Medical Necessity Review Owner Income: $185k Salary, $36M EBITDA

You’re planning owner pay in a regulated healthcare service where revenue is not the same as take-home This five-year model shows $814k to $8709M in annual revenue, -$986k to $3579M in EBITDA, Month 29 breakeven, reviewer costs, overhead, reserves, and owner compensation capacity It does not provide clinical guidance, tax advice, legal advice, or payer policy interpretation

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want the six drivers that change owner income?

1

Paid Volume

$814K-$8.7M

More paid reviews and contracts drive the biggest jump in owner take-home across the model.

2

Contract Price

$113K-$144K

Higher monthly contract value lifts revenue per client, so each sale adds more cash without the same sales effort.

3

Reviewer Utilization

12%-8%

Lower physician reviewer fees keep more gross profit after case work and improve what the owner can keep.

4

Case Burden

M29

Harder cases and tighter service levels can slow throughput, so cleaner case mix helps you reach breakeven faster.

5

Client Retention

-$1.273M

Keeping anchor clients in place lowers cash stress and protects the path to payback when growth is uneven.

6

Overhead Control

$288K/mo

Fixed overhead stays a direct drag on owner take-home, so every cut in rent, legal, and software flows through fast.

Want to see the owner income model?

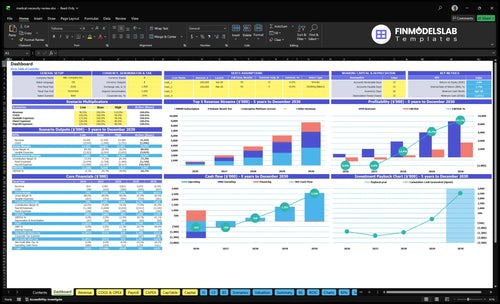

This dashboard in the Medical Necessity Review Service Financial Model Template shows revenue, margin, costs, reserves, and owner take-home assumptions. Planning charts also track revenue from $814k to $8.709M, EBITDA from -$986k to $3.579M, breakeven in Month 29, minimum cash of -$1.273M in Month 28, and payback in Month 52.

Owner-income model highlights

Volume to owner pay

Revenue and EBITDA path

Scenario controls included

Breakeven Month 29

Minimum cash Month 28

Payback Month 52

Does the owner earn more by reviewing cases or managing reviewers?

For a Medical Necessity Review Service, the owner earns more reliably by managing reviewers, because the model already includes a $185k CEO salary and a $250k Chief Medical Officer salary; billable case work only helps if it doesn’t double count labor. Use How To Write A Business Plan For Medical Necessity Review Service? to separate owner labor, credentialing, and reviewer costs before setting contract pricing.

Case Work Pay

Requires proper licensure and specialty fit

Needs credentialing before billable review work

Must not duplicate $435k executive labor

Works best for limited high-complexity cases

Manager Pay

Depends on reviewer network utilization

Protects quality assurance and client retention

Reviewer fees are 12% of Year 1 revenue

Fees fall to 8% by Year 5

Which contract model creates the most stable owner income?

The most stable owner income comes from PMPM—per member per month—because it charges a recurring fee tied to covered lives, not each case. For the Medical Necessity Review Service, the mix shifts from 40% of customers in Year 1 to 60% in Year 5, while volume-based tier work falls from 50% to 30% and the enterprise platform license stays at 10% but rises from $25k to $30k.

PMPM steadies cash

Recurring fee per member

40% to 60% mix shift

Less exposure to uneven case flow

Best for monthly planning

Minimums matter most

Cover reviewer readiness costs

Cover compliance overhead

Cover sales costs

$25k to $30k license helps

How many medical necessity reviews are needed to pay the owner?

You can’t pin this to one universal review count for a Medical Necessity Review Service, because contract size, per-review fee, case complexity, and staffing mix all change the answer. In Year 1, $814k of revenue maps to about 6 average contracts at a $113k weighted monthly contract value, and a $185k CEO salary alone needs about 17 Year 1 average contracts on 81% contribution math. Full company breakeven is much bigger: Year 1 wages are $995k, fixed overhead is $3,456k, marketing is $150k, and breakeven arrives in Month 29.

Owner pay

17 Year 1 average contracts

81% contribution math

$185k CEO salary alone

No single review count fits all

Scale math

6 average contracts in Year 1

$113k weighted monthly contract value

50 average contracts in Year 5

$144k weighted monthly contract value

Key Takeaways

Billable contract volume drives revenue, not inquiries.

