How Much IT Budgeting Business Owners Make: $150K Planned Pay

Based on the researched assumptions, the model includes $150,000 in planned annual CEO pay, but operating-funded owner take-home is $0 until the business clears break-even and reserves First-year revenue is about $37,600, while the revenue needed to cover listed costs and the owner salary is about $527,000 before reserves By the mature year, revenue reaches about $410,400, but payroll and marketing also rise, so profit is still negative under the provided cost structure

Owner income$0Net margin-72% to 28%Revenue for target pay$538kBusiness difficultyHard

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income will change with revenue, margins, payroll, taxes, debt, and reinvestment.

Want the six income drivers?

1

Client Acquisition

10-100

More clients raise revenue fastest and spread fixed payroll across more billable work.

2

Payroll Load

$315K-$860K

Payroll climbs from $315K to $860K, so hiring too early can wipe out take-home.

3

Engagement Value

$376K-$4.1M

Higher-value assessments and renegotiations lift revenue fast as the work mix shifts up.

4

Retainer Mix

10%-42%

More ongoing optimization moves work into recurring revenue and smooths cash flow.

5

Delivery Efficiency

5-20h

Fewer hours per engagement keep labor and tool costs in check and protect margin.

6

Reserve Discipline

$0

With losses in Year 1 and Year 2, owner draw should stay at $0 until Month 29 breakeven.

Want to see the full forecast?

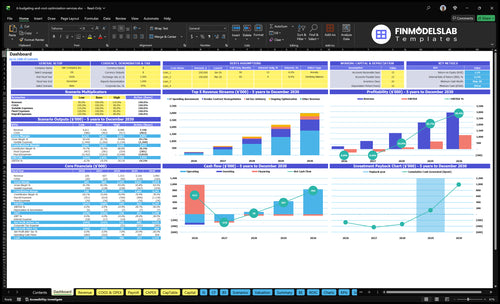

The IT Budgeting and Cost Optimization Financial Model Template shows dashboard tabs for revenue assumptions, client pipeline, delivery costs, overhead, payroll, owner income, reserves, and scenario testing. Charts run from $376k to $4,104k revenue, with $150k planned CEO pay, $762k fixed overhead, $20k-$150k marketing, and $2k-$15k CAC, so operating profit stays negative before outside funding.

Owner-income model highlights

CEO pay: $150k

Revenue: $376k-$4,104k

Scenario tabs test funding

How much can the owner of an IT cost optimization consulting business take home?

The owner of an IT Budgeting and Cost Optimization business can take home $0 from operations after reserves in the provided model until break-even is reached; the planned CEO salary is $150,000/year, but first-year revenue is only $376,000. For context, What Is The Most Critical Metric To Measure The Success Of Your IT Budgeting And Cost Optimization Service? matters because take-home depends on client volume, paid hours, hourly rate, delivery payroll, and reserve discipline.

Owner Pay Reality

$0 operating-funded take-home after reserves

$150,000 planned annual CEO salary

$376,000 first-year revenue

CEO salary equals 39.9% of year-one revenue

What Moves Pay

$4.104M mature-year revenue model

Revenue from assessments and renegotiation

Also from advisory and optimization retainers

Watch payroll, rates, hours, reserves

What expenses reduce owner income in an IT cost optimization business?

Owner income in IT Budgeting and Cost Optimization gets squeezed by two buckets: delivery costs and fixed overhead. Delivery work carries 5% software licenses, 4% data tools, plus lead consultant payroll, junior consultant payroll, and subcontractor support; in year one, sales commissions add 8% and travel adds 5%. If you want the launch math too, see How Much Does It Cost To Open, Start, And Launch Your IT Budgeting And Cost Optimization Business?

Delivery cost drag

5% software licenses

4% data tools

Lead consultant payroll

Junior consultant payroll

Overhead pressure

8% sales commissions

5% first-year travel

$6,350 monthly overhead

Payroll rises from $315k to $860k

Can an IT budgeting and cost optimization business scale without reducing owner income?

Yes, but only if added client capacity brings in more gross profit than the extra payroll, tools, and sales cost. In this model, revenue can reach $4.104M, but payroll also rises to $860k, so owner income usually gets squeezed unless pricing, utilization, or client volume improves. Solo expert delivery protects margin, yet it caps volume.

