How Much Patient Advocacy Owners Make: $120k Pay To $11M EBITDA

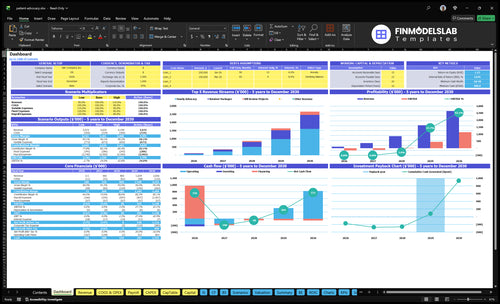

A patient advocacy business owner can plan for a $120,000 lead advocate salary in this model, but early profit does not support extra draws Researched assumptions show about $84,000 revenue in Year 1, $302,000 in Year 2, and $738,000 in Year 3, with EBITDA reaching break-even around Month 31 The higher-utilization staffed case reaches about $2385 million revenue and $1146 million EBITDA in Year 5 before taxes, reserves, debt service, or distributions Treat these as planning scenarios, not promised income

Owner income$120kNet margin-181% to 48%Revenue for target pay$250kBusiness difficultyHard

Want to test your patient advocacy owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, labor, overhead, marketing, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice, and it does not model clinical outcome assumptions.

Want the six main patient advocacy income drivers?

1

Pricing Model

$120-$190

Higher rates move take-home fast because the same case time earns more across hourly advocacy, retainers, and bill reviews.

2

Service Hours

1.5-10h

More paid hours per client lift revenue without adding as many new cases, so utilization matters.

3

Bill Review

$160-$190

Bill review brings the highest rate, but it only helps income if staff time stays tight and margin does not leak.

4

Lead Cost

$400->$250

As customer acquisition cost (CAC) falls from $400 to $250, more of each marketing dollar turns into booked patients.

5

Payroll Load

$813K

Year 5 payroll reaches $813K, so hiring pace and role mix decide how much gross profit reaches the owner.

6

Payback Lag

31 mo

The $4,770 monthly fixed bill and $480K minimum cash need push breakeven to month 31, so early draws stay limited.

If Patient Advocacy bills $120/hour and a case takes 25 hours, that is about $3,000 per case, so $120,000 of owner pay alone needs roughly 40 cases before overhead. The bigger test is capacity: Year 1 break-even revenue is about $268,000, while modeled Year 1 revenue is about $84,000. By Year 3, modeled revenue reaches about $738,000 and EBITDA turns positive at about $26,000, but intake, documentation, referral work, admin, and follow-up all count.

Revenue math

$120/hour is the billing rate.

25 hours per case equals about $3,000.

$120,000 owner pay needs about 40 cases.

Year 1 modeled revenue is about $84,000.

Real capacity

Year 1 break-even is about $268,000.

Year 3 modeled revenue is about $738,000.

EBITDA turns positive at about $26,000.

Nonbillable work also uses capacity.

How much should a patient advocate charge?

Patient Advocacy should charge $120/hour in Year 1, rising to $145/hour by Year 5, with higher pricing for complex billing work. Retainers should price at $115–$135/hour, and bill review should run $160–$190/hour; for success tracking, see What Is The Most Important Indicator Of Success For Patient Advocacy Business?. The main risk is unpaid scope creep, so calls, records review, and care-team follow-up need clear billable rules.

Core Rates

$120/hour Year 1 advocacy rate

$145/hour Year 5 advocacy rate

$115–$135/hour retainer package rate

$160–$190/hour bill review pricing

Scope Math

70–100 retainer billable hours

15–25 bill review project hours

$300 Year 1 hourly case revenue

$805 retainer; $240 bill review

Can a patient advocacy business scale?

Yes—Patient Advocacy can scale, but it is not passive income. A solo owner can protect gross margin, yet billable hours cap growth; staffed growth adds senior advocates, patient advocates, admin, marketing, and operations, so payroll rises from $144,000 in Year 1 to $282,000 in Year 2, $487,000 in Year 3, $663,000 in Year 4, and $813,000 in Year 5. Revenue can grow from about $84,000 to $2.385 million, but owner take-home improves only if utilization, pricing, quality control, and referrals outrun payroll and overhead.

Solo margin

Solo work keeps overhead lean.

Billable hours still cap output.

Pricing must rise with demand.

Referrals must stay strong.

Scale costs

Staffing adds more service roles.

Payroll rises from $144,000 to $813,000.

It passes $282,000, $487,000, and $663,000.

Revenue can reach $2.385 million.

Key Takeaways

Pricing and scope control effective hourly pay.

Billable hours rise when intake and follow-up stay tight.

Referrals beat paid ads for steadier case flow.

