Presentation Skills Training Owner Income: $145K Salary Plus Profit

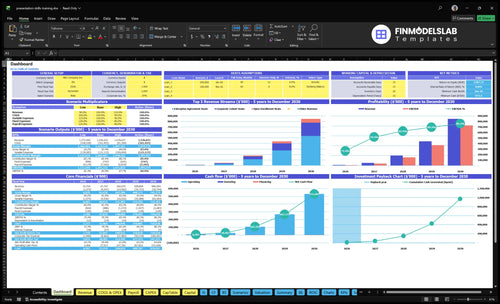

You’re estimating owner income, not a trainer wage or keynote speaking fee This model uses $10754M Year 1 revenue, $7790M Year 1 EBITDA, a $145,000 owner-operator salary, and reserve needs to frame possible take-home before personal taxes

Owner income$145kNet margin72%Revenue for target pay$200kBusiness difficultyHard

What drives owner take-home most?

1

Deal Size

$300-$25K

Bigger corporate cohorts, open enrollment seats, enterprise agreements, and coaching deals lift revenue per client and push owner income up fast.

2

Delivery Load

45%-88%

More billable days and higher occupancy turn the same team into more paid delivery, so revenue grows before headcount does.

3

Gross Margin

90%-94%

Materials and external coach commissions stay light, which keeps more of each training dollar above the line for owner pay.

4

Repeat Accounts

7x-10x

Growth in enterprise and cohort seats shows stronger repeat corporate buying, and that compounds revenue with less new sales work.

5

Lead Cost

8%-6%

As digital marketing drops from 8% to 6% of revenue, more of each sale drops through to profit before taxes.

6

Fixed Burn

$12.45K

With $12,450 of monthly fixed overhead and a $973K minimum cash floor, owner income only becomes usable after reserves are covered.

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Can a presentation skills training business scale beyond the owner?

Yes—Presentation Skills Training can scale beyond the owner, but the business changes from a pure teaching model into a managed delivery business. Here’s the quick math: the model grows senior communication coaches from 20 FTE in Year 1 to 100 FTE in Year 5, while enterprise agreement seats rise from 200 to 2,000 and corporate cohort seats from 120 to 900. Owner-led workshops keep more gross profit, but they cap delivery days; facilitator-led delivery expands revenue, and it adds hiring, quality control, scheduling, and customer success load.

What scales

20 FTE to 100 FTE by Year 5

200 to 2,000 enterprise seats

120 to 900 cohort seats

More seats means more revenue capacity

What gets harder

Owner-led work keeps margin higher

Delivery days stay capped by the owner

Facilitators need hiring and training

Quality control and scheduling become daily work

What profit margin can a presentation skills training business earn?

On the model as given, Presentation Skills Training can show a 724% Year 1 EBITDA margin, with $7,790M EBITDA on $10,754M revenue, as outlined in How Much To Start A Presentation Skills Training Business?. That only works if delivery COGS, marketing, and payment fees stay tight, because delivery COGS alone is 100% of revenue and is split 40% materials and 60% external coach commissions. Fixed overhead is $12,450 a month, payroll starts at $575,000 and rises to $1,910M by Year 5, so higher facilitator use can raise capacity but lower per-engagement margin.

Margin drivers

724% Year 1 EBITDA margin

$7,790M EBITDA

$10,754M revenue

100% delivery COGS

Cost pressure

40% materials

60% coach commissions

$12,450 monthly overhead

$575,000 to $1,910M payroll range

How much revenue does a presentation skills training business need for owner income?

If the goal is $145,000 in owner pay, Presentation Skills Training needs about $200,000 in base revenue at a 72.4% EBITDA margin, before reserves and timing gaps. The Year 1 model also shows a $575,000 payroll base and $149,400 in fixed overhead, so the real revenue target has to cover delivery costs, marketing, payment fees, and reserves too. Workshop count then comes down to the actual contract value per seat or cohort.

Owner pay math

$145,000 target owner pay

72.4% EBITDA margin used

About $200,000 base revenue

Reserves and timing add more

Revenue drivers

$575,000 payroll base

$149,400 fixed overhead

Delivery costs reduce margin

Contract value sets workshop count

Key Takeaways

Higher contract values lift revenue without more leads.

Billable days drive income, but burnout risk rises.

Delivery costs fall from 100% to 60% by Year 5.

Cash reserves protect client delivery when revenue lags.

Compare low, base, and high owner-income cases

Owner income scenarios

Income moves with seat volume, occupancy, and coaching mix. Fixed staff and platform costs stay in play, so early ramp and later scale produce very different owner take.