Protect margin

Solo delivery keeps overhead lean.

Subcontractors add capacity fast.

More staff raises fixed payroll early.

Gross profit must outrun costs.

Watch the squeeze

Revenue can reach $4.104M.

Payroll can reach $860k.

Scale can cut distributable income.

Fix pricing, utilization, or volume.

Key Takeaways

Qualified client volume drives most revenue growth.

Retainers and pricing lift income fastest.

Efficiency helps, but savings quality still matters.

Hold cash before paying owner draws.

Owner income scenario objective

Owner income scenarios

Owner draw stays tight because client growth pulls up payroll and operating costs. These cases show how 10, 47, or 100 clients change cash left after reserves.

Low, base, and high cases for owner income planning.

Scenario

Low CaseDownside case

Base CaseBase case

High CaseUpside case

Launch model

This is the lower earnings path, with 10 clients and $376k revenue.

This is the modeled middle path, with about 47 clients and $1.814M revenue.

This is the stronger revenue path, with 100 clients and $4.104M revenue.

Typical setup

The model uses 78% contribution after COGS and variable costs, $315k payroll, and no safe owner draw after reserves.

The model holds 81% contribution, $625k payroll, and still leaves no safe owner draw after reserves.

The model scales service volume, but listed costs still leave no safe owner draw after reserves.

Cost drivers

Client count

payroll

COGS and variable costs

reserve needs

Client count

payroll

contribution rate

reserve needs

Client count

payroll

service mix

reserve needs

delivery costs

Owner income rangeBefore owner reserves

$0No safe draw

$0No safe draw

$0No safe draw

Best fit

Use this to stress-test a lean launch with tight cash.

Use this for the main planning case and staffing plan.

Use this to test capacity, hiring, and cash pressure at scale.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

IT Budgeting and Cost Optimization Core Six Income Drivers

Client Acquisition Volume

Qualified Client Volume

This driver is the count of qualified US business clients that convert into paid assessments, vendor renegotiation projects, advisory work, and ongoing optimization. With $20k of marketing spend and $2k CAC, the math supports 10 clients; with $150k and $15k CAC, it still supports 10 clients. So volume only lifts owner income if referral flow or close rate improves.

Client count affects revenue, cash flow, and the owner’s draw. Assessments and vendor work pay sooner; optimization retainers smooth income later. The main inputs are leads, close rate, CAC, and the mix of one-time versus recurring work. If close rate slips, sales spend grows faster than profit, and owner pay stays unfunded.

Track CAC and Close Rate

Track qualified leads, proposal-to-close rate, and CAC by channel each month. Use marketing budget ÷ CAC = client count to test whether spend is buying enough work. If the count does not rise, tighten qualification, shorten the sales cycle, and push more referrals before adding budget.

Leads by source

Close rate by offer

CAC by channel

Referral share of new clients

Set separate targets for assessments, renegotiation projects, and retainers. A cheap referral that closes fast is worth more than paid traffic with weak fit. If referral flow lags, cap owner draws until pipeline cash can cover fixed labor and overhead.

Average Engagement Value

Average Engagement Value

Average engagement value is the revenue you collect per client job, before overhead. Here’s the quick math: 20 hours × $200 = $4,000 for a first-year assessment, 15 hours × $220 = $3,300 for vendor renegotiation, 5 hours × $180 = $900 for ad-hoc advisory, and 10 hours × $190 = $1,900 for ongoing optimization. A mix with more assessments and retainers lifts owner pay faster than small CAC cuts.

If the book skews toward $900 advisory work, the firm needs many more clients to cover the same fixed base. Higher-fee scopes also improve cash flow because each sale brings in more dollars per engagement before delivery costs and collections lag.

Raise the realized fee

Track realized hourly rate, billable hours, and service mix by offer. Separate assessment fees, implementation support, and retainer work in the quote, so each scope is priced on its own value. That lets you see whether the average ticket is moving toward $4,000 and $1,900 work instead of low-value one-offs.

Quote every deliverable separately.

Log hours by service line.

Review mix before owner draws.

What this estimate hides: if scope creep adds hours without higher fees, margin drops fast. The clean fix is simple—raise the fee when the work includes planning, implementation, or recurring reviews.

