher repeat rate supports better lifetime value and lower CAC payback.

4

Ticket Mix

$2.5K-$17K

Moving toward larger shippers lifts revenue per job because Enterprise Shippers carry far bigger order values than SMB importers.

5

Overhead Burn

$122K/mo

Fixed overhead plus acquisition marketing keeps cash tight early, so the model must clear the Month 17 breakeven point before draws start to feel safe.

6

Cash Reserve

$48K

Minimum cash falls to $48K in Month 16 and payback takes 32 months, so reserves come before owner distributions.

Want to see how owner income changes in the full forecast?

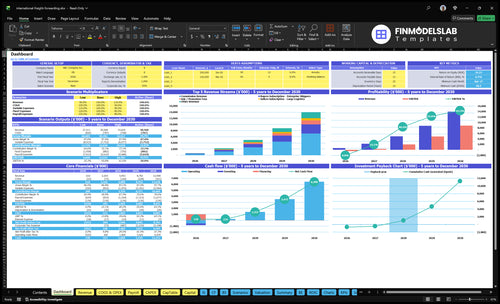

The screenshot shows how owner income flows from revenue, order volume, contribution, and operating costs in the International Freight Forwarding Financial Model Template; the owner pool tabs also test buyer acquisition, seller acquisition, mix, repeat orders, average order value, commissions, subscriptions, extra fees, fixed expenses, and variable expenses, with Year 1, Year 3, and Year 5 charts showing $6998K, $393M, and $1030M retained revenue before unmodeled payroll and reserves. Open the model to check the base case.

Owner-income model highlights

Owner pool drives take-home

Revenue and margin flow

Scenario tests by year

How much revenue does a freight forwarding business need to pay the owner?

For International Freight Forwarding, the owner is paid from retained revenue, not from customer freight value. The first-year break-even before payroll and reserves is about $464K in retained revenue, based on $396K of known operating costs divided by a 85.5% contribution margin, and the modeled ~$202K owner pool needs about $700K retained revenue. A $5,000 order does not create $5,000 of income; under the commission model it keeps only $175 before other revenue streams.

Break-even math

$396K known operating costs

85.5% contribution margin

$464K break-even revenue

Before payroll and reserves

Owner payout math

$700K retained revenue target

~$202K modeled owner pool

$175 kept on a $5,000 order

Commission: $25 plus 30%

Can a freight forwarding owner make more by scaling shipments?

Yes—if International Freight Forwarding keeps service quality and documentation accuracy tight, more shipments can lift retained revenue as volume grows from 31 orders/month in Year 1 to 186 in Year 3 and 542 in Year 5. But owner pay can lag because hiring coordinators, sales staff, compliance support, and finance help raises overhead before the scale pays back. Compliance mistakes, disputes, and slow receivables can erase the benefit fast.

Scale upside

31 orders/month in Year 1

186 orders/month in Year 3

542 orders/month in Year 5

Retained revenue rises from $6998K to $1030M

Key risks

Overhead rises before owner pay

Hiring adds cost early

Compliance errors kill margin

Slow receivables hurt cash flow

What affects freight forwarding profit margins?

Margins in International Freight Forwarding come down to the gap between carrier buy rates and shipper sell rates, then the add-ons: agent charges, destination charges, documentation, compliance, insurance, software, support labor, sales spend, and credit losses. If you're sizing the launch side, see What Is The Estimated Cost To Open And Launch Your International Freight Forwarding Business?; at the model level, 15% transaction processing, 20% cloud hosting, 80% variable sales and marketing, 30% operational support, $2K/month legal and compliance, $700/month insurance, and $15K/month software each cut owner take-home unless volume or retained revenue rises.

Where margin leaks

Carrier rate spread drives gross margin.

Agent charges and destination fees stack fast.

Documentation and compliance add labor.

Credit losses can erase thin deals.

Cost lines to watch

15% transaction processing hits each payment.

20% cloud hosting rises with usage.

80% variable sales and marketing can outrun growth.

30% operational support, plus $2K legal, $700 insurance, and $15K software, press take-home.

Key Takeaways

More shipments raise revenue only after capacity is covered.

Higher commission per order improves owner pay fast.

