How Much Large Venue Projector Rental Owners Can Make On $918K Revenue

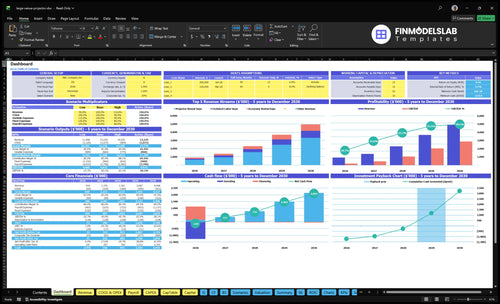

A large venue projector rental owner can plan around a $145K owner-manager salary in this model, but extra take-home depends on cash flow after debt, reserves, taxes, and reinvestment The researched first-year case shows $918K revenue and $190K EBITDA, while Year 5 reaches $4948M revenue and $2876M EBITDA Those are planning assumptions, not guaranteed earnings Utilization, pricing, labor control, maintenance, and the $1275M equipment investment drive the real owner outcome

Owner income$145KNet margin21%→58%Revenue for target pay$918KBusiness difficultyHard

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margins, payroll, taxes, debt, and reinvestment. Not guaranteed salary, tax advice, or owner distribution advice.

Want to see the six income drivers?

1

Utilization

180-850

With fixed overhead near $16K a month, more booked projector days spread the floor cost and lift owner pay fast.

2

Rental Rate

$3.5K-$3.9K

A higher projector day rate adds revenue on every event, and most of that extra cash can flow through to EBITDA.

3

Package Mix

$5.1K-$5.8K

More screen, lens, and media-server add-ons raise the average ticket without adding much extra setup time.

4

Labor Efficiency

0.5-4 FTE

Tight technician and support staffing protects margin as bookings scale, so wage drag does not eat owner take-home.

5

Fleet Reserves

7.5%-8.5%

Maintenance, freight insurance, and small supply costs run as a steady share of sales, so reserve discipline protects cash.

6

Repeat Channels

5.4x

Repeat bookings fill gaps in the calendar and help revenue scale from $918K in year 1 to $4.95M in year 5.

How many projector rental days are needed to pay the owner?

For Large Venue Projector Rental, you need about 125 projector rental days to pay the owner’s $145K salary after non-owner overhead, before debt and reserves; without owner pay, about 91 days covers fixed overhead and payroll. For setup context, see How Much To Start Large Venue Projector Rental Business?.

Quick math

180 Year 1 projector rental days

$5,100 average revenue per rental day

86% contribution after variable costs

$4,386 contribution per rental day

Pay target

91 days covers about $399.5K overhead

125 days adds the owner salary

180 days supports $190K EBITDA

Fleet count and debt change the target

What expenses reduce projector rental owner income?

For Large Venue Projector Rental, income gets cut first by direct event costs: maintenance and parts at 45% to 55%, freight and logistics insurance at 30%, sales commissions at 50%, and consumables at 15%. If you’re sizing upfront spend, see How Much To Start Large Venue Projector Rental Business?; the fixed load adds another $16K a month for warehouse, insurance, marketing, software, utilities, and dues. Long-term leakage also comes from repairs, depreciation, financing, reserves, and subrentals, while payroll starts at $3525K in Year 1 and reaches $875K in Year 5 as EBITDA margin rises from about 207% to 581% with better utilization.

Direct cost drains

Maintenance and parts: 45% to 55%

Freight and logistics insurance: 30%

Sales commissions: 50%

Consumables: 15%

Fixed and hidden drag

Monthly overhead: $16K

Payroll: $3525K to $875K

Repairs, depreciation, financing

Reserves and subrentals

Should a projector rental business buy or subrent equipment?

If bookings are steady, Large Venue Projector Rental should buy the core fleet; ownership can lift margins when rental days hold, rates stay firm, and gear stays busy. Here’s the quick math: researched capex totals $1275M across projectors, lenses, screens, media servers, tools, van, and IT, cash dips to negative $215K in Month 6, payback takes 39 months, and IRR is 366%. If demand is still shaky or jobs vary by lens, brightness, or screen setup, subrenting is the safer cash move.

Buy when use is steady

Higher margin when booked often

Fixed fleet fits repeat events

39-month payback in the model

366% IRR if rates hold

Subrent when demand is uneven

Protect cash before bookings mature

Match specs by lens and brightness

Reduce idle gear and repair risk

Limit debt in early months

Key Takeaways

Utilization drives income by spreading fixed fleet costs.

