How Much Do Patient Transport Service Owners Make at 15% Take-Rate

You’re trying to separate ride revenue from cash you can actually pay yourself In the supplied five-year model, first-year revenue is ~$144M with an 850% margin after listed direct and variable costs, but owner income is before personal taxes and only after payroll, vehicle debt, and reserves are funded Because payroll, fleet count, debt service, and reserve percentage are not provided, treat owner pay as a planning output, not a guaranteed distribution

Owner income$7.9MNet margin7%Revenue for target pay$14.3kBusiness difficultyHard

Want to see the six main income drivers?

1

Trip Volume

7.6K

More completed rides spread fixed costs, so take-home rises fast when utilization climbs.

2

Payer Mix

$60-$75

Higher-paying facility and insurance work lifts revenue per ride and steadies monthly income.

3

Fleet Mix

20%-55%

A bigger share of small fleets and larger operators increases capacity, but the right vehicle mix keeps margin from leaking.

4

Staffing Load

$52K/mo

Payroll moves fast as the team grows, and owner pay holds up only if trips rise faster than staff.

5

Overhead

$66K/mo

Known fixed costs run about $66K a month before payroll and fleet debt, so reserves decide how long cash lasts.

6

Dispatch Control

30 mo

Cleaner dispatch and fewer no-shows keep vehicles busy, which protects margin and shortens payback.

Want to test your owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see owner income in the Patient Transport Service model?

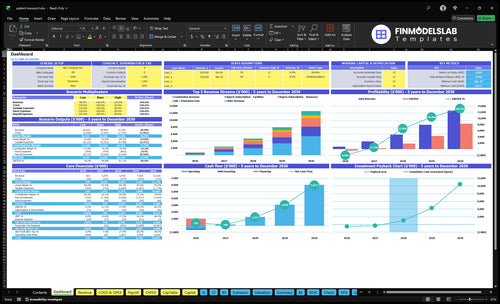

The Patient Transport Service Financial Model Template dashboard shows the revenue build, payer mix, seller mix, acquisition assumptions, commission and subscription revenue, COGS, variable expenses, fixed overhead, scenario testing, and owner income outputs. It also shows ~$144M first-year revenue, 850% margin after listed direct and variable costs, $350k marketing, and a ~$7,948k pre-payroll ceiling; open the model for the full view.

Owner-income model highlights

Owner take-home outputs

Revenue and margin build

Separate input ceilings

Does adding more vehicles increase patient transport owner income?

Yes, but only if utilization keeps up. For a Patient Transport Service, more vehicles can lift income when staffing, routing, and payer demand scale with the fleet: the model shifts supply from 600% individual drivers in Year 1 to 200% by Year 5, while small fleets rise from 300% to 550%. Demand also shifts toward facilities and insurance from 300% combined to 700%, but idle vehicles, insurance, repairs, and payroll can outrun completed trips.

When more vehicles help

Repeat orders rise.

CAC falls with scale.

Dispatch stays tight.

Trips per vehicle hold up.

When more vehicles hurt

Idle vehicles drain cash.

Insurance costs climb.

Repairs add up fast.

Payroll outruns trips.

What costs reduce patient transport business profit?

For a Patient Transport Service, profit gets squeezed fast by platform costs and by transport costs that sit outside the app math; if you’re planning launch spend, What Is The Estimated Cost To Open And Launch Your Patient Transport Service Business? gives the setup side. In Year 1, 100% of direct costs are already spoken for: 60% cloud hosting and software licensing, plus 40% provider vetting and onboarding. Variable costs add another 50%—30% payment processing and 20% customer support tools—before you count $66k/month fixed overhead and $350k first-year marketing, plus vehicle insurance, driver wages, fuel, repairs, dispatch labor, no-shows, and vehicle debt.

Direct cost load

60% cloud hosting

40% provider vetting

100% Year 1 direct costs

Owner take-home looks too high

Operating costs

30% payment processing

20% support tools

$66k/month fixed overhead

$350k first-year marketing

How much can a patient transport owner make with one van?

A Patient Transport Service owner with one van can’t calculate reliable take-home from the source data because driver wages, fuel, maintenance, debt service, and operating days are missing. Use rides per day × days operated × average reimbursement; Year 1 payer values are $60 for individual patients, $75 for facilities, and $70 for insurance, then track the core metric in What Is The Most Important Indicator Of Success For Your Patient Transport Service?.