Cash reserves matter before owner draws expand.

Compare lean, base, and high patient advocacy owner income scenarios

Owner income scenarios

Owner income shifts with client mix, staffing, and marketing spend. Year 1 is cash negative, Month 31 is near breakeven, and Year 5 is strongly profitable.

Low, base, and high owner income cases by operating stage.

Scenario

Low CaseHard ramp

Base CaseBreakeven path

High CaseScale win

Launch model

This is the early ramp case, where owner pay is likely limited until funding covers the Year 1 loss.

This is the modeled breakeven case, where the business is close to covering payroll and overhead from operations.

This is the upside case, where scaled client volume and a larger team produce strong owner income.

Typical setup

Year 1 reaches about $84,000 revenue, with 75% hourly advocacy, $144,000 payroll, $57,240 fixed overhead, and $20,000 marketing, so EBITDA is about -$152,000.

Year 3 reaches about $738,000 revenue, with direct costs still light, $487,000 payroll, $70,000 marketing, and EBITDA near $26,000.

Year 5 reaches about $2.385 million revenue, with $813,000 payroll, $130,000 marketing, and EBITDA near $1.146 million.

Cost drivers

Year 1 loss

heavy payroll

fixed overhead

low marketing base

founder-funded draw

Growing retainers

more bill review work

higher payroll

steady marketing

thin EBITDA

Higher client volume

larger team

stronger retainer mix

more marketing

high EBITDA

Owner income rangeBefore owner reserves

-$152,000Loss year

$26,000Near breakeven

$1.146MUpside year

Best fit

Use this to stress-test cash needs when demand is still thin and owner pay is not yet dependable.

Use this as the main planning case if you expect steady client flow and gradual team expansion.

Use this to test upside if referral flow, pricing, and staffing all scale cleanly.

!

Planning note: These scenario ranges are researched planning assumptions from the model, not guaranteed earnings, salary promises, tax advice, or distribution forecasts.

Patient Advocacy Core Six Income Drivers

Pricing Model

Pricing Model Drives Pay

Pricing sets revenue per case and what the owner can pay themselves. In patient advocacy, hourly work runs $120 to $145, retainer packages run $115 to $135 per hour across 70 to 100 billable hours, and bill review projects run $160 to $190 per hour. The clean math is simple: more paid hours at the right rate means more gross margin.

The risk is loose scope. If follow-up, family calls, or records chasing is unpaid, a high-fee case can turn into low effective hourly pay fast. Use packages for complex coordination, records review, and recurring family communication so the work stays priced to the time it really takes.

Track Effective Hourly Rate

Measure billable hours, unpaid follow-up, and effective hourly rate by case type. Compare hourly advocacy, retainers, and bill review projects so you know which mix protects owner draw. If the hours are not capped in writing, margin leaks into admin time and care-team follow-up.

Price every scope change.

Log unpaid time daily.

Match packages to complex cases.

Keep the estimate tied to the case. The key inputs are price per hour, paid hours per engagement, and how much nonbillable coordination each client creates.

Staffing Leverage

Staffing Leverage

Staffing leverage means adding senior advocates in Year 2, patient advocates in Year 3, and operations support in Year 3 so one owner can serve more cases. Payroll rises from $144,000 in Year 1 to $813,000 in Year 5, while revenue is modeled to reach $2,385 million by Year 5. That only lifts owner pay if billable volume, pricing, and case mix cover training, quality control, and compliance.

More staff can raise capacity, but it also cuts flexibility and adds management load. If added advocates do not turn nonbillable work into paid hours, the owner ends up funding payroll growth instead of taking home more profit. Here’s the quick math: payroll grows about 5.6x from Year 1 to Year 5, so the business needs steady case flow and tight scope control to keep draws safe.

Track capacity before you hire

Measure billable hours per advocate, revenue per case, and payroll as a share of revenue before each hire. Tie senior advocates to complex cases, patient advocates to higher case volume, and operations support to less admin drag. If a role does not lift billed capacity, it can lower owner income even when revenue looks bigger on paper.

Use staffing only when the pipeline can fill the added hours. Track intake, scheduling, documentation, follow-up, and compliance work, then forecast how many paid hours each hire must create to cover salary plus oversight. If scope is loose or handoffs are messy, unpaid work rises fast and effective margin falls.

Billable Utilization

Billable Utilization

Owner income rises when more of the week turns into paid advocacy time. In this model, billable hours per engagement run from 25 to 35 for hourly advocacy, 70 to 100 for retainers, and 15 to 25 for bill review, so the same advocate can produce more revenue if scope stays tight and service quality holds.

