Owner income$135k–$5.53M

Owner income$135k–$5.53MWhat Pottery Owners Really Earn

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$135k–$5.53M  Net margin3.0%–8.3%

Net margin3.0%–8.3% Revenue for target pay$4.48M

Revenue for target pay$4.48M Business difficultyHard

Business difficultyHard

You’re trying to see if the studio can pay you after rent, payroll, clay, glaze, firing, and marketing In this five-year US planning model, EBITDA rises from $135,000 in Year 1 to $5529 million in Year 5, but that is not guaranteed owner salary, tax advice, or cash you can withdraw without reserves

Owner income$135k–$5.53MNet margin3.0%–8.3%Revenue for target pay$4.48MBusiness difficultyHardWant to test your pottery studio owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Pottery Studio model?

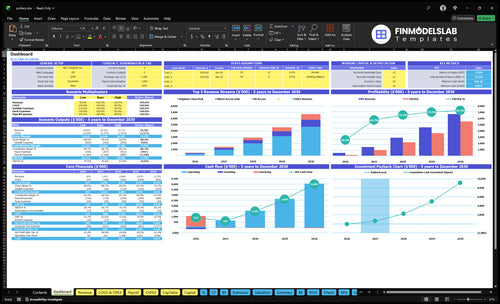

The screenshot shows dashboard, owner income, revenue assumptions, expense build, payroll, scenarios, and cash flow in the Pottery Studio Financial Model Template; open it to check classes, memberships, wheel access, private events, retail ceramics, reserves, and capex. It also shows EBITDA from $135k to $5.529m, occupancy from 400% to 850%, and a $831k minimum cash need in Month 2.

Owner-income model highlights

- Owner take-home outputs

- Revenue and margin tabs

- Payroll and kiln costs

- Cash need in Month 2

Does hiring instructors make a pottery studio more profitable?

Yes, but only if the added classes fill up enough to pay for the extra payroll. In a Pottery Studio, an owner who teaches, cleans, and handles admin can earn more early on, while hiring instructors can raise capacity but usually cuts per-class margin unless occupancy and pricing rise. Year 1 payroll can include a $50k lead instructor, a $40k workshop instructor at 0.5 FTE, a $55k studio manager, and assistant support, so this is not passive income unless volume covers that cost.

Owner-led setup

- Owner teaching keeps payroll light.

- Cleaning and admin stay in-house.

- Early income can be higher.

- Margin stays under tighter control.

Hired instructor setup

- Adds class capacity fast.

- Raises fixed payroll pressure.

- Needs stronger occupancy to work.

- Needs higher pricing to protect margin.

What pottery studio operating costs reduce owner take-home?

Owner take-home gets squeezed fast in a Pottery Studio because Year 1 variable costs can hit 170% of revenue, so higher sales do not automatically mean more profit. High sales still can leave thin cash if classes need paid instructors and kiln use rises. If you want the setup side, see How Much Does It Cost To Open A Pottery Studio?

Variable costs

- 80% consumable materials

- 40% firing kiln costs

- 40% marketing

- 10% tool replacement

Fixed overhead

- $8,275/month fixed overhead

- $5,500/month rent

- $1,200/month utilities

- $137.5k to $220k/year payroll

Can a pottery studio support an owner’s full-time income?

Yes, a Pottery Studio can support a full-time owner, but only after rent, payroll, variable costs, reserves, and debt service are covered; this model shows Month 2 breakeven and $135k Year 1 EBITDA. For the growth lens behind that pay decision, see What Is The Most Important Metric To Measure The Growth Of Pottery Studio?.

Owner pay reality

- $135k EBITDA before owner cash planning

- Hold cash for kilns and tools

- Reserve working capital before full draw

- Debt service lowers safe owner pay

Risk points

- $1,375k annual payroll starts early

- $993k/year fixed overhead is heavy

- 400% Year 1 utilization drives model

- Below target, owner pay tightens fast

Want the six pottery studio income drivers?

1

40%-85%Seat Utilization

With 22-26 billable days and 40%-85% occupancy, every extra filled seat spreads fixed rent over more sales and lifts take-home.

2

$80-$280Pricing Mix

The $80-$280 price ladder, plus private events at $15K-$55K, raises cash per booking without adding many extra studio hours.

3

$137K-$220KLabor Mix

Payroll rises from about $137.5K to $220K a year, so matching instructor FTE to demand is a direct win for owner income.

4

$8.3K/moOverhead Control

Fixed overhead is $8,275 a month, so tighter rent, utilities, and studio spend protect cash even when bookings dip.

5

8-16Repeat Sales

All-access grows from 8 to 16, and repeat buyers keep the studio fuller between new class pushes.

