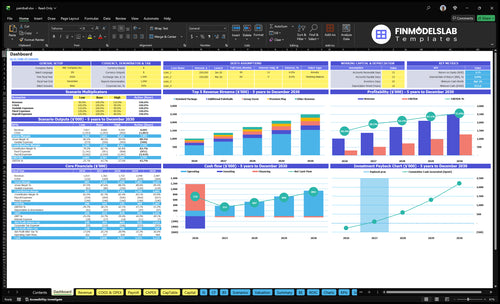

How Much Paintball Business Owners Make: $298K Year 1 EBITDA

You’re estimating owner income from a paintball field, not a fixed paycheck This 5-year model uses 19,000 Year 1 player visits, $1015M Year 1 revenue, payroll, facility costs, insurance, maintenance, reserves, and owner role assumptions to frame take-home before taxes and personal debt

Owner income$298kNet margin29.4%Revenue for target pay$1.015MBusiness difficultyHard

Want to estimate your paintball owner take-home?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. The model starts from Year 1 at 19,000 visits, about $53.42 revenue per visit, $15,850 monthly fixed costs, about $289,500 annual payroll, a $615,000 minimum cash need, and about a 23-month payback. It is not guaranteed salary, tax advice, or owner distribution advice.

Which six drivers move paintball owner income most?

1

Player Volume

19K-45K

More visits lift every revenue line, and the model grows from 19K to 45K yearly visits.

2

Spend Per Visit

$53-$55

A higher spend per visit adds fast, especially as paintballs, rentals, and add-ons stack on each player.

3

Group Events

3K-7K

Group bookings add steady demand, with visits rising from 3K to 7K over the model period.

4

Direct Margin

16%-19%

Keeping direct and variable cost rates near 16% to 19% protects gross cash and owner profit.

5

Labor Load

$290K-$482K

Payroll climbs from about $290K to $482K, so staffing control matters as volume grows.

6

Fixed Overhead

$16K/mo

The $15,850 monthly fixed base, plus the $615K cash floor, sets how much profit becomes usable income.

Want to see the Paintball income forecast?

Yes—open the Paintball Financial Model Template to see revenue, EBITDA, cash, payback, IRR, ROE, and owner income. Charts show revenue growth from $1.015M to $2.487M and EBITDA from $298K to $1.267M, then keep it as a planning aid.

Owner-income model highlights

Owner income and cash

Player volume and pricing

Costs, capex, reserves

Scenario testing built in

Is a paintball business profitable year round?

Paintball can be profitable year round, but only if booked volume stays steady; the plan grows from 19,000 Year 1 visits to 45,000 Year 5 visits, with EBITDA rising from $298K to $1267M as provided. Indoor fields, leagues, parties, and booked groups help smooth demand, but lease, insurance, and utilities still run in slow months, and an owner-operated field cuts manager cost but adds workload.

What drives profit

Keep bookings consistent

Use indoor play to cut weather risk

Fill weekdays with group events

Run leagues to smooth demand

What keeps it tight

Fixed lease costs keep running

Insurance stays due in slow periods

Utilities do not pause

Owner-operated fields add workload

What costs most affect paintball field profit margin?

Paintball profit margin gets squeezed first by payroll, lease, and paint inventory, and the cost mix is clear in How Much Does It Cost To Open And Launch Your Paintball Recreational Facility?. In Year 1, payroll is $2,895K, fixed costs run $15,850 per month, and direct plus variable costs total 190% of revenue. The biggest leaks are paintballs at 100%, CO2/HPA (air refills) at 30%, equipment maintenance at 40%, and digital marketing at 20%.

Fixed cost pressure

Payroll is the biggest Year 1 hit.

$2,895K shows the labor load.

$15,850 monthly fixed costs stay on.

Lease, insurance, utilities, and repairs add up fast.

Variable cost leaks

Paintballs take 100% of revenue.

CO2/HPA (air refills) adds 30%.

Equipment maintenance adds 40%.

Small leaks cut EBITDA and owner distributions.

How much revenue does a paintball field need?

A Paintball field needs enough revenue to cover direct costs, payroll, and fixed facility costs before the owner can take a draw. In the model, break-even lands by Month 2, and at an average of $53.42 per visit, every 1,000 extra visits adds about $53.4K in revenue before costs.

Core math

Cover direct costs first.

Then cover payroll.

Then cover fixed facility costs.

$53.42 average per visit drives scale.

Owner pay

Break-even happens by Month 2.

Owner draw comes after reserves.

Debt service can eat cash fast.

Repeat player volume matters most.

