How Much Can a Modular LED Panel Systems Owner Make at $46M Sales?

A modular LED panel systems business owner’s income depends less on revenue alone and more on gross margin, payroll, inventory cash, and reinvestment In the researched base case, Year 1 revenue is about $46M with gross profit near $30M before digital advertising, fulfillment, overhead, payroll, taxes, and reserves The model includes a $145,000 annual CEO salary, but additional owner take-home would come from profit distributions only if the company keeps enough cash for inventory, warranties, and growth These are planning assumptions, not guaranteed earnings

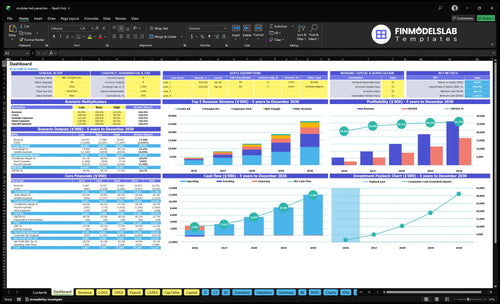

Owner income$145kNet margin48%Revenue for target pay$301kBusiness difficultyMedium

Want the six drivers that move owner income?

1

Monthly Volume

28.5K

Year 1 volume is 28,500 units, so even a small lift in sell-through pushes revenue up fast; if supply slips, the upside vanishes.

2

Unit Price

$161

Year 1 weighted unit revenue is $161, so a richer mix of higher-priced kits lifts take-home more than discounting.

3

Gross Margin

79%

Year 1 direct costs leave about 79% gross margin, so small changes in component cost, waste, or duties flow straight into profit.

4

Pipeline Conversion

18%

Digital ads and 3PL shipping take 18% in Year 1, so better conversion lowers the cost of each sale and frees cash for owners.

5

Operating Overhead

$14K/mo

The business carries about $14K a month of fixed overhead before payroll, and the CEO role is set at $145K, so profit depends on keeping the cost base tight.

6

Reserve Needs

$1.16M

Minimum cash is $1.163M in Month 1, so early gains stay tied up in stock, tooling, and working capital instead of owner draws.

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margins, payroll, taxes, reserves, and reinvestment. It is not guaranteed salary, tax advice, or owner distribution advice.

How do you check owner income in Modular LED Panel Systems?

The Modular LED Panel Systems Financial Model Template organizes dashboard outputs, revenue, margin, payroll, fixed and variable costs, inventory reserve, warranty reserve, and owner pay; open it to refine the assumptions.

Owner-income model highlights

$46M to $268M revenue growth

65% to 66% gross margin

$14k monthly overhead

What gross margin does a modular LED panel business need?

Modular LED Panel Systems needs a very high gross margin to work; the model shows about 662% in Year 1 and 646% in Year 5 after unit COGS and 21% revenue-based COGS. Here’s the quick math: volume hits 28,500 units in Year 1 and 210,000 in Year 5, so even small cost changes move cash fast. For the operating mix behind that, see What Are The 5 KPIs For Modular LED Panel Systems Business?

Unit COGS

$35 Creator Kit

$6 Expansion Pack

$45 Hexagon Pro

$1,250 Mini Triangle

Cost control

$2 Flex Connector

Chipsets and PCB fabrication matter

Freight, testing, and duties add up

Rework and waste hit take-home margin

Can a modular LED panel business support an owner salary?

Yes, Modular LED Panel Systems can support an owner salary in the provided model because it includes a $145,000 CEO salary from Month 1; for setup depth, see How To Write A Business Plan For Modular LED Panel Systems?. But that is planned payroll, not proof of cash availability if sales ramp slower than unit production.

Pay Capacity

CEO salary: $145,000 from Month 1

Year 1 revenue: $45.865M

Gross profit: about $30.4M

Fixed overhead: $168,000 annually

Cash Watchouts

Founder draw comes after expenses

Salary is an operating cost

Customer acquisition runs 12% of revenue

3PL and shipping run 6% of revenue

How much revenue does a modular LED panel business need to pay the owner?

There isn’t one revenue number that pays the owner for Modular LED Panel Systems. Here’s the quick math: owner cash = revenue × contribution margin minus $168k fixed overhead, $270k payroll, and reserves, so top line alone won’t tell you the answer. The provided Year 1 figures show $45,865M revenue, 662% gross margin, and 18% variable selling and fulfillment cost, but closing rate (the share of leads that buy), average order value, inventory reserve, and warranty reserve decide what the owner actually takes home.

