How Much Can A Lemonade Stand Owner Make With $122k EBITDA?

Lemonade Stand Bundle

Key Takeaways

Saturday traffic and events drive the biggest revenue swings.

Price by daypart; weak conversion can erase gains.

Track ingredient and packaging costs separately each cup.

Fixed costs and setup cash can delay breakeven.

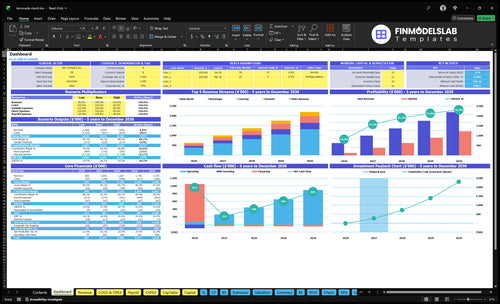

Owner income$122k-$1.215MNet margin18% to 56%Revenue for target pay$676kBusiness difficultyHard

Want to test your lemonade stand income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on traffic, margin, payroll, taxes, reserves, and operating discipline.

For Lemonade Stand, you can’t answer this with revenue alone; use contribution margin per cup after COGS (cost of goods sold), variable fees, and marketing. The model shows 80.5% at $18 AOV, $14.49 per sale at $22 AOV, and about $283k in monthly fixed costs plus payroll before reserves. So break-even cups = $283k divided by contribution per cup, and the count goes up if the owner wants profit too.

Break-even math

Use contribution per cup, not sales.

Divide $283k by cup margin.

Add profit to the numerator.

Higher fees raise the cup count.

What changes the count

$18 AOV shows 80.5%.

$22 AOV shows $14.49 per sale.

Fixed costs set the floor.

Target profit pushes volume higher.

How much money can a lemonade stand make in a day?

Yes, Lemonade Stand can be profitable at the operating-profit level. In the model, it breaks even in Month 4, pays back in 14 months, and delivers $122k in first-year EBITDA. But that result depends on a permissioned location, event traffic, pricing, operating days, and owner involvement, and it also carries heavy upfront needs: $965k capex, $273k payroll, and $810k minimum cash.

Profit drivers

Use permissioned sites only.

Push event-day traffic.

Price for the crowd.

Stay open more days.

Cost pressure

Fund $965k capex.

Cover $273k payroll.

Hold $810k cash.

Cut waste to raise income.

Lemonade Stand Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want to see the main income drivers?

1

Cups Sold

50-150/day

More daily cups is the biggest swing factor, because 50 to 150 first-year customers changes revenue fast before fixed costs move.

2

Cup Price

$18-$22

A higher cup price lifts take-home on every sale, and the model's $18 to $22 range expands revenue without adding labor.

3

Unit Cost

15.5%

Every point of ingredient and drink cost hits margin directly, so keeping unit cost near 15.5% protects cash on each cup.

4

Location Access

3x

Better street or event access can push traffic toward the busiest days, which raises sales without changing the menu.

5

Open Days

7/wk

Selling more days smooths seasonality, and weekend volume keeps weekly revenue from dropping hard.

6

Fixed Load

$5,550/mo

Monthly fixed costs run $5,550, so the stand needs enough gross profit and cash reserves to clear overhead before owner pay shows up.

Lemonade Stand Core Six Income Drivers

Customer Volume And Cups Sold

Customer Volume And Cups Sold

Traffic is the biggest first-year revenue driver. The model ranges from 50 Monday customers to 150 Saturday customers, so the owner’s income depends on how many covers and cups sell each day. Parks, events, neighborhoods, sports games, and fundraisers can lift volume, but slow days still burn through fixed costs, which keeps take-home pay under pressure.

Here’s the key point: more cups sold raises revenue fast, but only if selling hours, pitchers, ice, cups, and staffing match demand. The model says each added $18 midweek sale contributes about $1,449 before fixed cost recovery, so small traffic gains matter when the line is busy.

Track Covers, Not Just Sales

Measure customers per daypart, cups sold per customer, and sales per selling hour. That tells you whether volume is coming from more traffic or just bigger tickets. If a site can’t support the expected count, revenue stalls even when prices are fine.

Staff to the peak day first, then hold enough stock for ice, cups, and pitchers. If you can add traffic from event days or weekend footfall, the same fixed costs get spread over more sales, which improves cash flow and owner draw.

