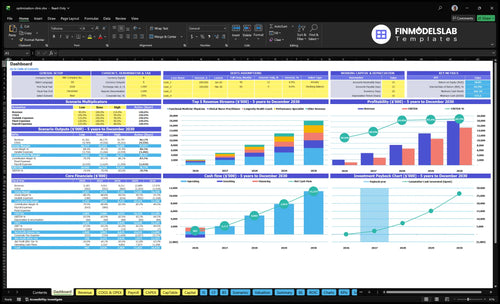

How Much Health Optimization Clinic Owners Make At $218M Year 1 Revenue

A health optimization clinic owner’s income depends on what is left after clinical costs, payroll, overhead, debt, taxes, reserves, and growth spend In these researched assumptions, Year 1 revenue is $218M, gross margin after lab and consumable costs is 88%, and known non-payroll overhead is $25,900 per month That leaves about $142M before most payroll, taxes, debt, reserves, and owner distributions, so it is not the same as owner take-home By Year 5, revenue reaches $1798M and gross margin rises to 91%, but owner pay still depends on staffing and reinvestment choices

Owner income$1.42MNet margin50%→84.5%Revenue for target pay$2.18MBusiness difficultyHard

Want to test your clinic owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from monthly revenue, gross margin, labor, overhead, reserves, debt, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margin, payroll, reserves, debt, and timing.

Want the six main income drivers?

1

Patient Volume

$2.2M-$18.0M

Year 1 revenue is $2.183M and Year 5 is $17.976M, so qualified patient flow is the biggest swing in owner take-home.

2

Program Pricing

$250-$2.5K

Treatment prices span $250 to $2,500, so a better mix toward higher-ticket visits lifts revenue without the same fixed cost.

3

Provider Utilization

30%-85%

Utilization moves from 30%-45% up to 75%-85% across providers, and every empty slot is lost income.

4

Contribution Margin

80%-85%

Direct plus variable costs fall from 20.5% of revenue in Year 1 to 15.5% in Year 5, which lifts contribution fast.

5

Fixed Overhead

$25.9K/mo

Fixed overhead is $25.9K a month, so rent, software, insurance, and admin need tight control to protect cash.

6

Recurring Care

40-120/mo

Monthly treatment counts stay steady by role, so retention and follow-up care decide whether patients become repeat revenue.

Want to check owner income in the Health Optimization Clinic model?

What health optimization clinic profit margin matters most?

Net margin matters most for a Health Optimization Clinic, because 88% to 91% gross margin can still shrink fast once $25,900 monthly overhead and variable spend hit the P&L; see How Increase Health Optimization Clinic Profits?. Gross margin is strong after diagnostic labs and consumables, but net margin tells you if the clinic actually keeps cash.

Gross margin

88% in Year 1

91% in Year 5

After diagnostic labs and consumables

Strong, but not the full picture

Net margin drivers

85% Year 1 variable costs

65% Year 5 variable costs

$25,900 monthly fixed overhead

Watch lab fees, payroll, rent, and compliance

How much can a health optimization clinic owner pay themselves?

For a Health Optimization Clinic, the owner can pay themselves only after full payroll, reserves, taxes, debt, and reinvestment are funded; see How To Launch Health Optimization Clinic? for the launch context. Year 1 revenue is $2.18M, but known non-payroll costs leave about $1.42M before payroll, so that is the ceiling before staff pay and other required cash needs.

Owner Pay Math

$2.18M Year 1 revenue

12% COGS equals about $262k

8.5% marketing and processing equals $185k

$25,900 monthly fixed overhead equals $311k

Pay Rules

Pay salary through payroll first

Take draws only from surplus cash

Keep reserves for slow months

Protect growth capital before distributions

Is an owner-operated or provider-led wellness clinic more profitable?

For Health Optimization Clinic, an owner-operated model often looks more profitable early because the owner’s clinical time replaces hired labor. But that can hide the real cost of work, burnout, and weak delegation; the provider-led model adds payroll, including a $260,000 Medical Director, yet it scales capacity from 30%–45% in Year 1 to 75%–85% by Year 5. So the better choice depends on whether you want near-term cash flow or a larger, more transferable business.

Owner-operated model

Lower early payroll burden

Owner labor can boost cash flow

Burnout risk rises fast

Harder to delegate and scale

Provider-led model

Grows from 8 to 31 roles

Capacity rises to 75%–85% by Year 5

$260,000 Medical Director adds fixed cost

Better for compliance and enterprise value

Key Takeaways

Conversion quality drives revenue more than raw leads.

