How Much Can a Personality Assessment Software Owner Make at $73M Revenue

A personality assessment software owner can plan around a modeled CEO salary of $140k, but true owner take-home depends on profit and cash reserves In the researched assumptions, revenue reaches $855k in Year 1, $3096M in Year 3, and $7324M in Year 5 EBITDA starts at -$83k in Year 1 and rises to $4019M by Year 5, but that is not the same as distributable cash Treat these as planning assumptions, not guaranteed earnings

Owner income$140kNet margin-10% to 55%Revenue for target pay$1.8MBusiness difficultyMedium

Want to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want the six owner-income drivers?

1

Pricing Power

$199-$2K

Higher monthly prices and one-time fees lift revenue per account, and the mix shifts toward Growth and Enterprise plans over time.

2

Active Base

15%-22%

Trial starts rise from 5% to 10% and trial-to-paid conversion climbs from 15% to 22%, so more users turn into recurring revenue.

3

Payroll Load

$450K-$1.3M

Payroll grows from $450K to $1.325M, and that fixed cost can wipe out early profit even when sales keep rising.

4

CAC Efficiency

$350-$450

CAC falls from $450 to $350, so each marketing dollar buys more paid customers as spend scales from $120K to $450K.

5

Gross Margin

90%-94%

Delivery costs stay near 6% to 10% of revenue, so more of each sale drops through to EBITDA.

6

Credibility

2%-4%

Validation and compliance support enterprise trust, and that helps move more customers into higher-value plans.

Want to see owner income in the full model?

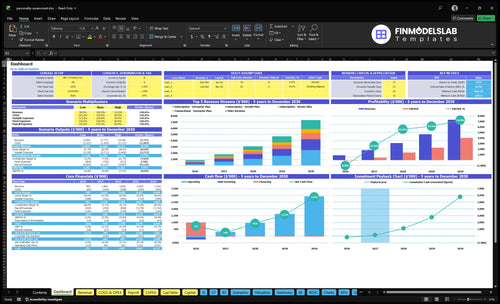

This dashboard in the Personality Assessment Software Financial Model Template shows revenue, EBITDA, cash need, break-even, and owner pay. Assumptions cover pricing, plan mix, trial conversion, CAC, churn, staffing, gross margin, fixed costs, capex, reserves, and owner salary.

Owner-income model highlights

Min cash: $671k

Break-even: Month 8

Payback: Month 23

Revenue: $855k to $7,324M

EBITDA: -$83k to $4,019M

How does personality assessment software make money?

Personality Assessment Software makes money from monthly subscriptions, per-assessment fees, enterprise licenses, and one-time setup fees. In Year 1, pricing is $199 Starter, $499 Growth, and $1,500 Enterprise per month, with per-assessment fees of $25, $20, and $15. The enterprise mix rising from 10% to 25% by Year 5 should lift revenue quality and owner pay capacity, and any white-label access or services should be modeled separately.

Core revenue

Subscriptions create recurring MRR.

Usage fees scale with assessments.

Enterprise licenses raise contract value.

Setup fees bring upfront cash.

Year 1 pricing

$199 Starter, $25 per assessment.

$499 Growth, $20 per assessment.

$1,500 Enterprise, $15 per assessment.

$0, $500, $2,500 setup fees.

What costs reduce personality assessment software owner income?

Separate delivery costs from operating expenses if you want to know what cuts owner income in Personality Assessment Software. Cloud hosting takes 6% to 4% of revenue and assessment validation audits take 4% to 2%, while sales commissions add 5% and payment fees run 3% to 25%. For the launch math, see How Do I Launch Personality Assessment Software?; the cash plan still needs reserves because minimum cash reaches $671k in Month 8.

Variable costs

Cloud hosting: 6% to 4%

Validation audits: 4% to 2%

Sales commissions: 5%

Payment fees: 3% to 25%

Fixed and build costs

Annual overhead: $144k

Payroll: $450k to $1.325M

Marketing: $120k to $450k

Capex: $80k and $12k

Is personality assessment software more profitable as self-serve or enterprise SaaS?

For Personality Assessment Software, enterprise SaaS is usually the more profitable path by Year 5 if CAC drops from $450 to $350 and the enterprise mix rises from 10% to 25%. The self-serve model can still scale volume at $199/month with a 60% Starter mix, but it only works if trial traffic, conversion, support load, and churn stay tight. Enterprise wins on higher pricing too: $2,000/month plus $3,500 one-time fees.

Self-Serve Model

$199 monthly Starter price

60% Starter mix at launch

Needs trial traffic and conversion

Low support keeps margin cleaner

Enterprise Model

$2,000 monthly by Year 5

$3,500 one-time setup fee

10% to 25% enterprise mix

Needs sales, security, renewals

Key Takeaways

Higher prices lift owner pay if retention holds.

