Peatland Restoration Owner Income: $185K Salary Plus Scenario Upside

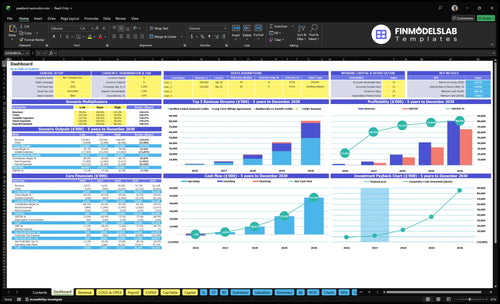

A peatland restoration service owner can plan around a $185,000 annual CEO salary in this model, before personal taxes Here’s the quick math: first-year revenue is $2075M, listed direct and variable costs are 195%, gross margin is 805%, and EBITDA before reserves and reinvestment is about $568k By Year 5, modeled revenue reaches $811M with 845% gross margin and $662M EBITDA, but that upside depends on verified credit volume, offtake agreements, compliance costs, and cash reserves Carbon credits, grants, and distributions are scenario inputs, not guaranteed take-home pay

Owner income$185kNet margin22% to 81%Revenue for target pay$855kBusiness difficultyHard

What owner pay fits your restoration pipeline?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate only, not guaranteed salary, tax advice, or owner distribution advice.

Which six drivers move owner take-home most?

1

Project Volume

$2.1M-$81.1M

More funded peatland sites drive more credits, and revenue scales from $2.1M in year 1 to $81.1M in year 5.

2

Contract Mix

$69-$108

The mix of verified credits, offtake deals, and biodiversity add-ons lifts realized price per unit.

3

Carbon Timing

2-17 mo

Breakeven lands in month 2, but payback takes 17 months, so slow issuance or sales timing ties up cash.

4

Delivery Costs

16%-20%

Registry fees, audits, royalties, and commissions run about 16%-20% of sales, so small cuts flow straight to take-home.

5

Compliance Load

$28K/mo

Remote sensing, legal, and reporting costs sit in fixed overhead, so lean compliance keeps more cash in the business.

6

Payroll Discipline

$770K-$2.0M

Payroll rises from about $770K to $2.0M as the team scales, so hiring discipline protects owner income.

Can a peatland restoration founder pay themselves?

Yes, a Peatland Restoration Service founder can pay themselves if pay is built into eligible payroll, management fees, unrestricted service revenue, or allowed profit distributions. This model includes a $185,000 CEO salary in year 1; see What Are Operating Costs For Peatland Restoration Service? for where that sits in operating costs. Restricted grants or monitoring funds should not be treated as owner cash.

Pay paths

Budget payroll before launch.

Use approved management fees.

Pay from unrestricted service revenue.

Distribute profit after reserves.

Guardrails

$185,000 CEO salary is modeled.

1 credit represents 1 ton CO2e.

Keep monitoring funds restricted.

Confirm treatment with CPA and counsel.

How much revenue does a peatland restoration service need to pay the owner?

The Peatland Restoration Service needs about $1.37M in annual revenue to cover $770k of payroll, including the $185k CEO salary, plus fixed overhead before reserves. At the modeled $2.075M first year and 80.5% gross margin, EBITDA is about $568k, but owner pay still depends on cash left after compliance, capex, and working capital.

Break-even math

$1.37M break-even revenue

$770k payroll load

$185k CEO salary included

80.5% gross margin drives EBITDA

Owner payout rule

Revenue is not take-home cash

EBITDA is about $568k

Reserve cash for compliance

Fund capex and working capital first

What affects peatland restoration profit margin?

If you’re asking what affects Peatland Restoration Service profit margin, the short answer is pricing discipline: owner income is hit hardest by direct delivery costs, verification, royalty terms, broker commissions, technical payroll, and monitoring burden. Here’s the quick math: first-year direct and variable costs total 195%, then ease to 155% by Year 5, while third-party verification audits alone run 50% in Year 1 and 30% by Year 5; see What Are The 5 KPIs For Peatland Restoration Service Business? for the metrics that keep this from slipping.

Big margin drains

Direct delivery costs set the floor.

Verification audits take 50% Year 1.

Royalty and broker terms cut take-home.

Technical payroll and monitoring add drag.

What to price in

Field work and hydrology design.

Equipment and rework.

Travel and permitting.

Monitoring burden from year one.

Key Takeaways

Funded projects, not pipeline size, pay owner salaries.