Here’s the catch: intake, documentation, care-team follow-up, admin, referral development, and client education all eat working time. If those tasks expand, effective hourly pay falls, gross margin tightens, and less cash is left for owner draw. The quick test is billable hours divided by total working hours, by case type.

Raise Paid Advocacy Hours

Track billable hours, nonbillable hours, and revenue per advocate by service line. Then compare hourly advocacy, retainer work, and bill review separately, because the mix changes utilization and pay. A retainer with 70 to 100 billable hours can outperform a smaller hourly case only if follow-up does not spill into unpaid time.

Set clear scope, pre-book follow-ups, and use templates for notes and care-team updates. Measure the share of time spent on intake, documentation, and admin each week. If unpaid work keeps climbing, raise minimum case size, narrow service menus, or price for the extra labor so owner income does not get diluted.

Count billable hours by case

Track unpaid follow-up weekly

Separate results by service type

Price scope creep before it spreads

Overhead And Reserves

Overhead and Reserve Discipline

$4,770 a month in fixed overhead covers rent, utilities, privacy-compliant CRM and billing software, supplies, legal and accounting, IT, telecom, and training. That base cost is small, but it still sets the floor for owner pay. When revenue-linked costs fall from 175% in Year 1 to 100% in Year 5, more profit can stay in the business instead of being eaten by operating drag.

The cash rule matters too: the minimum cash need is $480,000 at Month 31. That means the owner should not pull every dollar of EBITDA, or earnings before interest, taxes, depreciation, and amortization. Safer draws start after break-even and after reserves are funded, so the business can handle slow collections, unpaid follow-up, and case spikes without starving payroll or operations.

Hold the Line on Cash

Track fixed overhead, revenue-linked cost %, and cash on hand every month. If overhead rises above $4,770 without more billable hours, owner pay gets squeezed fast. If costs stay high in Year 1, keep draw policy tight and use cash to build the reserve instead of paying out profit too early.

Watch monthly overhead per active client.

Check reserve runway against Month 31.

Set draws after break-even only.

Here’s the quick math: lower overhead and lower variable costs raise the share of revenue that can become free cash. But what this estimate hides is timing risk, since patient work can bill late and collect late. That’s why the reserve is not optional; it protects owner pay when collections slip or case volume dips.

Case Complexity And Specialization

Complex Case Pricing

Complex cases can lift revenue fast because the client pays for judgment, not just time. In this model, hourly advocacy often runs $120 to $145, while bill review projects can reach $160 to $190 per hour. The upside only holds if scope stays tight, because unpaid follow-up, extra handoffs, and deep documentation can drag effective hourly pay down.

Track case type, billable hours, and handoffs per client. A care coordination case with many family updates may look premium, but if it turns into heavy admin, owner take-home falls. Keep the work clearly outside medical, legal, tax, or insurance advice unless properly qualified, so the business protects both pricing and risk.

Price by Scope, Not Emotion

Use case details to set price before work starts. Here’s the quick math: revenue per case = billable hours × hourly rate. Higher-value work includes eldercare navigation, insurance appeal support, condition-specific navigation, and records review. Those cases can justify higher fees only when you define what is included, what is excluded, and how many touchpoints the client gets.

Track billable hours by case type.

Count nonbillable handoffs and calls.

Price extra documentation separately.

Set boundaries on advice and follow-up.

If a case needs more coordination than planned, reset scope early. That protects gross margin and keeps more of the collected fee available for owner pay instead of getting eaten by unpaid work.

Client Acquisition

Referral-Led Client Acquisition

When referrals stay steady, the owner spends less time chasing low-fit leads and more time on billable advocacy. Here’s the quick math: annual marketing rises from $20,000 in Year 1 to $130,000 in Year 5, while customer acquisition cost (CAC) improves from $400 to $250. That shift supports more predictable case volume and protects utilization, which lifts take-home income.

This driver includes referral volume, lead quality, consultation close rate, and CAC by source. Useful sources are eldercare professionals, attorneys, caregiver groups, and healthcare-adjacent networks. What this estimate hides: referral channels must avoid improper referral payments and other compliance-sensitive arrangements, or the margin gain can turn into legal and cash flow risk.

Measure CAC by source

Track each source separately: referrals, paid search, events, and partner outreach. If 100 new clients cost $40,000 at a $400 CAC, and then $25,000 at a $250 CAC, that is $15,000 saved on the same volume. Lower CAC gives the owner more room to pay themselves after fixed overhead and staff time.

Focus on referral quality, not just count. Ask which sources bring complex, high-fit cases that convert fast and stay longer. Keep outreach documented, use plain referral rules, and have counsel review any partner setup so growth stays clean and the extra revenue does not get eaten by compliance or wasted marketing spend.