Better retention protects ARR and reduces sales pressure.

Low delivery costs keep margins near 94%.

CAC, payroll, and compliance decide cash timing.

Scenario objective: Compare low, base, and high owner-income outcomes using researched assumptions

Owner income scenarios

Owner income shifts with trial conversion, plan mix, and Enterprise pricing. Year 1 is cash-tight, Year 3 turns profitable, and Year 5 leaves more room for owner pay.

Low, base, and high cases show how revenue mix and spend change owner pay.

Scenario

Low CaseCash need

Base CasePayback

High CaseStaffing load

Launch model

This is the lower earnings path, where owner pay is mostly salary and cash stays tight.

This is the modeled middle path, where profit starts to support owner pay.

This is the stronger earnings path, where scale supports bigger owner pay but also heavier reinvestment.

Typical setup

Year 1 mirrors $855k revenue, about 90% gross margin, -$83k EBITDA, $120k marketing, $450 CAC, 60% Starter mix, and a $140k CEO salary funded by cash.

Year 3 mirrors $3.096M revenue, about 92% gross margin, $1.355M EBITDA, $250k marketing, $400 CAC, and a 15% Enterprise mix.

Year 5 mirrors $7.324M revenue, about 94% gross margin, $4.019M EBITDA, $450k marketing, $350 CAC, and a 25% Enterprise mix.

Cost drivers

5% trial starts

15% conversion

60% Starter mix

$120k marketing

$450 CAC

18% conversion

15% Enterprise mix

$250k marketing

$400 CAC

92% gross margin

22% conversion

25% Enterprise mix

$450k marketing

$350 CAC

heavier staffing

Owner income rangeBefore owner reserves

$140k salary-fundedSalary funded

Profit-backed owner payMonth 8

Scaled owner take-homeReinvestment pressure

Best fit

Founders stress-testing the launch year and cash runway.

Operators planning around the first profitable scale-up period.

Teams modeling rapid growth, bigger headcount, and reinvestment.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or expected distributions.

Personality Assessment Software Core Six Income Drivers

Pricing and Monetization

Pricing mix drives pay

When pricing moves, owner pay moves too, because every recurring account re-rates the revenue base. Here the Year 1 weighted monthly revenue per customer is about $509 before one-time fees, and the plan ladder rises from $199, $499, and $1,500 to $250, $600, and $2,000 by Year 5. If retention holds, higher ACV can fund more sales payroll and compliance spend.

What this hides is service load. Enterprise sales usually need more demos, onboarding, procurement work, and support, so the extra revenue does not all flow to profit. A cleaner mix helps take-home income only if the added gross profit beats the extra delivery and admin time. One-liner: price up, but watch the service cost on every larger account.

Track mix, not just price

Measure plan mix, enterprise share, one-time fees, and support hours per account. The key check is simple: do higher-priced accounts lift monthly recurring revenue faster than they raise demo, onboarding, and procurement costs? If not, the owner may see more revenue but less cash for draws.

Use a monthly cohort view. Compare new logos at $199/$499/$1,500 against the updated $250/$600/$2,000 ladder, then tie each tier to staffing and compliance cost. If enterprise retention stays strong, the higher ACV should raise owner pay capacity; if churn rises, the pricing win gets eaten by replacement sales.

Track weighted monthly revenue per customer.

Watch enterprise onboarding time.

Log support hours by tier.

Compare one-time fees to setup cost.

Validation and Compliance Credibility

Validation and Compliance Credibility

Credibility costs cash, but it can raise price. In personality assessment software, validation audits take 4% of revenue in Year 1 and 2% in Year 5, while legal and compliance fees add $2k/month. Security setup capex of $12k and algorithm development capex of $80k hit cash before distributions, so owner pay depends on whether trust helps sell higher-ACV enterprise deals.

The tradeoff is simple: these costs lower near-term free cash flow, but they can cut buyer risk and support enterprise pricing. If validation and privacy work do not change close rates or price, they act like overhead. If they help win larger contracts or reduce procurement delays, they protect margin and make owner draws steadier as recurring revenue builds.

Track Trust Costs Against Price Lift

Measure this like a sales asset, not a science project. Track audit spend as a share of revenue, legal and compliance cash burn, and whether each security or validation step helps move deals from pilot to paid. The clean test is whether the added margin from trust covers the added compliance load.

Audit spend as % of revenue

$2k/month legal and compliance cash burn

$12k security and $80k algorithm capex

Enterprise price lift after trust reviews

Price enterprise tiers to recover the cost of credibility. If validated assessments, privacy controls, and security reviews shorten procurement or support a higher annual contract value, the payoff shows up in better cash flow and a bigger owner draw; if not, keep the spend tight and the product stack lean.

