How Much IT Compliance And Governance Owners Can Make: $180K Pay Test

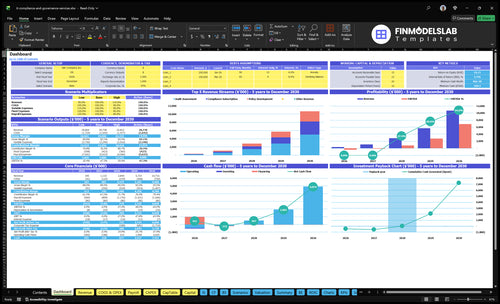

An IT compliance and governance business owner can plan around little to no operating-funded take-home in the first year if the firm hires ahead of revenue, even when the model includes a $180,000 founder salary Under the researched assumptions, revenue grows from about $168,000 in Year 1 to $155 million in Year 3 and $732 million in Year 5 The owner-income pool turns more attractive after the firm has enough recurring compliance subscriptions, project work, and staff utilization to cover payroll, marketing, software, insurance, and admin costs These are planning assumptions, not guaranteed earnings

Owner income$180kNet marginNeg. to 81%Revenue for target pay$222kBusiness difficultyHard

Want the six drivers behind owner income?

1

Recurring Retainers

$101K-$540K

Subscription adoption rises from 70% to 90%, and Year 1 MRR is about $101K versus about $540K in Year 5, so recurring work becomes the revenue base.

2

Labor Load

$485K-$1.2M

Annual wages climb from about $485K in Year 1 to about $1.2M in Year 4 and Year 5, so staffing discipline has a direct hit on take-home.

3

Client Value

$180-$240

Hourly rates move from $180 to $240, so each client can produce more revenue before you add another seat.

4

Billable Hours

4-15h

Retainers take about 4 hours, while audits take 15 and policy work 12, so reducing delivery time lifts consultant throughput.

5

Pricing Power

30%-40%

Policy development grows from 30% to 40% of mix, and that work prices at $200 to $220 an hour, so niche work lifts margin.

6

Cash Control

$7.1K/mo

Fixed overhead is $7,050 a month, and cash bottoms at $184K in Month 27, so reserve discipline decides how much profit you keep.

Want to test your own owner-income case?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Can you check owner income in the IT Compliance and Governance model?

See the full IT Compliance and Governance Financial Model Template for dashboard, revenue, service mix, staffing, costs, cash flow, and owner take-home. It ties Year 1 revenue of about $168k to Year 3 near $155M and Year 5 near $732M. Open the model.

Owner-income model highlights

Founder take-home output

Revenue and margin bridge

Reserve holdback scenarios

Solo IT compliance consultant versus firm owner income

In IT Compliance and Governance, solo owner income looks cleaner because the founder sells and delivers the work, but revenue stops when their hours do. A boutique firm can grow with analysts, consultants, sales, and admin support, yet in Year 1 a staffing load of $150k for the lead consultant, $100k for sales, $55k for admin, and $180k for the founder is too heavy for about $168k of revenue; by Year 5, about $732M can support it if client acquisition and delivery volume show up.

Solo owner cash flow

Founder sells and delivers work.

Income stays cleaner on paper.

Hours cap revenue fast.

Low overhead, but limited scale.

Boutique firm math

Analysts and sales expand capacity.

Year 1 payroll is $485k.

$168k revenue cannot carry it.

$732M revenue can, if volume lands.

What affects IT compliance business owner income the most?

In IT Compliance and Governance, owner income is driven most by recurring retainers and utilization. Here’s the quick math: subscription adoption rises from 70% in Year 1 to 90% in Year 5, hourly pricing rises from $180 to $200, and monthly hours per subscribed client rise from 4 to 6, while audit assessment time falls from 15 to 11 hours. Income gets weaker if one large client dominates revenue, consultants sit underused, or audit support creeps beyond scope.

Income drivers

Retainers create steady cash flow.

90% adoption lifts predictability.

$200/hour supports higher revenue.

6 hours per client raises monthly billings.

Income risks

One client can distort income.

Low utilization cuts owner pay fast.

Scope creep hurts margins.

11 audit hours only help if efficient.

What margins do IT compliance consulting businesses have?

Margins for IT Compliance and Governance are tight at the start, but they improve as revenue grows faster than fixed labor and overhead; if you want the launch budget first, see What Is The Estimated Cost To Launch Your IT Compliance And Governance Business?. Here’s the quick math: technology stack runs at 8% of revenue in Year 1 and 5% by Year 5, training falls from 4% to 2%, sales commissions drop from 7% to 5%, and external expertise declines from 5% to 3%. Fixed overhead is $7,050/month, and payroll is the biggest swing factor, so Year 1 is loss-making on a staffed plan while Year 5 has strong profit capacity.