Delivery Efficiency

Faster Delivery, Higher Margin

Delivery efficiency lifts owner income when the same assessment or vendor review takes fewer hours and fewer rework loops. In the model, assessment work falls from 20 to 16 hours and vendor renegotiation falls from 15 to 13 hours. That raises effective revenue per hour from $200 to $250 on a $4,000 assessment, and from $220 to about $254 on a $3,300 vendor job.

Same fee, less labor means higher gross margin and more billable capacity. A 20% cut in assessment hours and a 13% cut in vendor hours can free cash for owner pay, but only if savings quality stays strong; weak analysis can hurt referrals and renewals, which lowers future income.

Trim Rework, Not Analysis

Track hours by work type, rework loops, and savings outcomes on every job. Use a standard spend intake, vendor templates, and scoped review checklists so the team spends less time fixing avoidable gaps. The goal is fewer non-billable hours, not less analysis.

Watch two guardrails: cycle time and savings quality. If speed pushes out a bad recommendation, renewals and referrals can fall, and that damages cash flow and owner draw. Measure each engagement against the 20 to 16 and 15 to 13 hour benchmarks, then keep senior review on the risky parts.

Labor And Tool Costs

Labor and Tool Costs

Payroll and software can squeeze owner pay fast. In this model, fixed tool COGS can range from 9% to 55% of revenue, payroll rises from $315k to $860k, and fixed overhead stays at $762k a year. If billable work does not rise with staffing, profit gets thin and owner take-home drops quickly.

Track billable hours, headcount, and tool spend together, not in separate silos. Variable costs move from 13% to 11% of revenue, so the key is splitting fixed costs like rent and insurance from variable costs like commissions and travel. Margin risk is highest when hiring runs ahead of paid client work.

Control Headcount Before It Hits Cash

Use a simple labor-to-revenue check each month. Compare payroll, tool COGS, and overhead against booked billable work before adding staff or renewing software. If labor is growing faster than revenue, the business may look busy but still leave the owner with little cash to draw.

Build the forecast with revenue, billable utilization, tool subscriptions, travel, commissions, rent, and insurance. Here’s the quick math: higher payroll plus higher tool COGS lowers contribution margin, while fixed overhead stays stuck at $762k. The best control is to delay hiring until paid work supports it.

Track payroll against billings monthly.

Separate fixed and variable costs.

Cancel unused tools fast.

Hire only after demand is booked.

Recurring Retainer Revenue

Recurring Retainer Revenue

Recurring retainers smooth owner income because the work repeats: budget support, vendor renewal reviews, cloud spend monitoring, and quarterly cost reviews. In the model, recurring work rises from 10% to 42%, hours rise from 10 to 12, and the hourly rate rises from $190 to $214. That lifts one retainer from $1,900 to $2,568 before delivery costs, and better retention cuts cash-flow gaps.

Track Retention and Retainer Hours

Track retention rate, committed hours, and price per client. If recurring work slips, the owner loses the steady cash that supports pay between one-time audits. Forecast take-home income from signed retainers first, then treat project work as upside. One clean rule: protect the recurring book before adding more new client chasing.

Measure renewal rate each month.

Price by hours and scope.

Lock in quarterly review dates.

Cash Reserves And Owner Draws

Cash Reserves and Owner Draws

Owner pay here is the cash left after the business keeps enough money for delayed collections, sales spend, hiring, software renewals, and tax set-asides. In this model, the planned $150k CEO salary is built in, but safe operating-funded distributions are $0 while losses remain. So net profit on paper does not mean cash is ready for an extra draw.

The key inputs are cash on hand, accounts receivable timing, monthly burn, and the next renewal or hire. If cash stays tight, owner income stays capped even when sales improve. Personal taxes are outside this estimate, so the draw number is not a full after-tax take-home figure.

Track cash before you pay yourself

Measure cash runway, not just profit. If the business cannot fund the next operating cycle, owner distributions stay at $0. Use a monthly reserve check before approving any draw.

Cash on hand

Accounts receivable timing

Payroll and software renewals

Tax set-asides and hiring

Before adding analysts or raising draws, test the cash hit from slower collections and new fixed costs. Update the reserve plan when invoices slip or renewals land. That is what protects owner income later.