Key Takeaways

Attendance growth drives revenue from 19,000 to 45,000 visits.

Group events improve utilization and add schedule control.

Payroll rises to $482K, so labor discipline matters.

Minimum cash hits $615K, so reserves come first.

Compare lean, base, and strong paintball owner income outcomes

Owner income scenarios

Owner income moves fast in this model because visit volume, add-on sales, and staffing costs all scale together. The low, base, and high cases map to Year 1, Year 3, and Year 5 operations.

A quick read on income from opening year to mature year.

Scenario

Low CaseOpening year

Base CaseYear 3 run-rate

High CaseYear 5 upside

Launch model

This is the lower earnings path: Year 1 volume supports about $1.015M revenue and $298k EBITDA.

This is the modeled middle path: Year 3 volume lifts revenue to about $1.723M and EBITDA to $725k.

This is the stronger earnings path: Year 5 volume reaches about $2.487M revenue and $1.267M EBITDA.

Typical setup

It reflects 19,000 visits, a 29.4% EBITDA margin, $289.5k payroll, and $190.2k in fixed costs while the site builds repeat traffic.

It reflects 32,000 visits, a 42.1% EBITDA margin, $412k payroll, and steady add-on sales from paintballs, concessions, merch, and equipment.

It reflects 45,000 visits, a 50.9% EBITDA margin, $482k payroll, and higher revenue from paintballs, concessions, merch, and equipment sales.

Cost drivers

Visit count

extra paintball sales

payroll scale

lease and utilities

Visit mix

add-on sales

referee staffing

marketing spend

Visit growth

premium play mix

add-on sales

full staffing

fixed overhead

Owner income rangeBefore owner reserves

$298kYear 1 base

$725kModeled base

$1.267MUpside path

Best fit

Use this to test early demand, staffing, and cash pressure in the opening year.

Use this as the most balanced planning case for budgeting and lender conversations.

Use this to test what happens if demand, add-ons, and capacity all stay strong.

!

Planning note: These are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions. Actual owner take-home depends on debt service, taxes, reserves, and reinvestment.

Paintball Core Six Income Drivers

Player Volume

Player Volume

Player volume is the main top-line engine. With 19,000 visits in Year 1 and about $53.42 in average spend per player, revenue is roughly $1.01M before costs. By Year 5, visits rise to 45,000, so the owner’s income depends on turning those extra visits into cash without running into labor, safety, parking, or field limits.

Here’s the quick math: each 1,000 visits adds about $53,420 at Year 1 spend, and the 26,000-visit jump from Year 1 to Year 5 adds about $1.39M in gross revenue. Higher volume helps cover the $15,850 monthly fixed facility load, but weak weather, empty weekdays, or too few booked slots can leave owner pay thin.

Track slot fill

Measure visits by day, slot, and channel. Weekend traffic, repeat players, leagues, location, and booking capacity drive utilization, meaning how many available play slots actually sell. If bookings climb but refs, parking, or safe play limits cap throughput, the extra revenue may not reach the owner as profit.

Use a simple control list: watch paid visits, show-up rate, group mix, and weather cancellations. Protect cash with deposits and set hard capacity caps before overtime or safety issues start to eat the margin.

Track visits by daypart.

Separate groups, leagues, and walk-ins.

Watch weather and no-show patterns.

Stop selling past field capacity.

Average Spend Per Player

Average Spend Per Player

Average spend per player is the main ticket size for each visit. In the model, it is $5,342 in Year 1 and $5,527 in Year 5, driven by standard packages, group events, premium play, extra paintballs, concessions, merchandise, and equipment sales. The business only pays the owner more if this spend stays high without forcing heavy discounts.

Here’s the quick math: more spend per player lifts revenue per visit, so fixed costs like lease, utilities, and payroll get covered faster. But if local competition pushes prices down, the higher ticket can vanish into lower margin. Price mix matters more than sticker price.

Track Spend Mix And Discount Pressure

Measure average spend per player by source: admission, rentals, paint, air fills, upgrades, memberships, concessions, and merchandise. Then compare booked groups, walk-ins, and premium play so you can see which segment carries the best margin. Track spend per visit, not just headcount.

Watch add-on attach rate.

Test price changes by segment.

Track discount rate weekly.

Protect margins on paint and rentals.

If spend rises but demand falls, cash flow weakens fast. The owner’s take-home improves when higher prices hold, add-ons stay strong, and the field keeps full sessions without extra labor or refund pressure.