Higher-brightness pricing only works with strong demand.

Add-ons lift revenue, but they also add costs.

Repeat bookings protect margin and reduce idle days.

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income moves with rental days, pricing, and staffing. Early fleet spend also creates tight cash, so the owner pay path changes as utilization scales.

Low, base, and high income paths by utilization.

Scenario

Low CaseLow Case

Base CaseBase Case

High CaseHigh Case

Launch model

Owner income stays salary-led while utilization is still ramping.

Owner income grows as rental days and labor days rise with a more staffed operation.

Owner income is strongest when utilization is mature and the payroll base is fully built.

Typical setup

Year 1 runs at 180 rental days, about $5,100 average package revenue, $918K revenue, roughly 86% direct margin, and $190K EBITDA, with the owner taking the $145K CEO salary and cash still tight.

Year 3 reaches 420 rental days, about $5,479 average package revenue, $2.301M revenue, roughly 85.5% direct margin, and $1.052M EBITDA, with more technicians and account coverage.

Year 5 reaches 850 rental days, about $5,821 average package revenue, $4.948M revenue, 85% direct margin, and $2.876M EBITDA, but payroll and reserve needs are much larger.

Cost drivers

180 rental days

$5,100 package revenue

86% direct margin

$190K EBITDA

$145K CEO salary

420 rental days

$5,479 package revenue

85.5% direct margin

$2.301M revenue

$1.052M EBITDA

850 rental days

$5,821 package revenue

85% direct margin

$4.948M revenue

$2.876M EBITDA

Owner income rangeBefore owner reserves

$145K salary-ledLow Case

Salary plus bonus roomBase Case

Salary plus distributionsHigh Case

Best fit

Use this to test launch-month cash pressure and a salary-only owner draw.

Use this as the mid-case for steady utilization and a fuller team.

Use this to test upside when capacity is full and cash reserves need discipline.

!

Planning note: Scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Large Venue Projector Rental Core Six Income Drivers

Utilization

Utilization Drives Owner Pay

Utilization is the share of projector fleet days that are billed. In this model, rental days rise from 180 in Year 1 to 850 in Year 5, and monthly fleet rental days rise from 15 to 71. More paid days spread warehouse, insurance, maintenance, and financing costs over more revenue, so owner income climbs when idle time falls.

Here’s the quick math: if the fleet stays underused, high-cost projectors still carry fixed costs with no offsetting rent. That hurts cash flow and slows owner pay, even if the equipment is top tier. The model ties stronger utilization to revenue rising from $918K to $4,948M, so paid days are the main swing factor.

Track Paid Days, Not Just Fleet Size

Measure utilization as rental days ÷ available projector days, then break it out by projector count, venue type, and month. That shows whether growth comes from more bookings or just a bigger fleet. Also track downtime from setup, repair, and transport, because every unused day still burns overhead.

Track booked days per projector.

Watch idle days by unit.

Separate repair downtime from demand gaps.

Forecast cash before buying more units.

If utilization rises without more fixed staff or storage, gross margin improves and more cash can flow to owner draws. If bookings stay thin, the fleet looks impressive on paper but still drags profit because the cost base does not shrink with demand.

Package Mix And Add-Ons

Package Mix

Projector-only rentals leave money on the table when the job also needs screens, lenses, signal processing, delivery, setup, and on-site technical support. In Year 1, the package average is $5,100 per rental day versus $3,500 for projector-only, so the bundle lifts revenue by $1,600 per day, or about 45.7%. By Year 5, that gap grows to $1,921 per day.

That lift helps owner pay only if the extra fees beat the added labor, equipment wear, logistics, and setup risk. Here’s the quick math: more add-ons raise top-line revenue, but the cash left after technician time and truck runs can shrink fast if the event is complex. One clean rule: do not treat every add-on dollar as pure profit.

Price the Bundle, Track the Margin

Measure attach rate (how often a package is sold), incremental labor hours, and delivery/setup cost per event. Compare package revenue to projector-only revenue, then subtract the added cost to see the real gross margin. If a screen or support add-on adds revenue but also adds a second crew move, its margin can be thin even when sales look strong.

Track package rate per rental day.

Price each add-on separately.

Log extra labor hours by event.

Reserve cash for wear and repairs.

Year 5 package revenue reaches $5,821 versus $3,900 projector-only, so the mix matters. If the bundle also pushes setup time, missed delivery windows, or overtime, owner income can fall even as sales rise. Keep the forecast tied to revenue per event and cost per event, not just quote size.