Low, base, and high cases show how owner income shifts as delivery fills up.

Scenario

Low CaseRamp period

Base CaseBoutique scale

High CaseHigh scale

Launch model

This is the ramp case, with the business still building demand and utilization in the first year.

This is the modeled steady case, with Year 3 demand and fuller use of the coaching team.

This is the upside case, with Year 5 scale and strong seat fill across corporate and enterprise work.

Typical setup

Year 1 uses 20 billable days, 45% occupancy, 120 corporate cohort seats, 50 open seats, and 200 enterprise seats, with $10.754M revenue and $7.790M EBITDA.

Year 3 uses 21 billable days, 75% occupancy, 480 corporate cohort seats, 150 open seats, and 1,000 enterprise seats, with $182.070M revenue and $149.960M EBITDA.

Year 5 uses 22 billable days, 88% occupancy, 900 corporate cohort seats, 250 open seats, and 2,000 enterprise seats, with $846.569M revenue and $729.650M EBITDA.

Cost drivers

20 billable days

45% occupancy

120 cohort seats

50 open seats

200 enterprise seats

21 billable days

75% occupancy

480 cohort seats

150 open seats

1,000 enterprise seats

22 billable days

88% occupancy

900 cohort seats

250 open seats

2,000 enterprise seats

Owner income rangeBefore owner reserves

≈$7.8MEarly ramp

≈$150.0MModeled steady

≈$729.7MFacilitator-supported scale

Best fit

Use this to stress-test launch month hiring, lead flow, and how fast the first cohorts fill.

Use this for a working plan if Year 3 occupancy and seat mix land near model.

Use this if corporate and enterprise delivery keep scaling and the coach bench holds.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Presentation Skills Training Core Six Income Drivers

Average Contract Value

Average Contract Value

Average Contract Value is the average dollars earned per training deal, and it matters because higher contract value lifts revenue without needing the same jump in lead volume. For this business, seat pricing runs from $300 to $550 in Year 1 and rises to $380 to $650 by Year 5, depending on audience level, customization, coaching add-ons, and deliverables.

Here’s the quick math: when corporate cohorts, open enrollment, or enterprise agreements move up in price, each closed deal contributes more to gross profit and owner pay. But premium pricing only works when the program shows outcomes, not just promises. If the offer is vague, discount pressure goes up and take-home income gets squeezed.

Price by outcome, not by seat count

Track ACV by segment every month: corporate cohort seats, open enrollment seats, and enterprise agreements. Compare sold price to the planned range, then check whether coaching add-ons or extra deliverables actually raise cash collected. If discounts are common, your ACV is weaker than your sales pitch suggests.

Use this control list to protect margin and owner income:

Price by audience level

Charge for customization

Separate coaching add-ons

Record discount rate

Test outcome-based packaging

When ACV rises, fewer deals can still fund the same overhead. That helps cash flow, makes forecasts cleaner, and gives the owner more room to pay themselves without chasing every extra lead.

Overhead And Reserves

Lean Overhead And Cash Reserves

When corporate payments land unevenly, $12,450 in monthly fixed costs can eat owner pay fast. That overhead includes rent, learning software, insurance, legal and accounting, video conferencing, and CRM tools, so distributions should wait until those costs are covered from collected cash, not just booked revenue.

The reserve floor is the real guardrail: $973,000 in Month 1 is about 78 months of fixed overhead at the stated burn rate. That cushion protects payroll, delivery quality, and client commitments, but it also delays take-home income until cash timing is steady enough to pay the owner without risking operations.

Track Cash Before Owner Draws

Measure owner pay against cash collected after fixed overhead, not against invoices sent. The key inputs are collected contract cash, monthly fixed costs, payroll or coach payouts, and the reserve floor. If cash stays below $973,000, keep distributions lean so the business can absorb slow closes and delayed renewals.

Watch monthly fixed spend.

Track cash by collection date.

Separate booked revenue from cash.

Pause draws when reserves dip.

Cut waste in office tools, admin services, and unused software before touching delivery spend. A small drop in overhead lifts owner income more safely than chasing extra sales, because every $1 saved goes straight into cash reserve or profit draw capacity.

Sales Pipeline Efficiency

Sales Pipeline Efficiency

Sales pipeline efficiency is the cost of finding, qualifying, and closing corporate buyers compared with the revenue they bring in. In Year 1, digital marketing and lead acquisition can absorb 80% of revenue, which leaves very little for delivery, overhead, and owner pay. By Year 5, that burden drops to 60%, so more cash stays in the business.