Labor Efficiency And Owner Role

Labor Cost and Owner Pay

Labor is the gatekeeper for owner income. The model states Year 1 payroll at $2895K and Year 5 at $482K, with an $80K general manager, $55K head referee, $70K referees, $30K front desk, $32K maintenance, and $225K marketing coordinator. If the owner runs the fields, the manager role can become owner working income; if not, payroll must be paid before any draw.

The key test is EBITDA after reserves—earnings before interest, taxes, depreciation, and amortization, after cash set-asides. More referee staffing can protect service and safety, but it also pushes payroll up. Owner pay improves only when labor hours rise slower than visits and booked events; if staffing grows ahead of demand, cash gets tied up and distributions shrink.

Control Labor by Shift and Volume

Track labor by role, event type, and daypart, not just as one total. Use player volume, group bookings, and weekend traffic to set referee, front desk, and maintenance schedules. If the owner is active, replace the GM salary with a clear owner draw and measure whether the same work gets done without adding hidden overtime or service gaps.

Keep the labor plan tied to booked visits and cash reserves. Compare payroll growth from $2895K to $482K against the rise in referee staffing, and only add headcount when it protects revenue or safety. Passive ownership means the business pays management first, then leaves owner distributions dependent on EBITDA after reserves.

Private Parties And Group Events

Private Parties And Group Events

Booked groups turn dead time into paid time. Here, group event visits rise from 3,000 in Year 1 to 7,000 in Year 5, and price per visit moves from $35 to $39, or about $105,000 to $273,000 in base group revenue before add-ons.

This driver helps owner income because deposits, set start times, and planned headcount improve cash flow and cut messy overtime. It also lifts add-on sales from birthdays, team events, and bachelor parties. The risk is simple: if group slots do not fill reserved capacity, the business still carries staffing and field costs but keeps less of the cash.

Track Slot Fill and Add-On Rate

Measure group visits, average group price, deposit collection, and add-on spend per booking. That tells you whether each party is paying enough to cover labor, gear wear, and the reserved field time. A strong booking system should show which dates sell out, which event types convert best, and where pricing can move from $35 toward $39 without hurting demand.

Use birthdays, team events, and bachelor parties to fill weak weekdays and early slots. One clean rule: if a group needs extra staff but does not raise deposit coverage or add-on sales, it can lower owner pay even when revenue looks good. The goal is simple—fill capacity, protect schedule control, and avoid overtime.

Paint, Rental, And Equipment Margin

Paint, Rental, And Equipment Margin

Additional paintballs are a big revenue add, with $150K in Year 1 and $270K by Year 5. But Year 1 paint cost is 100% of that revenue, plus 30% for CO2/HPA refills and 40% for equipment maintenance, so this line can look busy while gross profit stays thin. If pricing is loose, the owner’s take-home drops fast.

The key inputs are paint sold, refill use, marker upkeep, mask replacement, air systems, and consumables. Here’s the quick math: margin only improves as those cost rates decline over the model period, so the same sales can support more fixed overhead and owner draw later. What this hides is waste, breakage, and overfill, which can erase the gain.

Track Cost Per Player

Measure paint use, refill counts, and repair cost by package, field, and event type. Split add-on economics into paint, air, and wear-and-tear so you can see which offer makes money and which one just adds activity. If a bundle uses heavy paint or extra refills, price it separately instead of burying it in admission.

Run a weekly check on revenue, direct cost, and gross profit for every add-on. If marker upkeep, mask replacement, air systems, or consumables run above plan, tighten usage rules, raise bundle prices, or cut waste fast. That protects cash for rent, payroll, reserves, and owner pay.

Facility Costs And Reserves

Facility Costs And Reserves

Facility overhead sets the floor for owner pay. Fixed facility cost is $15,850 per month, or about $190,200 per year, before any player revenue lands. The model also shows $465K of startup capex and a $615K minimum cash point in Month 4, so reserves have to stay visible before any owner draw.

These costs are mostly fixed, so more visits help spread them, but weak traffic or late booking cash can crush take-home income fast. The key inputs are the lease bill, utilities, property taxes, insurance, and the cash trough. If monthly cash starts sliding toward that $615K floor, owner pay should wait.

Protect Cash Before Owner Pay

Track the floor, not just the profit. Use a 13-week cash forecast and watch the reserve balance every week. Measure facility cost per visit by dividing $15,850 by monthly attendance, then compare that to booked traffic so you know how much each player must cover before profit can reach the owner.

Lease payment

Utility bill

Property tax bill

Liability insurance premium

If those costs rise or bookings slow, cut discretionary spend first and push deposits on group events. That keeps cash above the minimum and protects owner income when the schedule is thin.