Pricing mix shapes owner pay and margin.

Reviewer utilization protects gross margin as scale grows.

Retention and overhead decide how much EBITDA remains.

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income shifts as reviewer fees, cloud/API costs, wages, marketing, and fixed overhead scale with volume. The model moves from -$986k EBITDA in Year 1 to $3.579M in Year 5.

Low, base, and high income cases for a medical necessity review service.

Scenario

Low CaseDownside case

Base CaseBase case

High CaseUpside case

Launch model

This is the downside path where Year 1 ramp keeps EBITDA at -$986k.

This is the modeled path where Year 3 revenue reaches $3.821M and EBITDA turns positive at $493k.

This is the upside path where Year 5 revenue reaches $8.709M and EBITDA grows to $3.579M.

Typical setup

Year 1 uses $814k revenue, 12% physician reviewer fees, 7% cloud/API fees, $995k wages, and $150k marketing against heavy fixed overhead.

Year 3 uses $3.821M revenue, 10% reviewer fees, 5% cloud/API fees, about $1.64M wages, and $400k marketing with positive EBITDA.

Year 5 uses $8.709M revenue, 8% reviewer fees, 3% cloud/API fees, about $2.405M wages, and stronger operating scale.

Cost drivers

reviewer fees

cloud/API fees

wages

marketing

fixed overhead

reviewer fees

cloud/API fees

wages

marketing

staffing mix

reviewer fees

cloud/API fees

wages

marketing

scale efficiency

Owner income rangeBefore owner reserves

Salary only if fundedCash tight

Salary plus modeled profitCore case

Salary plus strong profitScale upside

Best fit

Use this if you want a downside test for slow sales and heavy compliance costs.

Use this as the planning case for budgeting, hiring, and cash control.

Use this to test expansion plans, reinvestment capacity, and stronger contract wins.

!

Planning note: These scenario ranges are researched planning assumptions only, not guaranteed earnings, salary promises, tax advice, or distribution forecasts.

Medical Necessity Review Service Core Six Income Drivers

Paid Review And Contract Volume

Paid Review and Active Contract Volume

Income starts when a review is billed and completed or a contract is active, not when a lead asks for a quote. Here’s the quick math: model revenue rises from $814k in Year 1 to $8.709M in Year 5, and implied average contracts move from about 6 to about 50 on weighted monthly pricing. That volume pays reviewer labor, overhead, marketing, and owner draw.

The risk is simple: onboarding delay or low utilization after staff are hired. If reviews do not start flowing soon after launch, cash gets trapped in payroll and compliance before revenue catches up. No paid work, no owner pay. In this model, volume is the switch that turns fixed cost into profit.

Protect Billable Throughput

Track billable completed reviews, active contracts, and utilization every week. Do not forecast from inquiries, unpaid pilots, or casual consults. Tie each signed client to a start date and expected monthly volume, then compare that to reviewer capacity. One paid review is worth more than a stack of warm leads.

Build the forecast from contract type, monthly fee, and start lag. If staffing is hired before paid work starts, margin drops fast because labor and overhead keep running. Use the ramp from about 6 contracts to about 50 contracts as the operating test, and price staffing to paid start, not signed date.

Track billed reviews weekly

Measure contract start lag

Watch reviewer utilization rates

Block work without billing

Compare volume to payroll

Average Revenue Per Review Or Contract

Average Revenue Per Contract

Average revenue per contract is the mix of PMPM, volume, and enterprise pricing you actually collect, not the quote. Weighted monthly contract value rises from $113k in Year 1 to $144k in Year 5, a $31k or 27% lift. That extra revenue can fund reviewer labor, fixed overhead, and owner pay without adding the same amount of new work.

The risk is underpricing complex cases. If specialty premiums, urgent turnaround, minimums, and enterprise scope are not in the contract, the reviewer still does the work but the owner pays for the extra time out of margin. Track realized price by client type, then compare it with reviewer hours and rework on each account.

Price the Harder Work

Build the model from contract mix, member count, review volume, turnaround terms, and rework hours. The disclosed price ladder shows the spread: $12k to $14k PMPM, $8k to $10k for volume tiers, and $25k to $30k for enterprise. That gap should be captured in the rate card before staffing is set.