1

Price Per Cup And Average Order Value

Price Per Cup and Average Order Value

Average order value (AOV) is the dollars per ticket, and it drives revenue and margin at the same time. In year one, the model uses $18 midweek and $22 on weekends; in the mature year, that rises to $24 and $28. Higher pricing lifts contribution, but only if customers still convert. If the price feels wrong for cup size, setting, or local spending power, the gain can disappear fast.

Here’s the quick math: AOV improves 33% midweek and 27% on weekends from year one to maturity. That increase feeds cash flow and owner pay after food, labor, and rent, but it also raises the risk of fewer orders. The key inputs are customer count, order mix, daypart, and location. Price helps only when the check gets bigger without hurting traffic.

Test Pricing by Daypart and Location

Set prices by daypart and location, not with one flat menu. Track AOV, conversion rate, and gross margin separately for midweek and weekend service so you can see whether higher checks are really improving take-home income. Test one change at a time, then compare tickets, mix, and sales before you roll it wider.

Track AOV by daypart.

Watch conversion rate.

Match price to cup size.

Fit local affordability.

Test event pricing.

If a higher price lifts the check but cuts traffic, the owner can end up with less profit and less cash for draws. The real job is to protect revenue quality, not just raise the sticker price.

2

Ingredient And Packaging Cost Per Cup

Cost Per Cup

This driver decides whether each cup adds cash or drains it. The model shows first-year COGS at 155% of revenue, so every $1 of sales carries $1.55 of food and beverage cost before rent, payroll, or owner pay. That means gross profit is negative until variable cost comes down.

In the mature year, the model says COGS falls to 130% of revenue, but the stand still needs tighter control. Track lemons, sugar, cups, lids, straws, ice, water, and spoilage separately; fixed setup costs do not belong in cost per cup.

Track Waste Daily

Measure one cup from recipe to trash. Use purchase logs, batch counts, and waste counts so you can see where margin leaks. If spoilage rises after busy days, cash gets hit twice: once in the buy, once in the waste. Lower unit cost leaves more gross profit to cover fixed costs and owner draw.

Count lemons per cup.

Log cups, lids, straws.

Separate ice and water use.

Book spoilage every week.

Match invoices to cups sold.

Here’s the quick math: cut even small waste on packaging or produce, and each sale keeps more cash for the owner. If a cost line jumps, compare it to cups sold, not total revenue alone.

3

Location And Event Access

Location and Event Access

Location controls how many people see the business, and that drives take-home income. A high-foot-traffic event can support 150 first-year customers and a $22 weekend AOV, or about $3,300 in one day before costs. Traffic, not décor, decides the day.

Permissioned sites can also add fees, time limits, product rules, and setup limits. A quiet corner can miss break-even even with decent margin, because fixed costs like $5,550 per month keep running. Ask what the site can produce per selling hour before you commit.

Test Sales Per Selling Hour

Track customers per selling hour, weekend AOV, site fees, and any rules that cut speed or menu mix. Compare event sites, parks, and corner spots using the same labor plan. If one site cannot reach the volume you need, it lowers cash flow and squeezes owner pay.

Count customers by hour.

Log fees and setup limits.

Test weekend AOV by site.

Review event calendars weekly.

Use those numbers to forecast profit by location, not just revenue. If a site needs more staff or shorter selling windows, raise price or walk away. The best spot is the one that covers fixed costs fast and still leaves room for distributions.

4

Operating Days And Seasonality

Operating Days

This driver is the number of days you can actually sell, and when they land on the calendar. The model assumes weekday demand from 50 Monday customers to 150 Saturday customers in year one, so one strong day can produce far more income than a slow weekday.

Warm weather, weekends, holidays, and event calendars shape available revenue days. For a temporary stand, missed days are lost income, not delayed income, so the owner’s take-home pay depends on staffing and inventory matching the best-probability selling days.

Track Peak Days

Forecast each day with three inputs: expected customers, average check, and open hours. If Saturday runs at 150 customers and Monday at 50, the schedule changes cash flow fast even when unit margins stay the same.

Track weather, local events, and holidays, then staff and stock the top days first. If setup is slow or inventory runs out early, the owner loses revenue on the easiest sales days and has less cash left for profit or pay.

