LLC Formation Service Owner Income: $367M Year 1 EBITDA

You’re pricing filings before you know how much cash the owner can safely take out This planning view models a US LLC formation service with $6008 million in Year 1 revenue, $3668 million in Year 1 EBITDA, and breakeven in Month 2 It covers revenue, expenses, reserves, and target owner pay, not tax treatment, legal advice, or guaranteed distributions

Owner income$3.7M-$23.9MNet margin61%-74%Revenue for target pay$6.0M-$32.5MBusiness difficultyMedium

Want the six drivers behind owner income?

1

Formation Volume

706/mo

More filings spread fixed costs and lift take-home; Year 1 implies about 706 formations a month.

2

Net Revenue

$709

Average revenue of about $709 per customer moves straight into profit, so price and mix matter fast.

3

Attach Rate

20%-82%

Bigger attachment on EINs, agreements, and annual reports lifts revenue per lead without equal ad spend.

4

Acquisition Cost

$85

At $85 CAC, lower spend or better conversion protects payback as marketing scales.

5

Service Cost

27.5%

Fewer hours per order and a lower cost load keep labor and pass-through fees from eating the fee.

6

Cash Reserve

$822K

The $12.65K monthly fixed base and the $822K cash floor can slow owner draws even when EBITDA grows.

Want to test your owner pay target?

Owner income calculator

Estimate owner take-home and the gap to your target pay from revenue, margin, costs, reserves, and target pay.

!

Planning note This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

Want to see the owner-income model?

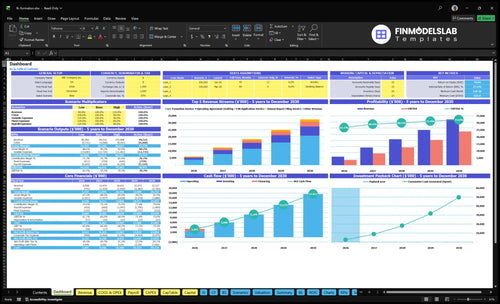

Open the LLC Formation Service Financial Model Template to see the dashboard with revenue, EBITDA, owner-income pool, Month 2 breakeven, Month 3 payback, $822k minimum cash, 7715% IRR, and 7099% ROE. The assumptions tab covers package pricing, hours, attachment rates, marketing budget, CAC, wages, fixed overhead, processing fees, cloud costs, referral commissions, reserves, and owner pay charts.

Owner-income model highlights

Revenue $6008M to $32527M

EBITDA $3668M to $23929M

Month 2 breakeven

Month 3 payback

$822k cash reserve

Does registered agent revenue increase LLC formation service owner income?

Yes—registered agent revenue can raise income for an LLC Formation Service, but only when renewal revenue stays ahead of churn, reminder work, and filing mistakes. In your add-on assumptions, annual report filing attachment rises from 20% in Year 1 to 65% in Year 5, operating agreement attachment from 45% to 65%, and EIN service from 70% to 82%. So the higher lifetime value helps only if servicing cost and error risk stay controlled.

Income upside

Recurring fees smooth cash flow.

Renewals lift customer lifetime value.

Higher attach rates boost revenue.

More add-ons can raise owner pay.

Cost traps

Churn cuts renewal income fast.

Reminders add support workload.

Compliance duty raises error risk.

Fulfillment costs can eat margin.

Are LLC formation services profitable?

Yes, an LLC Formation Service can be profitable when retained service revenue stays above CAC, support labor, software, processing, and referral costs. The source model shows 611% EBITDA margin in Year 1 and 736% in Year 5, but state filing fees paid to government agencies are pass-through amounts, not true revenue. For the setup path, see How To Launch LLC Formation Service?

Profit drivers

611% EBITDA margin in Year 1

736% EBITDA margin in Year 5

Retained fees drive real profit

CAC must stay below revenue

Cost traps

275% listed costs in Year 1

Fixed overhead still comes out

Support labor can compress margin

Filing fees are pass-throughs

How much can an LLC formation service owner pay themselves?

An LLC Formation Service owner can pay themselves only after client filing fees, support payroll, software, marketing, reserves, and reinvestment are covered; in this model, $3.668M of Year 1 EBITDA on $6.008M revenue is profit capacity, not automatic take-home cash. Use What Are 5 Core KPIs For LLC Formation Service? to track whether distributions are safe, because Month 2 needs $822k minimum cash before owner draws.