Year 1 pressure

Staffing drives the loss

Overhead stays at $7,050

Tech stack takes 8%

Sales commissions take 7%

Year 5 lift

Tech stack drops to 5%

Training drops to 2%

Commissions drop to 5%

External expertise drops to 3%

Key Takeaways

Recurring retainers stabilize cash and owner pay planning.

Specialization lifts rates and reduces rework.

Utilization improves when paid work replaces admin.

Overhead and payroll can outrun early revenue.

Compare lean, base, and high-scale owner-income scenarios

Owner income scenarios

Owner income swings with client volume, CAC, staffing, and how much work sits in subscription versus project services. Early growth is tight, but scale can leave real cash after the founder salary.

Compare owner pay at low, base, and high operating scales.

Scenario

Low CaseStartup strain

Base CaseScale transition

High CaseMature advisory model

Launch model

This is the lower-earnings path where early sales volume is too thin to fund full owner pay.

This is the modeled middle case where the firm is close to break-even after the founder salary.

This is the stronger upside path where scale and lower CAC create real owner-income capacity.

Typical setup

About 20 acquired clients from $50k marketing at $2,500 CAC keep the model under pressure, and operations cannot support $180k owner pay.

About 139 acquired clients from $250k marketing at $1,800 CAC puts the firm near break-even, with about $129k operating pool before founder pay and reserves.

About 500 acquired clients from $600k marketing at $1,200 CAC supports a much larger advisory platform and strong owner-income capacity before reserves.

Cost drivers

High CAC

light client volume

founder-heavy delivery

fixed team load

project mix

Lower CAC

larger client base

founder salary

mixed service revenue

rising support staff

Lower CAC

high client volume

better staffing leverage

stronger margins

deeper advisory mix

Owner income rangeBefore owner reserves

No owner payOwner pay blocked

$129kNear break-even

High take-home capacityCash-rich upside

Best fit

Use this to stress test the first operating year when demand is still thin and cash stays tight.

Use this as the planning base for budgeting, hiring, and owner draw timing in a normal growth path.

Use this to test upside when the firm has enough volume, delivery depth, and pricing power to pay the owner well.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

IT Compliance and Governance Core Six Income Drivers

Recurring Compliance Retainers

Recurring Compliance Retainers

Retainers turn compliance work into steadier income than one-off projects. On the model here, a subscribed client is worth 4 hours per month at $180/hour, or $720/month in Year 1, then 6 hours per month at $200/hour, or $1,200/month in Year 5. That gives the owner more cash visibility and makes pay planning cleaner.

The catch is scope. Policy updates, control monitoring, vendor risk support, audit readiness, and governance meetings fit the retainer; extra cleanup work does not. If scope creep turns included support into unpaid project work, gross margin drops fast and the owner’s draw gets less predictable.

Scope Control And Pricing Discipline

Track active retainer clients, included hours, hours used, and overage billed each month. Here’s the quick math: one client at $720/month is $8,640/year; by Year 5, that same client is $14,400/year. The value only shows up if the team stays inside the package and bills extras fast.

Define monthly hours in writing.

Price extra work separately.

Review scope at every renewal.

Watch time spent on revisions.

What this estimate hides is delivery drift. If governance meetings, audit prep, or vendor reviews keep expanding, the retainer stops behaving like subscription income and starts acting like a fixed-fee project with no guardrails.

Delivery Labor Cost

Delivery Labor Cost

Delivery labor is the salary load for the people doing the work, mainly the $150k lead consultant in Year 1 and the $120k senior consultant in Year 2. It expands capacity, but if sales lag, it cuts owner take-home fast. Here’s the quick math: Year 1 revenue of about $168k cannot carry a staffed delivery team, so the owner must fund payroll before the client base catches up.

By Year 5, the stated about $732M revenue can absorb $660k of lead and senior consultant salary. The inputs that matter are billable revenue, salary cost, utilization, and the timing of each hire. Delegation frees the owner from doing every task, but it also adds payroll risk and cash pressure if hiring comes too early.

Track Payroll Before You Add Heads

Track salary load as a share of monthly revenue and cash on hand. If new consultant pay arrives before billings do, owner draw gets squeezed first. Use a simple rule: don’t add a fixed salary unless current and near-term recurring revenue can cover it plus core overhead. One hire should buy capacity, not create panic.

Model the next 6 to 12 months with revenue, billable hours, salary, and utilization. Test what happens if sales land 1 quarter late. If the team can’t stay covered at the lower revenue base, delay the hire, keep the owner in delivery longer, or phase the role with contract support before moving to full salary.