Here’s the quick math: if revenue is $100,000, acquisition cost is $80,000 in Year 1 and $60,000 in Year 5. The rest only helps the owner if contracts close and cash collects. Lead volume alone does not pay the owner. Close rate, contract value, and collection speed matter more than raw inquiries.

Improve Close Rate, Not Just Lead Count

Track qualified leads, proposal-to-close rate, cash collected, and cost per closed deal. If referrals, past-client expansion, partnerships, webinars, and targeted outreach lower acquisition spend, owner income rises faster because less revenue gets burned before delivery even starts. A better funnel beats a bigger funnel when the bigger one does not convert.

Use a simple rule: if a channel brings names but no signed contracts, cut it. If a campaign drives one enterprise account that renews or expands, keep it. The real test is revenue kept after selling costs, not lead count. That is what protects margin and makes owner draws more stable.

Track cost per closed contract

Measure cash collected, not leads

Prioritize referrals and past clients

Drop low-close channels fast

Repeat Corporate Accounts

Repeat Corporate Accounts

Repeat HR, sales enablement, leadership development, and executive communication accounts make owner income steadier. Here’s the quick math: enterprise agreement seats rise from 200 in Year 1 to 2,000 in Year 5, a 10x lift, while corporate cohort seats grow from 120 to 900, or 7.5x. That kind of renewal base cuts pressure on new lead volume and smooths monthly cash for salary and profit draw.

This driver includes renewals, seat expansion, and multi-team adoption. The key inputs are repeat account count, seats per account, renewal timing, and expansion rate. What this estimate hides is scope creep: if programs drift into vague “communication support” instead of measurable training paths, renewals can stall and margin falls because you keep selling from scratch.

Track renewals, not just sign-ups

Measure renewal rate, seats per account, and expansion months. A repeat client that adds seats is worth more than a one-off cohort, because sales cost per seat drops while cash comes in on a steadier cycle. If one account renews into multiple functions, that can protect owner pay even when new lead flow slows.

Build each account around a named training path for HR, sales, or leaders, and tie expansion to clear outcomes. Track which path converts from 120 to 900 seats and which stalls. If a client needs custom work but no clear seat growth, price it carefully so delivery time does not eat the margin that funds distributions.

Facilitator Gross Margin

Protect Facilitator Gross Margin

Gross margin is what’s left after direct delivery costs. In Year 1, delivery costs are 100% of revenue, split between 40% training materials and 60% external coach commissions, so there’s no gross profit left for overhead or owner pay. If delivery stays this expensive, the business can grow in sales and still leave the owner with very little cash.

By Year 5, delivery costs drop to 60%, so every $1.00 of revenue keeps $0.40 before overhead. Owner-led delivery can lift margin fast, but it caps capacity. Contractor or employee delivery can expand sessions, but it adds margin pressure plus quality and scheduling risk. One clean rule: if direct delivery cost rises, owner draw falls.

Measure and Cut Delivery Cost

Track revenue per session, materials cost, coach commission, and direct delivery hours for each cohort or workshop. Use this formula: gross margin = revenue - direct delivery cost. If a program can’t reach the 60% cost level by Year 5, it may not leave enough gross profit to cover fixed costs and pay the owner well.

Test the delivery mix in small steps. Keep owner-led sessions where quality matters most, then add contractors only when booking volume is full enough to absorb the extra cost. Watch for gaps in instructor availability, because missed sessions hit cash flow fast. The key question is simple: does each delivery model raise take-home income after direct cost?

Paid Delivery Volume

Paid Delivery Volume

Paid delivery volume is the number of workshop days, cohort sessions, enterprise sessions, and coaching slots you can bill. The model uses 20 billable days per month in Year 1 and 22 in Year 5, a 10% lift. That only helps owner income if the time is paid; selling, prep, travel, admin, and follow-up are not billable time.

Here’s the quick math: more paid days raise revenue without the same jump in lead volume. But if utilization rises without ops support, burnout and quality risk rise fast. The model’s occupancy input moves from 450% to 880%, so the real limit is not demand alone, but how many high-quality delivery days the owner can sell and close each month.

Protect Billable Time

Track billable days, non-billable hours, and paid-to-total time every month. If you are already at 20+ paid days and still doing nights of prep and follow-up, the calendar is too full. Set a cap before more volume is added, and move admin, scheduling, and materials work off the owner.

Forecast owner pay from paid days × average contract value, then stress test it at 20 and 22 days. If delivery demand keeps climbing but support stays flat, add contractor help or tighter session formats first. More paid volume only improves take-home income when quality stays high and unpaid work does not swallow the extra cash.