Pay math

$168k fixed overhead

$270k payroll listed

$145k CEO pay inside payroll

Revenue needs margin, not just size

Cash filters

18% variable selling and fulfillment cost

Closing rate changes cash fast

Inventory reserve cuts owner pay

Warranty reserve cuts owner pay

Key Takeaways

Gross margin drives owner pay more than top-line growth.

Volume helps only when defects stay under control.

Bigger orders raise income if quoting covers complexity.

Cash reserves limit withdrawals during fast growth.

Compare low, base, and high owner-income outcomes

Owner income scenarios

Owner income shifts fast as unit volume, price mix, and payroll scale from launch to mature production. These cases show what the business can support at three operating stages.

Compare low, base, and high owner income at three scale points.

Scenario

Low CaseEarly scale

Base CaseGrowth scale

High CaseMature scale

Launch model

Modeled low-income path using Year 1 scale and operating profit before taxes and reserve set-asides.

Modeled growth path using Year 3 scale and operating profit before taxes and reserve set-asides.

Modeled mature path using Year 5 scale and operating profit before taxes and reserve set-asides.

Typical setup

Revenue is $4.587M on 28,500 units, 66.2% gross margin, $168k fixed overhead, and $270k listed payroll, with $145k CEO pay in the stack.

Revenue is $12.944M on 88,000 units, 65.8% gross margin, $168k fixed overhead, and $395k listed payroll.

Revenue is $26.750M on 210,000 units, 64.6% gross margin, $168k fixed overhead, and $520k listed payroll.

Cost drivers

Creator Kit volume

12% ad spend

6% shipping

$168k fixed overhead

$270k payroll

Product mix shift

10% ad spend

5% shipping

$168k fixed overhead

$395k payroll

Higher volume

8% ad spend

4% shipping

$168k fixed overhead

$520k payroll

Owner income rangeBefore owner reserves

$145k - $2.21MEarly scale

$145k - $7.53MGrowth scale

$145k - $16.51MMature scale

Best fit

Use it to test launch-month pay if sell-through is slow.

Use it for a normal growth year with steadier demand and staffing.

Use it to size founder pay if volume and repeat orders stay strong.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Modular LED Panel Systems Core Six Income Drivers

Average Project Value

Average Project Value

If most orders sit near the $29 entry point, owner income stays thin. The model’s Year 1 weighted unit revenue is about $161, so larger configured systems matter when they lift revenue per order without adding too much custom work, shipping, or support.

Here’s the quick math: a $299 system, multi-room bundle, or repeat facility order can bring more cash in from the same customer count. That only helps take-home pay if pricing covers design time, freight, and warranty risk; otherwise, extra complexity eats the added gross profit.

Track mix, not just sales count

Measure average order value, product mix, and quote-to-close rate by order type. Watch how many orders land at $29, how many at $299, and how often bundles or commercial packages increase revenue per customer.

Keep the lift clean. If custom quoting, support tickets, or component mix start rising faster than order value, owner profit can fall even when revenue grows. Price for design time, shipping, and warranty exposure before you approve larger builds.

Track revenue per order weekly

Separate bundle and custom quotes

Log support time per project

Flag repeat facility orders fast

Operating Overhead

Operating Overhead

This fixed-cost floor is $14,000 a month, or $168,000 a year, covering design studio rent, cloud hosting, software, liability insurance, legal and IP services, utilities, and internet. It sits outside COGS, advertising, fulfillment, shipping, and payroll, so slow sales hit cash fast; owner pay feels safe only after monthly sales cover that overhead and still leave profit.

One clean rule: when revenue rises, this base gets spread over more units, so profit can scale fast. When sales miss plan, the same $14,000 still has to get paid, and owner draws should wait until the business clears that gap.

Keep the Fixed Base Tight

Track fixed overhead by line item and compare it to monthly sales in a rolling forecast. The key inputs are revenue, gross margin, and cash timing; if a month slips, cut nonessential spend fast and delay owner pay until overhead is covered again.

Watch the big buckets first: rent, software, hosting, insurance, legal, utilities, and internet. If any one line creeps up, it raises the sales level needed before pay feels safe.

Gross Margin

Gross Margin

Gross margin is the cash left after direct product costs, before rent, ads, payroll, and owner pay. For modular LED panel systems, the model puts Year 1 at 662%, with $586,750 in unit COGS and 21% revenue-based COGS. That means sourcing, freight, and defect control move operating profit fast. Here’s the quick math: every margin point kept or lost hits take-home income directly.