Unverified carbon credits cannot safely fund payroll.

Reserves protect pay through delays, overhead, and seasonality.

Compare low, base, and high owner-income scenarios using the provided model years

Owner income scenario table

Owner income stays close to salary at launch and scales with volume, payroll, and margin. The upside case only works when all modeled credits sell and distributions are actually paid.

Low, base, and high cases show how owner income changes as peatland restoration scales.

Scenario

Low CaseLaunch downside

Base CaseModeled base

High CaseUpside case

Launch model

This case keeps owner income close to the CEO salary during the first operating year.

This case assumes owner income stays anchored to salary while the business reaches modeled scale in Year 3.

This case adds upside only if the mature model delivers strong sales and available distributions.

Typical setup

Year 1 runs at $2.075M revenue, 15,000 verified credits, $770k payroll, and early-stage overhead, so owner pay is mostly salary.

Year 3 reaches $19.35M revenue, 110,000 verified credits, $1.3M payroll, and $14.038M EBITDA, so salary remains the main owner draw.

Year 5 reaches $81.1M revenue, 750,000 modeled units sold, $2.01M payroll, and $65.584M EBITDA, so owner income can rise beyond salary.

Cost drivers

$2.075M revenue

15,000 credits

$770k payroll

launch overhead

CEO salary only

$19.35M revenue

110,000 credits

$1.3M payroll

$14.038M EBITDA

CEO salary only

$81.1M revenue

750,000 units sold

$2.01M payroll

$65.584M EBITDA

salary plus distributions

Owner income rangeBefore owner reserves

$185k salary onlySalary only

$185k salary onlyCore salary

$185k salary + distributionsUpside pay

Best fit

Use this to stress-test launch cash flow when volume is still small and distributions are not expected.

Use this as the working case for budgeting, hiring, and lender or investor planning.

Use this to test the strongest credible outcome, but it is not typical or guaranteed.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Peatland Restoration Service Core Six Income Drivers

Funded Restoration Project Volume

Funded Project Volume

Funded, executable project volume is the first gate on owner income. The model scales from 30,000 first-year units to 750,000 by Year 5, a 25x jump, but only if the work is backed by signed offtakes, verified credits, and funded restoration contracts. Without those, demand is just pipeline, and the $185k salary becomes cash-flow risk.

What this hides is timing. If projects are not funded before field work starts, payroll, verification, and land work still hit cash first. So the owner can show growth on paper and still miss pay days if volume is not executable.

Track Signed Volume Early

Measure volume by signed units, not leads. Track acres under contract, credits verified, and dollars funded against the work plan so you can see what is truly cash-backed. A clean pipeline should answer one question fast: can this project pay field crews, audits, and owner pay on time?

Signed offtakes by unit.

Verified credits by month.

Funded contracts before mobilization.

Cash cover for the $185k salary.

If the pipeline slips, slow hiring and delay distributions. That protects cash while you convert modeled volume into revenue the bank can actually see.

Direct Delivery Cost Control

Direct Cost Control

Direct cost control decides how much of each project dollar reaches owner pay. In the model, listed direct and variable costs are 195% of first-year revenue and 155% by Year 5, so gross margin is still negative before overhead. That means every $1.00 of revenue can be paired with $1.95 or $1.55 of direct cost unless pricing, scope, or pass-through terms change.

Those costs include registry issuance, account fees, third-party audits, landowner royalties, and broker commissions. Real field work can also add excavation, ditch blocking, native vegetation, travel, and subcontractors. Don’t cut technical quality to force margin; if verification slips, the saved cost can turn into lost revenue and weaker cash flow for the owner.

Track Cost Per Verified Credit

Measure direct cost per acre and per verified credit, then compare it to the revenue from that same unit. Separate pass-through spend from the management fee so owner income is tied to true gross margin, not reimbursed costs. The quick rule is simple: if direct costs stay above 100% of revenue, there is no room for owner draw.

Bid audits and royalties separately.

Forecast travel and subcontractors.

Approve scope before field work.

Price for scope creep upfront.

Use cost-plus pricing when field scope is uncertain, and keep inspection and verification steps intact. A project that misses verification may save a little cash now but can wipe out the credit sale later, which hurts both gross margin and the owner's take-home pay.

Monitoring, Permitting, And Compliance Burden

Monitoring, Permitting, and Compliance Burden

This is the cash leak between field work and owner pay. Third-party verification audits cost 50% in Year 1 and 30% by Year 5, registry fees add 45% in Year 1 and 25% by Year 5, and legal and regulatory compliance runs $5,000 per month. These costs can keep hitting cash after credits are sold.