Higher program mix lifts revenue per booked treatment.

Strong margins depend on controlled lab and supplement costs.

Overhiring and fixed rent can crush early cash flow.

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income moves with treatment volume, pricing, staffing, and fixed overhead. These cases show the launch, scale, and mature paths side by side.

Low, base, and high cases help you see how the clinic's income changes as volume and staffing grow.

Scenario

Low CaseLaunch case

Base CaseScale case

High CaseUpside case

Launch model

This is the Year 1 ramp case with lower owner income while the clinic builds volume.

This is the Year 3 modeled case with stronger, steadier owner income as the clinic scales.

This is the Year 5 upside case with the strongest modeled owner income.

Typical setup

Year 1 revenue is $2.183M with $1.092M EBITDA, 88% gross margin, and still-heavy fixed overhead as the team and patient flow ramp up.

Year 3 revenue reaches $8.211M with $6.733M EBITDA, near 89% gross margin, as staffing and treatment load spread fixed costs better.

Year 5 revenue reaches $17.976M with $15.189M EBITDA and about 91% gross margin, but take-home still drops after full payroll, reserves, debt, taxes, and reinvestment.

Cost drivers

Treatment volume

pricing

lab and supplement costs

marketing spend

fixed payroll

Treatment mix

pricing growth

capacity use

lower unit costs

added payroll

Higher volume

premium pricing

fuller capacity

payroll growth

reinvestment needs

Owner income rangeBefore owner reserves

$1.1MLaunch income

$6.7MMidcase income

$15.2MUpside income

Best fit

Use this to test a slower ramp, weaker pricing, or tighter capacity use.

Use this as the core planning case for owner review and operating plans.

Use this to test a strong scale-up with fuller capacity and higher pricing.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Health Optimization Clinic Core Six Income Drivers

Qualified Patient Volume And Program Conversion

Qualified Consult Conversion

Qualified patient volume is the revenue base here: the clinic’s monthly billable activity is modeled at 252 treatments in Year 1 and 2,098 in Year 5. That volume drives income because each booked treatment feeds the fee-for-service model, and weak consult-to-program conversion leaves paid provider time unused.

Here’s the quick math: if the clinic is filling consults that can’t convert, cash stalls even when lead flow looks busy. Better conversion of financially qualified consults lifts revenue and owner pay without adding rent, while poor conversion keeps fixed overhead stuck at $25,900 per month.

Track Qualified Close Rate

Measure consult-to-program conversion, not raw leads. The inputs that matter are qualified consults, booked treatments, average revenue per treatment, and provider capacity. The model’s monthly revenue base starts at $181,900 and scales with volume, so every extra converted consult should be tied to a booked, billable plan.

Watch for capacity waste: if provider hours are paid but not filled, gross profit drops fast. A simple control is to review which consults convert into a paid program, then tighten intake, pricing, and follow-up so the clinic improves cash flow before it hires more staff or takes more space.

Provider Utilization And Staffing Efficiency

Provider Utilization

Booked provider hours are the bridge between payroll and revenue. In Year 1, utilization sits at 30% to 45%, so a lot of paid capacity is still idle. By Year 5, 75% to 85% utilization turns more of each salary dollar into billable output. That gap matters for owner pay, because weak utilization raises payroll cost before revenue catches up.

The pressure point is staffing mix: provider roles grow from 8 in Year 1 to 31 in Year 5. If hiring runs ahead of demand, cash flow tightens and profit can lag even when the clinic looks busy. Count the owner’s labor as an economic cost too, even if early draws are small, so margins reflect real capacity cost.

Track Booked Hours

Track booked hours / available hours by role, not just visit count. Separate physicians, performance specialists, and other provider types, since their utilization targets differ. A simple monthly target sheet should show paid hours, booked hours, and revenue per booked hour. One clean rule: if booked hours don’t rise faster than payroll, owner income won’t scale.

Use the forecast to pace hiring. Add roles only when the next 30 to 60 days of booked demand can support them, and keep the owner’s hours in the model at market value. That keeps the clinic from hiding underused labor inside growth, and it protects take-home profit when demand softens or onboarding takes longer than planned.