Revenue math

Use rides/day × days × reimbursement

Individual patient rate: $60

Facility rate: $75

Insurance rate: $70

Owner pay levers

Drive yourself to cut payroll

Expect a capacity ceiling

Hire drivers to grow trips

Reserve cash for scheduling risk

Key Takeaways

More paid trips per route hour raise revenue.

Payer mix drives average trip revenue and repeats.

Add vehicles only after utilization supports them.

Dispatch quality protects margin and repeat accounts.

Compare low, base, and high owner income scenarios

Owner income scenarios

Owner income swings hard here because fixed staffing and compliance costs stay high while demand and payer mix change over time. The three cases show how slow ramp, mid-scale, and mature scale affect profit left for the owner.

Downside, base, and upside income paths for planning.

Scenario

Low CaseDownside case

Base CaseModeled case

High CaseUpside case

Launch model

This is the slow-start case, where Year 1 demand stays thin and fixed costs still dominate owner income.

This is the modeled middle path, where the business reaches steady Year 3 scale and owner income turns positive.

This is the stronger upside case, where the business reaches mature Year 5 scale and owner income is much higher.

Typical setup

It assumes a first-year ramp with lower utilization, a buyer mix still led by individual patients, and payroll, support, and compliance costs that outgrow revenue.

It assumes Year 3 revenue near $902M, about 87.8% margin after listed direct and variable costs, and a more balanced mix of patients, facilities, and insurance.

It assumes Year 5 revenue near $2,992M, about 90.6% margin after listed direct and variable costs, and a larger facility and insurance mix with more repeat volume.

Cost drivers

first-year ramp

low utilization

heavy payroll

compliance and vetting

missing vehicle debt

mid-model scale

mixed payer mix

repeat orders

sales coverage

software and support costs

mature volume

higher repeat orders

larger payer mix

staffing scale-up

utilization pressure

Owner income rangeBefore owner reserves

-$472kLoss risk

$1.8MCore plan

$8.3MUpside case

Best fit

Use this to stress-test launch risk, staffing strain, and how long cash stays tight before volume catches up.

Use this as the main planning case for budgeting, staffing, and cash control.

Use this to test what happens if volume scales well but staffing and utilization stay under control.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions; they also leave out vehicle debt and reserve funding.

Patient Transport Service Core Six Income Drivers

Trip Volume And Vehicle Utilization

More Paid Rides per Route Hour

Trip volume and vehicle utilization is the main income lever here: the same vehicle and driver schedule can produce more cash only when more trips are completed and billed. The first-year model assumes 7,600 orders, or about 633 per month, so every missed pickup, long wait, cancellation, or idle gap cuts revenue without lowering fixed costs.

Recurring accounts make this matter more. The model assumes repeat orders of 15 for individual patients, 80 for facilities, and 150 for insurance. The clean operating goal is simple: more paid rides per route hour.

Measure Fill Rate, Not Just Bookings

Track booked trips, completed billable trips, on-time pickups, and driver idle time by route hour. A schedule that looks full but drops trips at the last minute still hurts income, because the vehicle and driver are already committed.

7,600 annual orders target

633 monthly orders target

15, 80, 150 repeat counts

Watch cancellations and no-shows

Reduce gaps between pickups

Use tighter dispatch rules for repeat facility and insurance routes, since those accounts repeat often and can lift utilization fast. If onboarding or scheduling takes too long, route hours turn into wasted payroll, and take-home income drops even when demand is there.

Dispatch, Routing, And No-Show Control

Dispatch And No-Show Control

Dispatch quality drives owner income because it changes billable rides, driver hours, fuel, deadhead miles, and repeat bookings. The model does not give a no-show rate, so treat it as an editable input. When routing is tight, more paid trips fit into each route hour, and that helps protect the modeled 850% Year 1 margin after listed direct and variable costs.

Poor scheduling does the opposite. It turns paid driver time into idle time, raises fuel use, and weakens retention with facility and insurance accounts that rely on reliable pickups. One missed trip can hit revenue twice: lost ride income now and lower repeat volume later. That matters most when recurring accounts repeat 80 to 150 times in Year 1.

Track Pickups, Gaps, And Misses

Track completed rides per route hour, no-shows, late arrivals, cancellation rate, and deadhead miles. Here’s the quick math: more completed trips with the same driver schedule means more revenue without the same rise in labor and fuel. If pickups slip, fix dispatch rules before adding vehicles or staff.

Build the forecast around no-show rate, route time, and account mix. Test tighter scheduling windows for facility jobs, because reliable pickups make recurring accounts more valuable. If one route has high idle time, re-batch nearby trips and shorten wait gaps so paid driver time stays billable instead of becoming overhead.