Repeat customers make cash flow easier to forecast.

Reserve cash before paying owner distributions.

Compare low, base, and high owner income scenarios

Owner income scenarios

Owner income shifts with order volume, retained revenue, and how much marketing it takes to win and keep accounts. These are planning cases, not guarantees.

Compare low, base, and high owner income cases for freight forwarding.

Scenario

Low CaseDownside case

Base CasePlan case

High CaseUpside case

Launch model

This is the weaker earnings path, where Year 1 order flow stays light and the owner pool remains thin.

This is the modeled case, with mid-cycle volume and a more balanced owner pool.

This is the stronger earnings path, where Year 5 volume and a tighter cost load push the owner pool higher.

Typical setup

Year 1 runs at 31 orders per month with heavy variable costs and $250K of acquisition marketing, so cash left for the owner is tight before payroll and reserves.

Year 3 reaches 186 orders per month with 125% variable costs and $10M of acquisition marketing, which supports a larger pool before payroll and reserves.

Year 5 reaches 542 orders per month with 105% variable costs and $18M of acquisition marketing, which widens the pool before payroll and reserves.

Cost drivers

31 orders/month

145% variable costs

$250K acquisition marketing

Year 1 mix

186 orders/month

125% variable costs

$10M acquisition marketing

Year 3 mix

542 orders/month

105% variable costs

$18M acquisition marketing

Year 5 mix

Owner income rangeBefore owner reserves

$202KOwner pool low

$229MOwner pool base

$728MOwner pool high

Best fit

Use this to stress-test launch months, slow sales ramp, and tighter cash control.

Use this as the main planning case for budgeting and staffing.

Use this to test upside capacity, hiring pace, and how much growth the model can absorb.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

International Freight Forwarding Core Six Income Drivers

Shipment volume

Shipment Volume

Shipment volume is the number of completed orders that actually close and move through the platform. In this model, volume is the first gate to owner pay: at 31 orders/month in Year 1, income is still thin, but by 186 in Year 3 and 542 in Year 5, the same pricing stack can produce far more retained revenue if capacity keeps up.

Here’s the catch: more shipments help only after fixed capacity costs are covered. Each extra order can add commission and may pull in subscription revenue, but documentation errors, service delays, refunds, disputes, and extra support time can eat that gain fast. One clean line: volume without control is just more work.

Track Completed Shipments, Not Just Leads

Measure completed shipments per month, refund rate, dispute rate, and support minutes per shipment. Also track subscription attach rate, because more volume can support more recurring revenue only if service stays smooth. The key inputs are orders closed, average shipment value, commission per shipment, and the cost of fixing errors.

Track completed orders by month.

Flag refunds and disputes fast.

Watch support time per shipment.

Compare volume to capacity weekly.

If volume rises but error rates rise too, owner income can stall even as top-line revenue grows. The goal is simple: push more shipments through the system without adding the same amount of rework, so retained revenue turns into cash the owner can actually take home.

Operating costs and staffing

Fixed Cost Stack

Owner pay is squeezed here because fixed costs get paid before distributions. The disclosed fixed items include $5K rent, $2K legal and compliance, $15K software, $700 insurance, and $1K accounting, or $23.7K/month before other overhead. Known fixed overhead is $122K/month, so most of the cost load sits outside those five lines.

If the Year 1 caveat of variable costs at 145% of revenue holds, every $1 of sales creates $1.45 of variable cost before fixed overhead. That leaves no room for owner distributions until pricing, service mix, or cost structure changes. Hiring can protect service quality, but without payroll data it should be treated as a direct hit to near-term take-home pay.

Keep Overhead Visible

Track fixed overhead by line, then compare it to monthly revenue and gross margin. The key checks are fixed cost as a percent of revenue, variable cost per shipment, and cash left after operating bills. If costs rise faster than shipments, owner pay gets delayed even when sales grow.

Review staffing before hiring.

Model each role’s cash impact.

Keep non-payroll fixed costs visible.

Separate pass-through costs from profit.

One useful test: if new headcount improves service but cuts monthly distributions, decide whether the move protects retention enough to justify the hit. With no payroll figure provided, treat every hire as a margin decision first and an operations decision second.