6

9%-12%Retail Margin

Consumables at 8%-6% and kiln firing at 4%-3% keep sold ceramics closer to pure cash.

Pottery Studio Core Six Income Drivers

Class Seat Utilization

Class Seat Utilization

Class seat utilization is how many pottery seats you actually sell in beginner classes, wheel-throwing sessions, hand-building workshops, and date-night events. In this model, occupancy rises from 400% in Year 1 to 850% in Year 5, while billable days move from 22 to 26. More filled seats lift revenue without changing rent, but only if instructor time, clay, glaze, firing, and cleanup still fit the room.

Empty seats hurt fast because fixed rent and payroll keep running. One clean rule: if a seat stays open, you still pay for the room, the teacher, and the overhead, so owner pay improves only when each added class covers its variable cost and adds to profit.

Track Fill Rate by Class Type

Measure filled seats by class type, not just total attendance. Track seats sold, billable days, instructor hours, and variable cost per class for clay, glaze, firing, and cleanup so you can see which sessions actually raise cash flow. A packed beginner class can beat a low-fill workshop even if both use the same room.

- Track fill rate by session type.

- Compare revenue per instructor hour.

- Watch firing and cleanup limits.

- Cut empty seats before adding days.

Test schedule changes first: add the class type that fills the fastest, then price it so the extra seat revenue clears material and labor cost. If utilization rises but staff time or kiln use spikes harder, owner income can still slip.

1

Pricing And Package Mix

Pricing and Package Mix

Pricing and package mix set revenue per customer. When wheel access moves from $80 to $100, beginner packs from $150 to $190, and all-access from $220 to $280, the same seat base can lift monthly sales without adding rent. But if prices sit below local demand, instructor time, materials, and firing costs, the studio can look busy and still leave weak owner pay.

Private pottery events also matter: monthly event income ranges from $15k to $55k. The inputs are customer count, package mix, repeat rate, included clay and glaze, firing load, and instructor hours. Gross margin, the money left after direct class costs, has to stay healthy or higher volume will not translate into cash for payroll, utilities, and the owner.

Price for margin, not just seats

Track revenue per seat, direct class cost, and event margin by package. Test price lifts one offer at a time, then watch occupancy, repeat bookings, and cash after materials and firing. If a package fills fast but creates weak take-home, it is too cheap for the cost structure.

- Measure gross margin by package.

- Log materials and firing per class.

- Compare event income by month.

- Raise prices in small steps.

- Protect owner pay first.

One full class at the wrong price can lose more value than three empty seats. Price should match local demand and the real cost of instruction, supplies, cleanup, and kiln use.

2

Memberships And Repeat Customers

Repeat Members

Memberships turn one-time students into recurring cash. Wheel access, all-access, continuing classes, studio passes, and alumni workshops reduce dependence on beginner sales. The catch is capacity: shelf space, member supervision, wheel time, and firing slots must stay balanced, or recurring revenue just creates crowding. Marketing can drop from 40% of revenue in Year 1 to 25% in Year 5 when repeat students keep coming back.

Manage the Member Mix

Track active members, renewal rate, class fill rate, wheel utilization, and firing capacity together. Recurring income lifts owner pay only if low-priced members do not crowd out higher-margin classes or overload staff. One crowded membership tier can look healthy on revenue and still cut profit if it blocks better-priced seats.

- Watch monthly churn and renewals.

- Cap low-price memberships by capacity.

- Protect wheel and kiln slots.

- Compare member revenue to class margin.

3

Retail Ceramics Margin

Retail Ceramics Margin

Retail ceramics can add income through mugs, bowls, ceramic art, student supply add-ons, gift cards, and seasonal sales. But gross margin is not owner profit. You still pay for making time, breakage, display space, packaging, and unsold stock, so a full shelf does not always mean more take-home pay.

For a pottery studio, this driver works best as an add-on to classes and events, not a separate cash sink. The real question is: does each retail sale cover labor, materials, and handling, and still leave cash for owner pay? If inventory turns slowly, it ties up money that could support rent, payroll, and firing costs.

Manage Add-On Sales

Track units sold, average ticket, breakage rate, and days in inventory. Separate made-to-sell items from student add-ons, because each has a different labor load and margin. Tie retail displays to class exits and event checkouts so the sale happens when foot traffic is already there.

Keep buying small and test what moves fast. If mugs or bowls sit past a normal selling window, cut reorder size before cash gets trapped. Gift cards and seasonal pieces can lift revenue without adding much shelf risk, while slow stock should not crowd out class space or steal time from teaching.