Average Program Revenue

Average Program Revenue

The clinic’s income here is set by price mix, not just visit count. Year 1 blended revenue is about $722 per billable treatment, and Year 5 is about $714, so even small discounting or a shift toward lower-priced care can cut owner take-home fast.

Here’s the quick math: revenue per slot equals total program revenue divided by billable treatments. With $2,500 physician programs, $1,200 performance services, $450 dietitian care, $400 nurse practitioner care, and $250 coaching, the mix has to fit value, capacity, market position, and compliance. Underpricing high-value programs can erase margin.

Protect the Blended Price

Track blended revenue per billable treatment every month, then split it by service line. If the mix drifts toward lower-priced visits, the owner needs more volume just to stand still, and that pushes pressure onto payroll, cash flow, and profit draw.

Measure revenue per treatment by service.

Set discount limits and approval rules.

Watch mix against provider capacity.

Price for value, not just fill rate.

Forecast owner pay from net mix.

Fixed Overhead Control

Fixed Overhead Control

Fixed overhead is the monthly cost that stays on even before a visit is booked: $25,900 a month, including $15,000 rent, $3,500 for the health platform and electronic medical record (EMR) licensing, $2,800 malpractice insurance, $1,400 utilities and internet, $2,000 professional services, and $1,200 maintenance and security. That load is 142% of Year 1 monthly revenue, so it cuts owner take-home fast during ramp-up.

Here’s the quick math: if monthly revenue is below $25,900, the clinic is still paying overhead from cash on hand or owner capital. By Year 5, overhead falls to about 17% of monthly revenue, which is much easier to absorb. Premium rent is the main break-even risk.

Hold Overhead Flat While Revenue Catches Up

Track each fixed line monthly: rent, EMR, insurance, utilities, professional services, and security. The owner should model lease terms and software contracts against monthly billable volume, because a bad location or overbuilt tech stack can lock in cost before patient flow is stable.

Keep rent tied to realistic early revenue, not peak hope. If the clinic cannot cover $25,900 from recurring cash flow, delay upgrades, renegotiate terms, or keep the footprint light. One expensive lease can erase owner pay.

Retention And Recurring Care

Recurring Patient Care

Repeat testing, follow-up consults, memberships, and referrals turn one-time visits into revenue that is easier to forecast. No retention rate is given, so model it as an editable assumption. The business gets cleaner cash flow when returning patients reduce paid acquisition, which starts at 60% of revenue in Year 1 and falls to 40% by Year 5.

This driver works only when recurring care matches real patient need. If one patient comes back for labs, a review, and a plan update, the clinic gets more billable touchpoints without starting from zero each time. One clean return is worth more than three weak leads.

Track Return Revenue, Not Just Visits

Measure repeat-test rate, follow-up consult count, membership attach rate, and referral share by cohort. Use those inputs to forecast monthly recurring revenue and owner draw. If recurring care does not cover practitioner time, lab cost, and admin time, it is not helping profit, even if volume looks busy.

Track first-to-second visit conversion.

Separate membership and non-membership revenue.

Price follow-ups by real clinical need.

Avoid artificial lock-ins and churn risk.

Lab And Intervention Gross Margin

Lab and Intervention Gross Margin

This driver is the money left after labs, supplements, consumables, supplies, practitioner time, and vendor fees. In Year 1, diagnostic lab fees run at 75% of revenue, and medical-grade supplements and consumables at 45%; by Year 5, those fall to 55% and 35%. Gross margin still improves from 88% to 91%, so more of each dollar can reach owner pay.

Here’s the quick math: at $100 of revenue, gross profit is $88 in Year 1 and $91 in Year 5, before fixed overhead. That 3-point lift matters because direct costs scale with volume. What this hides: margin gains do not matter if the intervention is not clinically right or if pricing drifts into unethical territory.

Track Cost Per Case

Measure each program by lab cost, supplement cost, consumables, and practitioner minutes. Compare those costs to collected revenue by service line, not just at the clinic level. If one protocol burns more vendor spend than planned, owner income drops even when bookings stay strong.

Track direct cost by program.

Review gross margin monthly.

Watch practitioner time per case.

Test vendor pricing each quarter.

Cut waste, not needed care.

Keep pricing tied to value and clinical need. Standardize kits where it makes sense, but do not push cheaper inputs if they weaken outcomes. A 1-point gross margin gain adds $1 per $100 of revenue, which helps fund owner pay without adding more volume.