Pay Comes Last

Cover $12,650 monthly fixed overhead first

Fund $360k Year 1 payroll

Protect $120k marketing spend

Hold pass-through filing fee cash

Safe Draw Rule

Pay from cleared operating cash

Keep $822k Month 2 minimum cash

Reinvest before taking large distributions

Treat EBITDA as pre-draw capacity

Key Takeaways

Completed filings, not traffic, drive monthly revenue.

Add-ons and recurring work lift customer lifetime value.

Lower CAC only helps when margins stay strong.

Overhead and reserves limit owner take-home cash.

Compare low, base, and scale owner-income scenarios

Owner income scenarios

Owner income shifts with customer volume, CAC, and staffing. Lower, base, and high cases show how fast margin improves as the model scales.

Compare owner take-home across modeled operating cases.

Scenario

Low CaseDownside case

Base CaseCore case

High CaseUpside case

Launch model

Owner take-home stays near the first-year model, where revenue is $6.0M and EBITDA is $3.7M.

Owner take-home tracks the Year 3 model, where revenue reaches $18.4M and EBITDA reaches $12.6M.

Owner take-home follows the Year 5 model, where revenue reaches $32.5M and EBITDA reaches $23.9M.

Typical setup

This case assumes Year 1 scale, $85 CAC, $120k marketing, and about 706 implied monthly customers with heavier cost drag.

This case assumes better conversion, $75 CAC, more cross-sell into drafting and EIN work, and a leaner cost base than Year 1.

This case assumes $65 CAC, wider attachment into annual report filing, and a more efficient operating mix at scale.

Cost drivers

Year 1 revenue

$85 CAC

$120k marketing

275% listed costs

early volume

Year 3 revenue

$75 CAC

cross-sell mix

234% listed costs

stronger margin

Year 5 revenue

$65 CAC

service attach rates

192% listed costs

scale efficiency

Owner income rangeBefore owner reserves

$3.7MEarly scale

$12.6MModeled base

$23.9MScale upside

Best fit

Use this to stress test the business before automation and referral volume kick in.

Use this as the main planning case for hiring, reserves, and owner draws.

Use this to test what happens if acquisition stays cheap and add-on services convert well.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

LLC Formation Service Core Six Income Drivers

Monthly LLC formations

Paid LLC filings

Monthly LLC formations is the core volume driver: traffic only matters when it turns into completed paid filings. Based on the modeled revenue and service mix, implied volume is about 706 customers per month in Year 1 and 3,451 per month in Year 5. More completions raise revenue, but only if filing accuracy, state turnaround, and support time stay under control.

Here’s the quick math: more paid filings lift cash in, but rework and slow state processing push cash out. If paid acquisition cost rises faster than gross profit, owner pay shrinks even when lead volume looks strong. Completion rate, not clicks, is what funds profit draw.

Track completion, not traffic

Measure visitor-to-paid-filed conversion, filing error rate, average support minutes per order, and state turnaround days. Those inputs tell you whether added volume is profitable or just busier. If support load rises with volume, hire or automate before rework starts eating margin.

Track paid filings by channel

Watch rework and rejection rates

Cap CAC against gross profit

Use a simple rule: volume helps only when each extra filing adds more gross profit than it costs to win and fulfill. If a channel brings leads but not completions, cut it or fix the intake flow. Cash flow follows completed work, not website visits.

Customer acquisition cost

Customer Acquisition Cost

CAC is what you spend to win one paying customer, and it hits owner take-home before profit shows up. In this model, CAC improves from $85 in Year 1 to $65 in Year 5, even as marketing budget rises from $120k to $400k. That only works if conversion rate, channel mix, and blended order value improve together.

Paid search can still work, but only when each customer brings enough package and add-on margin to cover acquisition and support. If CAC rises faster than gross profit per client, the owner keeps more revenue on paper but less cash in hand. Here’s the quick math: lower CAC means more room for payroll, software, and owner draw.

Track CAC by channel mix

Measure CAC as marketing spend ÷ new paying customers, then split it by channel so you can see what’s really working. Don’t judge ad spend alone; check conversion rate, order value, and add-on attach rate too.

Watch paid search CAC weekly.

Compare package and add-on margin.

Cut channels that dilute profit.

If a channel brings cheap leads but low-value customers, owner income still gets squeezed. The best signal is contribution after CAC, not traffic volume.

Fulfillment and support efficiency

Fulfillment Hours

Labor hours are the margin guardrail here. In this model, LLC formation service hours drop from 350 in Year 1 to 250 in Year 5, operating agreement hours from 250 to 150, and annual report hours from 150 to 110. That means the core workflow falls from 750 hours to 510, so every hour saved protects gross margin and frees cash for owner pay.