Inputs here are project volume, audit timing, registry fees, permit scope, and how long monitoring lasts. The early monitoring and field equipment capex is $905k, so reserve planning matters. If compliance spend grows faster than verified sales, free cash drops and the owner’s draw has to wait.

Track cash burn before paying out

Build a monthly compliance budget and tie it to verified output, not booked promises. Here’s the quick math: if audits, registry charges, and legal costs rise before credits clear, the business funds the gap. That means owner pay should come from cash after reserves, not from unverified inventory.

Watch three numbers every month: audit cost rate, registry fee rate, and legal spend. If the project needs more field checks or a longer permit cycle, keep distributions tight. The clean rule is simple: protect the $905k early capex reserve first, then pay the owner.

Audit cadence changes cash timing.

Permit delay pushes pay later.

Reserves protect take-home income.

Fee And Contract Structure

Fee and contract structure

Contract terms decide how much project funding can actually support owner pay. In the model, first-year gross margin is 805% after registry fees, verification audits, landowner royalties, and broker commissions, but that only holds if the contract fits the work. Fixed-fee jobs can lose cash when field scope expands, while cost-plus work can protect margin if eligible overhead is clearly defined.

To estimate this driver, track project volume, fee type, reimbursable costs, landowner payments, broker fees, and approved payroll. Keep restricted pass-through costs out of owner-pay math. Management fees and approved payroll are the cleaner paths for owner compensation when contract language supports them.

Protect margin with contract terms

Price each job against the real cost stack before you sign. Here’s the quick math: if field scope, audit work, or verification steps grow after the bid, a fixed fee eats cash fast. If overhead is eligible under the contract, use cost-plus so the business can recover it instead of funding it from owner draw.

Track these items on every project:

Fixed fee versus cost-plus

Eligible overhead definition

Pass-through cost rules

Change-order approval timing

Management fee and payroll recovery

Carbon Revenue Timing

Carbon Revenue Timing

Carbon revenue can be huge on paper and slow in cash. In the model, verified carbon removal credits drive $1,275M of first-year revenue and $494M by Year 5, while long-term offtake revenue rises from $700k to $275M and biodiversity co-benefit revenue from $100k to $42M. If credits are still unverified, they should not fund owner pay.

The timing risk is the gap between work done and cash collected. Verification, permanence checks, monitoring, and buyer timing can all delay distributable cash, so accounting revenue and owner draw can split fast. One clean rule: if the credit is not verified and sold, it is not owner income yet.

Track Cash, Not Just Credits

Measure the lag from field work to cash in bank. Track verified credits, signed offtake volume, buyer payment terms, and the months from restoration work to issuance. The key inputs are units restored, verification status, sale price per credit, and how much revenue is already contracted. Without those, the forecast can overstate what can be paid out.

Separate verified from pending credits.

Forecast cash by issuance month.

Delay owner pay on uncollected revenue.

Stress-test buyer and audit delays.

If revenue depends on delayed verification, keep reserves and use management fees or approved payroll for owner pay. That protects cash when monitoring, registry steps, or buyer timing slips.

Overhead, Reimbursement Timing, And Reserves

Overhead, reimbursement timing, and reserves

Accounting profit is not the same as owner cash. With $277k a month of fixed overhead and $770k in first-year payroll, modeled core burn is about $919k per month before variable costs. If reimbursement lands late, payroll, insurance, and field spend still come due, so the owner’s draw depends on cash timing, not booked revenue.

This driver includes overhead, payroll cadence, insurance, reimbursement lag, and reserve balance. It hits hardest during seasonality, verification delays, and ramp-up, when weak reserves can force a cut to the $185k owner salary or reduce distributions just to keep the business funded.

Protect cash before distributions

Track cash on hand, days to reimbursement, and the next 90 days of payroll and insurance due dates. Hold distributions until reserves cover the expected lag plus the modeled burn, so the business can keep paying staff even when project cash arrives late.

Build a 13-week cash forecast

Set a minimum reserve floor

Age unpaid reimbursements weekly

Pay owner only after reserve tests

What this estimate hides is how fast cash can tighten if verification or billing slips by even one cycle. Reserve discipline keeps payroll stable and protects owner pay during project ramp-up, when paper profit can look healthy but cash is already spoken for.