This margin sits on LED chipsets, PCB fabrication, housings, power supplies, controllers, packaging, heatsinks, and connectors. If freight, duties, rework, waste, or warranty claims rise, the owner feels it before overhead is covered. In this model, gross margin is the main take-home lever, because it changes how much cash is left for the business and the owner.

Hold Unit Cost Line

Track unit COGS by part, not just total spend. Split out chipsets, PCBs, housings, power supplies, controllers, packaging, heatsinks, connectors, freight, and duties, then compare each build against the target $586,750 unit COGS base and the 21% revenue-based COGS layer. If one part slips, gross profit drops before any overhead is paid.

Test sourcing and standardization first. Use the same specs where you can, then watch rework, waste, and warranty claims each month. If defect rates rise, the owner’s draw gets squeezed even when revenue looks fine. The right control is simple: price to cover direct cost, then review gross margin by product mix every month.

Cash Reserves

Cash Reserves

Cash reserves are the money held back for inventory, supplier deposits, replacement parts, rework, warranty claims, product development, and growth stock. That cash is not owner income. As unit volume scales from 28,500 units in Year 1 to 210,000 units in Year 5, more cash gets tied up in working capital, so owner take-home usually runs below accounting profit.

Do not confuse net income with cash available for distribution. The model already includes revenue-based COGS items like testing compliance, safety certification, inventory insurance, procurement fees, customs brokerage, and logistics surcharge, but reserve timing still matters. When shipments rise, cash needs can grow faster than reported profit, so the owner draw has to stay conservative.

Track the cash cushion

Track reserve needs with a simple cash map: inventory on hand, supplier deposit timing, warranty claims, and rework cost. Here’s the quick math: Year 1 averages about 2,375 units per month, while Year 5 averages about 17,500 units per month. That scale jump means the reserve target should rise with production, not with last month’s profit.

Set owner pay after the reserve check, not before it. Test whether cash still covers replenishment, replacement parts, and product development after each production wave. If stock builds faster than sales or claims rise, hold distributions until the cash buffer catches up.

Monthly Project Volume

Monthly Unit Volume

Monthly unit volume is the number of modular LED panel units shipped each month. It rises from 28,500 units in Year 1 to 210,000 units in Year 5, or about 2,375 to 17,500 units per month. More volume spreads fixed overhead across more units, so owner take-home can improve if added output does not lift defects, rework, or late shipments.

The main inputs are assembly labor, supplier lead times, customization complexity, calibration, compliance testing, and installation coordination. If any one of those slips, higher volume can turn into more warranty work and support cost. So the real win is not just more units; it is more clean units shipped on time.

Track Flow, Not Just Output

Track units started, units finished, first-pass yield, and on-time ship rate each month. Compare actual output to the scale points of 2,375 and 17,500 units per month. If output rises but defects or support tickets rise faster, volume is hurting margin, not helping it.

Keep the process tight. Standardize common builds, limit custom options that slow calibration, and build time buffers around supplier delays and install scheduling. That helps volume absorb overhead instead of creating overtime, rework, and cash pressure.

Measure labor hours per unit.

Track supplier lead-time misses.

Log defects and returns weekly.

Separate ship dates from install dates.

Sales Pipeline Conversion

Sales Pipeline Conversion

A tighter pipeline makes owner pay steadier because revenue shifts away from one-off consumer demand and toward qualified commercial buyers, contractors, designers, and facility managers. Year 1 digital advertising and influencers are 12% of revenue, then fall to 8% by Year 5, so weak lead quality can burn cash fast. Strong conversion also helps repeat orders, which smooths monthly sales.

Here’s the quick math: if quote close rate rises and average order value holds up, the same sales team can generate more revenue with less wasted follow-up. What this driver hides is sales-cycle drag; slow quotes can delay cash even when demand is real. Track quote close rate, cost per acquired customer, repeat order rate, and average order value by segment.

Track Qualified Lead Quality

Measure lead source by customer type, then cut spend where intent is weak. A good mix should show higher closes from commercial accounts and fewer sales hours wasted on small, low-fit inquiries. One clean rule: if a channel does not improve close rate or repeat orders, it is too expensive.

Track close rate by segment

Watch CAC by channel

Compare repeat order rate

Review average order value monthly

Use the funnel to guide inventory too. Better forecasts from qualified buyers mean cleaner purchasing, fewer rush orders, and less dead stock. That keeps gross profit more predictable and helps protect owner draw in slower months.