4

Instructor And Labor Structure

Instructor Payroll

Instructor and support pay is a direct drag on take-home income, because the studio has to cover a studio manager, lead instructor, part-time assistant, and workshop instructor. Year 1 payroll is $1375k and rises to $220k by Year 5, so every extra class must earn enough to pay for prep, admin, cleaning, and setup time.

Owner teaching can boost cash in the short run, but it can also hide the real labor cost. Paid instructors only improve profit if occupancy and pricing cover the full labor load, plus the time it takes to run classes well. If seats are empty, payroll stays fixed and owner pay gets squeezed fast.

Track Labor Per Class

Measure labor by role and by class type: who taught it, how long prep took, and how much admin and cleanup it needed. Tie that to seat fill and price, because a filled class with weak pricing can still lose money once support time is counted. One clean rule: payroll has to scale with seats sold.

Watch three inputs every month: occupancy, average price per seat, and instructor hours per session. If adding instructors expands class times or skill levels, test whether the extra capacity actually lifts revenue enough to cover the higher payroll. If not, the owner is just buying busier days, not better pay.

- Track payroll by role.

- Test seat fill by class.

- Price for prep and cleanup.

- Limit low-value teaching hours.

5

Rent, Kiln, And Material Cost Control

Rent, Kiln, and Material Cost Control

Rent, kiln power, clay, glaze, and firing losses decide how much of each revenue dollar reaches the owner. Fixed overhead is $8,275/month, including $5,500 rent and $1,200 utilities, so weak cost control cuts take-home pay fast.

Year 1 is especially tight: materials are 80% of revenue and kiln firing costs are 40%, or 120% before rent and other overhead. By Year 5, that improves to 60% and 30%, but the owner still needs full kiln loads, low waste, and clean scheduling to protect cash flow.

Track cost per load, not just total spend

Measure materials as % of revenue, kiln cost per firing, and rent per booked hour. Here’s the quick math: if waste, re-fires, or half-full kilns rise, gross margin falls even when sales stay flat. Use batch firing, clay recycling, and tighter pour and trim controls.

- Track clay and glaze by class type.

- Fire full loads on set schedules.

- Keep safety and ventilation intact.

- Protect the customer experience first.

When rent is fixed, the real lever is better use of space and energy. Cutting waste here gives more room for owner draw, while sloppy firing or cheap materials can wipe out profit fast.

6

Compare low, base, and high pottery studio owner income scenarios

Owner income scenarios

Owner income moves with occupancy, billable days, and staffing. Early years are thin, while fuller class and membership use can lift earnings fast.

| Scenario | Low CaseLow case | Base CaseBase case | High CaseHigh case |

|---|---|---|---|

| Launch model | This is the lean starter path with the lowest modeled owner income. | This is the modeled middle path with steady owner income. | This is the stronger earnings path with the highest modeled owner income. |

| Typical setup | Lean starter model with 40% occupancy, 22 billable days, about $448k revenue, and heavy fixed and payroll costs. | Stable community studio at 75% occupancy and 24 billable days, with about $2.852m revenue, $2.15m EBITDA, and a staffed class mix. | High-utilization class-and-membership studio at 85% occupancy and 26 billable days, with about $6.653m revenue, $5.529m EBITDA, and fuller staffing. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $135k EBITDALow case | $2.15m EBITDABase case | $5.529m EBITDAHigh case |

| Best fit | Use this to stress-test the launch year and early cash burn. | Use this as the normal run-rate plan after the ramp period. | Use this to test upside if the studio fills out and fixed costs spread well. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Pottery Studio Porter's Five Forces Analysis

- Pottery Studio BCG Matrix

- Pottery Studio Business Model Canvas

- 7 Core KPIs for Your Pottery Studio

- Pottery Studio Business Plan Template in Pre-Written Word

- How to Increase Pottery Studio Profitability in 7 Practical Strategies

- Pottery Studio Running Costs: How Much To Operate Monthly?

- Pottery Studio Startup Costs: $1535K CAPEX Opening Budget

- Pottery Studio Financial Model Template in Excel

- How to Open a Pottery Studio in 3 to 6 Months With Classes Ready

- How to Write a Pottery Studio Business Plan: 7 Steps to Funding

- Pottery Studio Marketing Mix

- Pottery Studio Marketing Plan

- Pottery Studio Business Proposal

- Pottery Studio PESTEL Analysis

- Pottery Studio Pitch Deck Example Editable PPTX

- Pottery Studio Business SWOT Analysis

- Pottery Studio Value Proposition Canvas

Frequently Asked Questions

In this model, owner income is best viewed as pre-tax business cash flow, not guaranteed salary EBITDA is $135,000 in Year 1 and $5529 million in Year 5 Actual owner draw should be lower after taxes, debt service, kiln reserves, working capital, and any reinvestment needed to keep the studio running