Payer Mix And Reimbursement Rates

Payer Mix

Payer mix changes revenue per trip fast. The first-year average order value is $60 for individual patients, $75 for facilities, and $70 for insurance. A heavier share of facility and insurance trips lifts cash per ride, but local contracts, payer terms, and billing rules can change the real reimbursement. One clean rule: better payer mix beats more low-rate rides.

Recurring accounts matter because facilities repeat 80 times and insurance repeats 150 times in Year 1, while individual patients repeat 15 times. Here’s the quick math: more repeat trips mean more predictable collections and less chase for new bookings. If the mix tilts toward repeat payers, owner take-home improves even if total trip count stays flat.

Track By Payer

Measure trip count, average reimbursement per payer, and repeat volume by segment every month. Don’t use one blended rate in the forecast; separate individual, facility, and insurance income so you can see which payer funds payroll and profit. The $60, $75, and $70 figures are useful starting points, not universal rates.

Before you sign or renew accounts, test what each payer actually pays after local rules, mileage limits, and authorization steps. If a segment takes more admin work but pays near the lower end, it can drag down margin and cash flow. Keep a simple payer sheet with trips, repeat count, and collected revenue so you can protect owner draw.

Operating Costs And Cash Reserves

Reserve-Adjusted Income

Reserve-adjusted income is the safer payout number. Year 1 carries 100% of revenue in listed direct costs, another 50% in variable costs, plus $66k per month in fixed overhead and $350k of marketing in Year 1. That leaves little room for owner draws until cash covers bad weeks, slow payers, and unplanned downtime.

Count commercial auto insurance, fuel, maintenance, vehicle payments, licenses, dispatch labor, and repair reserves before taking distributions. If a vehicle breaks or a claim pays late, booked income won’t hit the bank on time. One clean rule: no owner pay until the reserve bucket is funded.

Build the Cash Buffer

Track cash on hand, days of cash, and monthly burn. The quick math starts with $66k in monthly fixed overhead, then adds operating reserves for repairs and insurance renewals. That means cash planning should follow real bills, not just trip volume or booked revenue.

Measure these inputs every month:

Completed trips

Fuel per trip

Repair spend

Insurance renewal timing

Dispatch labor

Customer payment lag

When any of these drift up, owner pay should drop first. That keeps distributions tied to cash, not to a paper margin that can disappear after one breakdown or a slow insurer payment.

Staffing And Owner Role

Owner Driving And Staffing

When the owner drives early trips, take-home cash can look stronger because paid driver cost is delayed. But that only works if you treat owner hours as a real cost; otherwise profit is overstated and the model gets too rosy.

In non-emergency medical transportation, staffing also adds payroll, supervision, scheduling, and compliance work. Source data puts provider vetting and onboarding at 40% of revenue in Year 1, falling to 20% by Year 5, so labor setup is a major drag before scale kicks in.

Track Owner Labor Separately

Price owner driving as labor, not free work. Track owner hours, paid driver hours, trips per route hour, and onboarding cost as a % of revenue. That shows whether more routes are creating real profit or just trading owner sweat for revenue.

Separate owner pay from business profit.

Test hiring only when routes expand.

Watch onboarding at 40% then 20%.

Flag burnout before service quality drops.

If the owner keeps driving, cash flow may improve fast, but the business still needs a plan for coverage, compliance, and scheduling. Once driver volume grows, the real check is whether payroll and supervision stay lower than the extra trips they unlock.

Fleet Size And Vehicle Type

Fleet Size and Vehicle Mix

Fleet size should follow utilization, not a revenue target. If a new vehicle is added before trips, it can raise insurance, repair reserves, and idle cost faster than it adds cash. The key inputs are vehicle count, paid trips per route hour, and revenue by service level, so each unit should be checked as its own profit center.

Ambulatory, wheelchair-accessible, and higher-acuity service levels change price, capacity, staffing, and risk. The source data does not give vehicle count, van cost, financing, or maintenance by type, so the owner should not assume every added unit improves take-home pay. A bigger fleet only helps if each vehicle clears its own costs and still leaves margin for the owner.

Measure Before You Add Vehicles

Track paid rides per vehicle day, idle hours, cancellations, and revenue by vehicle class. Here’s the quick math: if a unit is not busy enough to cover its own direct costs plus its share of overhead, the extra revenue is weak and owner draw can shrink.

Set a separate margin target for each vehicle type and test it against staffing, insurance, fuel, and repair reserves. A wheelchair van should not be priced or approved like an ambulatory vehicle if it needs more labor or has slower loading. That keeps growth tied to cash, not just trip count.