What this estimate hides is the labor rate and rework rate. If intake is messy or state rules change, support time rises fast and wipes out the gain from automation. The owner’s income improves only when completion time drops without hurting filing accuracy, because compliance errors create refunds, callbacks, and delayed cash.

Track Hours per File

Measure hours per LLC file, first-pass accuracy, and support tickets per order. Here’s the quick math: if fulfillment work is down to 510 hours by Year 5, then each extra hour of rework cuts directly into owner draw. Better intake forms, document workflows, state checklists, and support scripts keep labor from growing with volume.

Track hours by service type.

Log rework after filing.

Measure tickets per customer.

Test scripts for common questions.

Review state-by-state error rates.

Automation helps, but it does not remove compliance responsibility or customer support needs. The best control is a tight handoff: collect complete intake data, route each state filing through a checklist, and answer repeat questions with one approved script. That protects margin, keeps turnaround steady, and helps more revenue turn into owner income.

Add-on and recurring revenue

Add-on Attachments

Add-ons lift lifetime value, so each filing can earn more than the base formation fee. Here’s the quick math: attachment assumptions rise from 45% to 65% for operating agreements, from 70% to 82% for EIN work, and from 20% to 65% for annual report filings. That helps owner income only if support hours and rework do not rise faster than gross margin.

Recurring work also smooths cash flow between new formations, but it can hide weak economics. If renewal retention is soft, compliance tasks are heavy, or reminder work takes too many labor hours, the extra revenue may not reach profit. Recurring revenue is useful only when churn and fulfillment cost are measured.

Track Attachment, Retention, and Hours

Measure each add-on by order count, attachment rate, labor minutes, and refund or retry rate. Use a simple formula: add-on income = orders × attach rate × price, then subtract support and compliance labor. That shows whether higher take-home income comes from real margin or just more work.

Push reminders, scripts, and bundled offers where they raise attachment without adding much service time. Watch annual report renewals closely, because they can look like easy recurring revenue while still consuming reminder, filing, and customer support time. More attachments help only if delivery stays lean.

Track operating agreement attach rate

Track EIN attach rate

Track annual report renewals

Track support hours per add-on

Track churn and rework

Net revenue per order

Net revenue per order

Net revenue per order is what stays after pass-through state filing fees, so package price can look strong while true margin stays thin. In this LLC formation service, $43,750 in Year 1 modeled formation work before add-ons and about $709 blended revenue per customer after attachment rates show why pricing and mix matter more than traffic alone.

Here’s the quick math: owner income improves when the order price covers preparation, filing workflow, operating agreement drafting, EIN service, and compliance support. If support-heavy customers are priced like simple filings, gross margin falls, cash gets tighter, and the owner has less room for pay.

Price the work, not the filing fee

Track revenue per completed filing, pass-through fees, and labor time per order. Government filing fees are pass-through, not retained margin, so the real test is whether each order covers support hours and rework. Watch attachment rates too: operating agreement at 45% to 65%, EIN at 70% to 82%, and annual report at 20% to 65%.

Measure revenue per completed order.

Split standard and high-touch cases.

Track support minutes and rework.

Price add-ons by workload.

If high-touch clients take more time, raise the tier or add a service fee. That protects take-home income when filing delays, questions, and compliance work push labor cost above the blended price.

Overhead, software, and reserves

Fixed Overhead and Reserves

Fixed overhead and reserve cash decide how much EBITDA turns into owner pay. Monthly fixed overhead is $12,650, or about $151,800 a year, before payroll. Year 1 payroll is $360,000, which is about $30,000 a month. The $822,000 minimum cash in Month 2 stays in reserve, so it is not available for owner distributions.

Here’s the quick math: the business must cover $42,650 a month in baseline fixed load before owner take-home starts to grow. If staffing rises, EBITDA can still look fine while cash stays tight, because payroll and overhead get paid first. Owner income only improves when recurring gross profit beats these fixed costs and the reserve target stays untouched.

Track the cash floor, then pay yourself

Measure each fixed cost line every month and keep reserves separate from draws. Track $6,500 office lease, $1,200 software, $850 insurance, $2,000 legal and accounting, and $1,500 marketing tools, plus payroll growth tied to staffing. If the reserve balance is below the target, hold owner pay until cash rebuilds.

Lease: $6,500

Software: $1,200

Insurance: $850

Legal and accounting: $2,000

Marketing tools: $1,500

Update the forecast before hiring. If payroll rises faster than gross profit, owner take-home slips even when sales are growing.