Track realized price by client type

Log urgent and specialty hours

Invoice minimums and add-ons

If a case needs more physician time, more QA, or faster turnaround, the contract should charge for it. Otherwise, the same workload looks busy but owner take-home shrinks because labor cost rises faster than billed revenue.

Client Retention And Concentration

Client Retention and Concentration

Recurring contracts make owner income steadier, but concentration can swing the whole plan. If one payer, third-party administrator, or provider-side client is too large, a single lost renewal can wipe out months of margin. With PMPM mix rising from 40% to 60%, revenue gets more predictable and easier to forecast for owner pay.

Here’s the quick math: customer acquisition cost starts at $125k in Year 1 and improves to $9k by Year 5, while marketing spend rises from $150k to $700k. That means lost renewals are expensive to replace. The key inputs are renewal rate, client share of revenue, and contract mix.

Protect Renewal Revenue

Track revenue by client, not just total bookings. Set a cap so no single client can distort cash flow or owner draw. If a procurement delay or onboarding drag pushes a renewal out, the gap hits payroll and margin fast. One clean rule: no client should be big enough to break the forecast.

Use a simple watchlist:

Top client revenue share

Renewal date by account

PMPM vs. volume mix

Days from signed to live

Lost renewal replacement cost

Clinical Reviewer Cost And Utilization

Clinical Reviewer Cost And Utilization

Physician reviewer fees sit at 12% of revenue in Year 1, then 11%, 10%, 9%, and 8% by Year 5. That lifts gross margin before overhead from 88% to 92%, so reviewer efficiency flows straight into owner pay. The catch is simple: specialty match, documentation, and compliance have to stay tight, or the margin gain gets lost in rework and risk.

Here’s the quick math: reviewer cost = revenue × reviewer fee %. If revenue scales and reviewer time is not fully booked, idle time, scheduling gaps, credentialing delays, and low productivity cut take-home even when sales look strong. This driver matters most when case volume is steady and reviewer capacity can be used every day.

Track Utilization Before It Hits Margin

Measure billable reviewer hours, cases per reviewer, credentialing lag, and rework by specialty. Split the forecast by reviewer type, because a bad specialty match can raise labor cost without adding revenue. The main inputs are case volume, reviewer rate, utilization, and the share of cases that need escalation or redo work.

Track billable hours each week

Flag idle time and gaps fast

Route cases by specialty fit

Clear documentation before review starts

Reduce credentialing delays early

Set schedules to demand, not headcount. If utilization slips, the same 12% reviewer cost can feel much larger in cash terms because payroll is paid now, while subscription revenue may arrive later. Better routing and tighter QA protect gross margin and leave more room for owner draw.

Overhead, Compliance, And Operating Leverage

HIPAA-Ready Fixed Overhead

For a medical necessity review service, HIPAA-ready operations are required spend, not optional trim. Fixed overhead is $288k per month for office rent, liability insurance, cybersecurity, legal and compliance, clinical guideline licensing, and software, while payroll climbs from $995k in Year 1 to $2.405M in Year 5. If volume is soft, this cost stack cuts straight into owner pay.

Measure Fixed Cost Coverage

Measure fixed overhead coverage monthly: recurring revenue, gross margin left after reviewer fees, and EBITDA, or earnings before interest, taxes, depreciation, and amortization. Here’s the quick math: once the $288k monthly base is covered, new contract revenue should flow faster to profit because the cost is fixed. That is the operating leverage the model says can lift EBITDA margin to 411% in Year 5. The $250k platform build and $120k database integration only pay back if volume scales.

Case Complexity, Turnaround, And Rework

Case Complexity And Rework

Complex cases cut owner income fast because urgent SLAs, specialist reviews, incomplete records, appeal support, and QA fixes add paid reviewer hours and coordinator time. Even with cloud/API costs at 7% in Year 1 falling to 3% in Year 5, labor rework is the bigger drag. A case priced on simple turnaround can turn underpriced when extra checks consume margin without new revenue.

Price For Turnaround And Documentation Burden

Track case mix, turnaround time, rework minutes, appeal rate, and QA correction rate by client and case type. Then add fees for urgent SLAs, specialist routing, and incomplete documents. If a priced case needs repeated review, it is using reviewer capacity twice, so gross margin falls and owner draw gets squeezed. The goal is simple: charge more for messy work, or refuse it.