5

Fixed Costs, Setup Costs, And Reserves

Fixed Burn Delays Owner Pay

This model starts with a heavy cash load, so owner take-home stays low until the business clears its fixed burn. $5,550 a month in fixed costs before payroll, plus $273k in first-year payroll, means the business carries about $339,600 in annual fixed operating burden before food and drink costs.

Setup capex of $965k and a $810k minimum cash need in Month 2 mean break-even is not the same as owner income. The owner has to separate recovery of startup cash from ongoing profit and distributions, or early draws can starve working capital.

Protect the Cash Floor

Track monthly fixed burn, payroll timing, and cash runway against the $810k Month 2 floor. If the reserve dips below that level, slow owner draws first, not supplier payments or core staffing. That protects the chance to reach true operating profit.

Build a simple monthly forecast that separates startup payback, ongoing profit, and owner distribution. Keep capex, reserve use, and recurring fixed costs in different lines so you can see whether cash is coming from sales or from the original funding pool.

6

Lemonade Stand Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and high-traffic lemonade stand income scenarios

Owner income scenarios

Owner income moves mainly with customer count, ticket size, and cost control. The lean, base, and high cases show how cash flow can scale from first-year traffic to mature demand.

Lean, base, and high cases for owner income planning.

Scenario

Lean CaseLean Case

Base CaseBase Case

High CaseHigh Case

Launch model

This is the lower earnings path if the stand stays near first-year traffic and pricing.

This is the modeled middle path if third-year demand and pricing hold.

This is the stronger earnings path if mature-year traffic and ticket sizes come through.

Typical setup

About 50 to 150 daily customers at $18 to $22 ticket size, with 15.5% COGS and 4.0% variable costs, keeps owner income tight.

About 100 to 250 daily customers at $21 to $25 ticket size, with 14.3% COGS and 3.7% variable costs, supports the core plan.

About 150 to 350 daily customers at $24 to $28 ticket size, with 13.0% COGS and 3.0% variable costs, pushes income to the top end.

Cost drivers

50-150 daily customers

$18-$22 ticket size

15.5% COGS

4.0% variable costs

100-250 daily customers

$21-$25 ticket size

14.3% COGS

3.7% variable costs

150-350 daily customers

$24-$28 ticket size

13.0% COGS

3.0% variable costs

Owner income rangeBefore owner reserves

About $122kLean income

About $625kBase income

About $1.215MHigh income

Best fit

Use this for a cautious first-year view or to stress-test slow traffic.

Use this for budget planning and lender talks once the model reaches year three.

Use this to test upside if the stand scales to mature-year demand and pricing.

!

Planning note: Scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

In the provided model, the business reaches $122k of first-year EBITDA and $1215M in the mature year That is not the same as owner take-home Owner cash comes after reserves, taxes, debt service, reinvestment, and any distributions The model also assumes $273k of first-year payroll and $5,550 in monthly fixed costs

The provided model reaches breakeven in Month 4 and pays back in 14 months That timing depends on daily traffic, AOV, cost control, and fixed-cost load A small temporary stand with lower setup costs may have a different breakeven point, while a larger setup with $965k capex needs more cash discipline

Permits are a cost and timing consideration, but this estimate does not give legal advice Local rules can affect where you sell, what you can serve, and whether event fees apply In the calculator, treat permit costs as fixed setup costs because they reduce early owner take-home before sales volume covers them

Cups sold and price drive the top line, while COGS and fixed costs decide what remains The first-year model uses 50-150 daily customers, $18-$22 AOV, 155% COGS, and 40% variable costs Weather, event access, spoilage, and payment fees can move profit quickly, especially on short selling windows

Increase high-margin sales before adding fixed cost Focus on better locations, weekend/event traffic, tight ingredient buying, and less spoilage In this model, each $18 midweek sale contributes about $1449 before fixed cost recovery, while each $22 weekend sale contributes about $1771 Hold reserves back before paying the owner

About the author

Peter Walsh

Launch Planning Specialist

Peter Walsh is a launch planning specialist at Financial Models Lab who helps online business beginners check whether a business idea is financially realistic by breaking down operating cost estimates into clear, practical planning steps. He focuses on opening and running small businesses, and he explains business costs in a helpful, plain-spoken way without unnecessary jargon.

Choosing a selection results in a full page refresh.