Billable Utilization

Billable Utilization

Billable utilization is the share of consultant time that gets billed to clients. Here, subscription hours rise from 4 to 6 per subscribed client, a 50% increase, while audit assessment work falls from 15 to 11 hours and policy development from 12 to 10 hours. That shifts time from rework and admin into paid delivery, so revenue quality improves and owner pay is easier to fund.

The key inputs are total consultant hours, billable hours, and hourly rate. If just 2 hours per client move from unpaid work to billed work at $180 to $240 per hour, that adds $360 to $480 in billings per client month. The risk is simple: push utilization too high and burnout, errors, and audit misses can erase the gain.

Raise Billed Time Share

Track billable time by service line: subscription support, audit assessments, and policy development. Use the model shift from 4 to 6, 15 to 11, and 12 to 10 hours as your check on whether more work is client-paid and less is internal cleanup. Here’s the quick test: if billed hours rise but rework rises too, utilization is fake.

Protect margin with tighter scope, templates, and fixed meeting blocks. Keep admin, follow-up, and document cleanup from eating paid hours, and forecast owner draw from billable hours × rate after rework time. If quality slips, the hidden cost shows up fast in refunds, slower cash collection, and lower take-home profit.

Specialization And Pricing Power

Specialization Raises Price

When the firm narrows to SOC 2 advisory, HIPAA compliance support, ISO 27001 readiness, or vendor risk management, it can charge more for the same work. Here’s the quick math: $180/hour to $200/hour on subscriptions is a 11.1% lift, $220/hour to $240/hour on audit assessment is 9.1%, and $200/hour to $220/hour on policy work is 10%.

That price lift feeds owner income fast. A 4-hour monthly client goes from $720 to $800, or $80 more per client each month, before overhead. The catch is scope creep: broad generalist work is harder to standardize, so rework rises, delivery slows, and margin leaks out of the same sales volume.

Price by Niche, Not by Hour

Track each niche by close rate, billable hours, rework hours, and realized rate. If one offer sells at $240/hour but takes extra revisions, the headline rate can hide weak take-home. The goal is cleaner scope, shorter delivery, and fewer unpaid follow-ups.

Measure rate by service line.

Count rework hours weekly.

Price fixed-scope deliverables.

Standardize templates and checklists.

Use niche language in proposals so buyers see a specific outcome, not a generic help desk. That usually improves conversion and makes staffing easier, because the work repeats. If the same offer keeps changing from client to client, the firm loses the very pricing power specialization should create.

Overhead, Reserves, And Cash Discipline

Fixed Overhead and Reserves

$7,050/month of fixed overhead comes off the top before the owner sees cash. That includes rent, utilities, insurance, accounting, legal, software, supplies, and professional development. On its own, that is $84,600 a year, so even healthy gross margin can still leave weak distributable income if sales don’t cover the base load.

Cash gets tighter as marketing scales from $50k in Year 1 to $600k in Year 5. Reserves are there to cover payroll and audit deadline risk, but they are not owner pay. If reserve targets are too thin, the owner may have to delay draws to protect operations.

Watch the cash floor first

Track three inputs every month: fixed overhead, marketing spend, and reserve balance. Also watch the timing of payables, payroll, and audit work. Here’s the quick math: fixed overhead alone uses $84,600 a year, so any owner draw has to come after that and after reserve funding.

Separate reserves from operating cash.

Set a payroll-only reserve floor.

Cap overhead before hiring.

Review marketing spend against cash.

The startup cash load is real too: $25k furniture and equipment, $18k IT infrastructure, $12k platform license, $10k website and brand work, $5k legal setup, $7k security system, and $8k software licenses. That cash is tied up early, so owner pay should wait until reserves stay funded.

Average Client Value

Average Client Value

Average client value rises when the firm sells project-plus-retainer work, not just hourly tasks. A Year 1 audit assessment is 15 hours × $220 = $3,300 per project, and policy development is 12 hours × $200 = $2,400. By Year 5, those projects still reach $2,640 and $2,200, so better packaging lifts revenue per client without adding the same workload.

This metric includes project fees, retainer hours, hourly rates, and repeat work. The key inputs are hours, price per hour, and how often the client buys again. Discounting complex work cuts margin fast, so the owner’s take-home improves most when audit and policy work is priced cleanly and kept out of scope creep.

Price the Project, Then Add Retainer

Track average revenue per client by service line each month. Split it by audit assessment, policy development, and retainer work, then compare the realized rate to the target rate. If a project runs long or sells below $220 or $200 per hour, the owner is giving away profit and cash.

Push bundled scopes: project first, then ongoing monitoring, governance meetings, or audit readiness support. One clean rule helps: price the complex work first, then attach the recurring work. That raises client value without needing the same number of new clients or the same number of hours.