Gross Margin After Delivery Costs

Gross Margin After Delivery Costs

When delivery costs stay low, more of each subscription dollar can reach the owner. In this model, hosting, scoring, support, payment, and validation sit below revenue. Modeled delivery costs fall from 10% of revenue in Year 1 to 6% in Year 5, so gross margin rises from 90% to 94%.

That 4-point lift matters because it adds cash for payroll, sales, and owner draw. Sales commissions and payment processing add another 8% in Year 1, and psychometric maintenance plus content updates stay in the cost base because credibility is part of the product. On $1,000,000 of revenue, a 94% gross margin keeps about $40,000 more than a 90% margin before fixed overhead.

Keep Cost Per Assessment Low

Track cost per completed assessment, not just total spend. Split it into hosting, scoring, support, payment fees, validation, and content updates. If support tickets, retakes, or validation work rise, gross margin can slip fast even when revenue grows. That pushes out the point where the owner can take profit instead of reinvesting every dollar.

Use a simple monthly check: gross margin = revenue minus delivery costs. Then watch the drivers behind it. If delivery costs move from 10% to 6%, the business keeps more cash from each sale, but if commissions or payment fees creep up, the owner feels it in lower distributions and tighter working capital.

Track support cost per assessment

Review validation work monthly

Price for payment fees

Budget content updates as core cost

Customer Acquisition Cost

Customer Acquisition Cost

Customer acquisition cost (CAC) is the cash spent to win one new customer, including paid ads, outbound sales, partnerships, demos, and enterprise procurement. In this model, CAC improves from $450 in Year 1 to $350 in Year 5, so growth needs less upfront cash as the customer base matures.

That matters for owner income because lower CAC shortens payback and speeds up distributions. With annual marketing spend rising from $120k to $450k, long sales cycles can make EBITDA look fine while cash stays tied up in pipeline, so the bank balance can lag profit.

Keep CAC payback tight

Track CAC by channel, not as one blended number. Measure spend, closed customers, and payback time for each path, then compare paid ads, outbound, partnerships, and enterprise demos against the cash they bring back.

Move budget toward the channels that close faster and need fewer follow-ups. If CAC payback runs long, the company may need larger reserves before it can safely pay the owner, even when revenue and EBITDA are growing.

Staffing and Operating Costs

Staffing and Operating Costs

When payroll grows faster than revenue, owner pay gets squeezed. In this model, staffing costs rise from $450k in Year 1 to $1.325M in Year 5, plus $12k per month in fixed overhead, or $144k per year. That mix includes the CEO, lead industrial-organizational psychologist, engineers, account executives, and customer success managers.

The key issue is timing. Founder-led sales and support can protect cash early, but it also limits scale and raises burnout risk. If hiring adds capacity before recurring revenue can carry it, owner take-home stays thin even when topline growth looks good. One clean rule: payroll should grow only when the revenue base can pay for it.

Track payroll against recurring revenue

Watch monthly payroll, fixed overhead, and revenue per employee. Here’s the quick math: if staffing and overhead rise faster than subscription cash, profit turns into headcount, not distributions. Track how many demos, onboarding tasks, and support tickets each hire removes from the founder so you can see whether the team is really buying owner time.

Use a hiring gate tied to cash, not hope. Add roles only when the next hire can lift sales, retention, or delivery enough to cover their cost. If the founder is still handling sales and support, document the hours spent each week; once that load blocks growth, the business needs staff, but the payback has to show up in margin and cash flow.

Customer Retention

Customer Retention

For personality assessment software, retention is what keeps ARR and owner draws steady. Retained hiring teams, HR departments, coaches, and organizations keep subscription and assessment revenue active. In the model, lifting trial-to-paid conversion from 15% to 22% means more cash from the same traffic, while stronger retention also lowers replacement sales pressure and helps protect EBITDA. If churn rises, CAC payback stretches and cash gets tighter.

Track Retention by Account Type

Track churn, active accounts, and trial conversion by segment. Here’s the quick math: if 100 trials start, 15 pay at a 15% rate, but 22 pay at 22%. That gap compounds across monthly subscriptions and assessment volume. If free-trial starts rise from 5% to 10%, top-of-funnel growth only helps if onboarding is fast and users reach value before the trial ends.

Use onboarding checklists, usage nudges, and quarterly check-ins with hiring teams. If onboarding takes 14+ days, churn risk rises, so fix first-run setup before spending more on ads. Better retention makes monthly revenue less jumpy and gives more room for owner distributions.