Gross profit per shipment

Gross profit per shipment

When you look at shipment profit, don’t use the freight invoice as income. The model shows Year 1 commission revenue of $213/order from $25 fixed plus 30% of order value, but a $5,000 order can still produce only $175 commission in the example. Gross profit rises when more value stays after pass-through costs, so owner pay improves only if carrier, support, and exception costs stay tight.

Track retained value per shipment

Measure commission per shipment, pass-through costs, and exception costs separately. Here’s the quick math: if a lane or shipper type adds revenue without adding the same workload, take-home income improves faster than headcount. Confusing invoice value with retained revenue overstates profit and can lead to weak pricing, thin margins, and cash that looks better than it is.

Track gross profit by lane.

Separate fixed and variable fees.

Test higher fee capture.

Watch refunds and support time.

Working capital and reserves

Working capital and reserves

In freight forwarding, profit on paper can still leave the owner short on cash. If carriers or agents must be paid before customers settle, owner distributions can stall even when revenue looks strong. With no reserve percentage, bad debt, receivable days, or carrier payment timing provided, the safe rule is simple: set reserves before owner pay.

This driver includes disputes, chargebacks, slow customer payments, and upfront carrier or agent payments. The key inputs are open receivables, expected payout timing, and claim exposure. One delayed shipment can turn a good month into a cash squeeze, so reserve discipline matters as much as gross margin.

Tighten collections and reserves

Track receivable days, unpaid invoices, and shipments still at risk of reversal. If collections slip, cash gets trapped while fixed overhead still runs, including the disclosed $122K/month known fixed overhead. A clean rule helps: do not pay out more to owners than cash left after expected carrier, agent, and claim exposure.

Improve this by invoicing fast, collecting deposits where possible, and holding a dispute reserve until shipments clear. Tighter collections make income less lumpy and protect distributions. If refunds or chargebacks rise, cut owner draws first, not reserves.

Customer mix and retention

Repeat Shipper Mix

When more shipments come from repeat shippers, owner income gets steadier and easier to forecast. SMB importers repeat 15 times in Year 1 and 19 times in Year 5, enterprise shippers repeat 25 to 29 times, and e-commerce brands repeat 40 to 48 times. More repeat volume lowers sales friction and supports more reliable owner pay.

Mix matters too. If e-commerce brands rise from 30% to 50% of the book, revenue should be less lumpy because those accounts reorder more often. Low retention pushes the business to keep replacing lost shippers, which raises acquisition burden and can squeeze profit before any draw to the owner.

Track Repeat by Segment

Measure retention by shipper type, then watch the repeat count per account. The key inputs are shipments per account, segment mix, repeat shipments per year, and new accounts needed to replace churn. If a segment’s repeat rate slips, the forecast gets weaker and sales costs rise.

Bookings per active account

Share from e-commerce brands

Share from SMB importers

Share from enterprise shippers

Push the mix toward stable accounts, but keep service tight. Repeats only help owner income if documentation, support, and payment flow stay clean. One blunt test: if repeat shippers are growing but support time is also rising fast, the extra revenue may be going to operations instead of owner pay.

Mode, lane, and service mix

Mode, lane, and service mix

Mode, lane, and service mix changes both revenue and workload. Order values range from $2,500 for SMB importers in Year 1 to $17,000 for enterprise shippers in Year 5, while commission rate falls from 30% to 26%. Bigger orders can still lift income, but only if the extra handling does not eat the margin.

The key question is not just shipment value. It’s whether agent charges, documentation time, and service risk stay controlled. With no mode-specific cost data provided, the owner should judge each lane by retained commission, support load, and exception rate, not by invoice size alone. Bigger orders help only when the work stays lean.

Measure lane profit, not just volume

Track each lane by order value, commission %, and minutes spent on docs and follow-up. Split results by service type so you can see which lanes pay after the extra work. If a higher-value lane needs more touch but does not raise retained income, it is weaker for owner pay.

Test enterprise-style shipments against SMB work before you scale the mix. Watch whether faster quotes, fewer corrections, and lower dispute rates keep staff time flat. The best lane is the one that raises retained revenue per shipment without forcing more handholding.