Repeat Booking Channels

Repeat Booking Channels

Repeat bookings from venues, planners, production companies, and corporate event clients cut idle days and smooth owner income. In this model, that matters because a weak pipeline leaves expensive projectors sitting while fixed overhead and payroll keep running. Repeat demand also makes pricing and package mix more stable, so cash flow is less lumpy.

Here’s the key test: if recurring work does not absorb the $4K monthly digital spend plus any 50% sales commissions, the channel is too costly. The owner should track bookings per account, repeat rate, and days between rentals. One clean metric: more repeat rental days, less dead inventory time.

Improve Repeat Bookings

Focus on accounts that can rebook: venues with steady calendars, planners with recurring programs, production firms, and corporate teams. Build simple account lists, then measure booked days per client, not just leads. That shows which relationships actually pay for inventory, labor, and overhead.

Track repeat days by account

Price for recurring volume

Protect margin after commissions

Document standard package rates

Forecast idle days each month

What this hides is timing risk: a few lost repeat clients can strand high-cost gear fast. So the owner should review pipeline health every month and watch whether repeat demand is strong enough to keep utilization up without discounting.

Labor And Delivery Efficiency

Labor and Delivery Efficiency

When technical labor days climb from 120 to 620, the job stops being just a rental business. More crew time, delivery miles, and teardown hours lift cash payroll and can squeeze owner pay unless each event is scheduled tightly. Owner-operated labor lowers cash outlay, but it also hides unpaid owner time, so profit can look better than the real take-home.

The key inputs are crew hours per event, venue load-in, delivery routing, and teardown speed. If those are controlled, you can protect margin without hurting service quality. If not, labor becomes the line that drains the spread between rental price and gross margin.

Track Labor Per Booking

Build every quote from labor hours, delivery distance, and load-in rules. Staffing is modeled at $3,525K and $875K, so small scheduling waste can hit owner income fast. Use pre-built kits, route jobs by venue, schedule technicians tightly, and cut teardown time where possible.

Measure hours per booking.

Price difficult load-ins higher.

Track unpaid owner labor.

Fleet Cost And Reserves

Fleet Reserves

With $1.275M tied up in projectors, lenses, screens, servers, tools, a van, and IT, this driver decides how much cash is left for owner pay. Maintenance and parts run 45% to 55% of revenue, so thin reserve planning turns good revenue into weak draws fast.

The cash risk is real: logistics insurance can absorb 30%, minimum cash falls to -$215K in Month 6, and payback is 39 months. If repairs, debt service, and replacement are underfunded, the owner ends up financing the fleet instead of getting paid.

Protect Owner Pay

Set the reserve from booked revenue before taking draws. Track repair cost per rental day, insurance cost, replacement timing, and debt service by asset class so you can see which item is draining cash.

Booked rental days versus downtime

Maintenance and parts as a revenue %

Insurance, logistics, and claims

Replacement reserve and debt service

If reserve funding is late, cash gets trapped in broken gear and missed replacements. Pay the owner only after the fleet reserve is funded, so income follows real free cash, not gross revenue.

Pricing And Projector Class

High-Brightness Day Rates

This driver is the rental rate by projector class plus labor and accessory fees. In the model, high-brightness projector rent rises from $3,500 in Year 1 to $3,900 in Year 5, while labor day rates rise from $1,200 to $1,400 and accessory rates from $800 to $900. One clean one-liner: better gear can charge more.

Here’s the quick math: that is a $400 increase per rental day, or 11.4% on projector rent alone. Pricing power comes from brightness, laser units, lens inventory, venue complexity, reliability, and technician quality. If booked days do not hold, the higher rate does not help owner income; it just leaves expensive equipment idle.

Price by Class and Track Attach Rate

Price each job by class, not by habit. The owner should track realized rental rate, utilization, labor add-ons, and accessory attach rate by venue type. That shows whether the business is earning more per paid day or just quoting higher and winning less work. A higher rate only improves take-home income when booked days stay steady.

Track booked days by projector class.

Measure labor and accessory attach rates.

Review discounts by venue complexity.

Watch utilization before raising rates.

If demand is strong, lift rates on complex venues, urgent installs, and premium laser units first. If demand softens, protect cash flow before pushing price again, because fixed costs still sit on the books and the owner’s profit draw depends on keeping rental days full.