Medical Prior Authorization Service Owner Income: $175K CEO Assumption

You’re pricing owner pay before the workflow has proved itself This US planning model covers first-year revenue of $1287 million, a $175,000 CEO salary assumption, staffing, software, compliance, reserves, and owner take-home before taxes, not a guaranteed salary or clinical billing claim

Owner income$175kNet margin-0.9% to 45.1%Revenue for target pay$1.29MBusiness difficultyHard

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income will move with revenue, margin, staffing, overhead, reserves, and debt.

Want to check owner income in the full Medical Prior Authorization Service model?

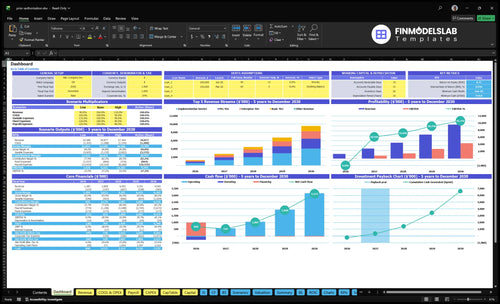

The Medical Prior Authorization Service Financial Model Template shows revenue, EBITDA, owner salary, breakeven, payback, and minimum cash. Open it to see the assumptions tab, revenue build, staffing plan, and scenario outputs; Year 1 revenue is $1.287M, Year 2 is $2.809M, Year 5 is $9.565M, EBITDA runs from -$11k to $4.314M, and minimum cash is $519k.

Owner-income model highlights

Owner salary and take-home

Revenue, EBITDA, and costs

Tier pricing and scenarios

How many clients does a prior authorization service need to pay the owner?

A Medical Prior Authorization Service needs about 7 average clients to cover $175,000 owner pay only, before labor, overhead, taxes, and variable costs; for operating discipline, tie this to What 5 KPI Metrics Should Medical Prior Authorization Service Business Track?. In the fuller Year 1 cost view, the target is closer to 42 average clients if owner pay sits on top of payroll, fixed costs, and marketing.

Owner Pay Math

45% at $1,200/month

40% at $2,500/month

15% at $5,000/month

Weighted MRR: $2,290/client

Real Cost Load

Owner pay: $14,583/month

Fixed costs: $14,400/month

Payroll: $670,000/year

Marketing: $120,000/year

Can a solo owner run a prior authorization service?

Yes, a solo owner can start a Medical Prior Authorization Service, but it is not a true solo workload. The Year 1 operating plan is 7 roles total — 1 CEO, 3 authorization specialists, 1 CTO, 1 sales and account manager, and 1 customer success representative — so owner labor may save cash early, but it hides the replacement cost of the work and the owner’s salary should stay separate from business profit and distributions.

Lean start reality

7 roles total in Year 1

6 hires beyond the owner

Owner labor saves cash early

Hidden replacement cost stays real

Managed team upside

Lean staffing improves capacity

Payroll lowers short-term profit

Team supports growth and retention

Better for multi-location accounts

What affects prior authorization service profit margins?

Margins on a Medical Prior Authorization Service get squeezed mainly by labor hours per request, denial rework, payer portal complexity, missing documentation, specialist wages, referral commissions, and security overhead. In Year 1, 3 FTEs at $65,000 each means $195,000 in authorization payroll, plus 8% of revenue for HIPAA cloud and data security and 10% referral commissions if rework adds time. If you want the cost side, see What Are Operating Costs For Medical Prior Authorization Service?

Main margin pressure

Labor hours per request

Denial rework adds time

Payer portals slow handling

Missing docs trigger delays

Track these KPIs

Requests per specialist

First-pass completion rate

Turnaround time

Provider documentation gaps

Medical Prior Authorization Service Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

What drives owner income most?

1

Provider Volume

$1.3M-$9.6M

More provider clients push revenue from $1.3M in Year 1 to $9.6M in Year 5, and fixed cost gets spread wider.

2

Pricing Model

$1.2K-$5.8K

A stronger Pro and Enterprise mix lifts monthly fee per client from $1.2K to $5.8K, so each account pays back faster.

3

Workflow Efficiency

7 mo

Faster approvals shorten the cash cycle and help the model reach breakeven in Month 7 with a $519K minimum cash need.

4

Labor Productivity

3-25 FTE

If each specialist clears more cases, payroll grows slower than revenue, which protects profit as headcount scales.

5

Client Expansion

55%-75%

Keeping accounts and moving them into higher tiers lifts recurring revenue, and higher-tier share rises to 55%-75%.

6

Case Mix

18%-10%

Harder payer and specialty mixes can raise direct cost, and the model's combined direct load still runs 18%-10% as it scales.

Medical Prior Authorization Service Core Six Income Drivers

Provider Client Volume

Provider Client Volume

More active provider clients and steady authorization request volume grow recurring revenue, but quality matters more than raw count. The plan assumes a 45% Basic, 40% Pro, and 15% Enterprise mix, with revenue rising from $1.287 million in Year 1 to $9.565 million in Year 5.

Low-volume accounts still use onboarding, portal setup, and account management time, so weak fit can drag margin. The main inputs are active clients, requests per client, tier mix, and churn. If volume stays soft or churn runs high, breakeven can slip past Month 7 and squeeze owner pay.

Track Volume That Pays

Qualify each client by expected monthly requests before you sign. The best accounts are the ones that keep requests steady enough to cover fixed service time and keep cash moving.

Track requests per client each month

Measure onboarding hours per account

Watch churn by tier

Flag low-volume, high-touch clients

Review tier mix monthly

Here’s the quick test: more requests per active client should raise revenue faster than support time rises. If a client is busy on paper but thin in volume, it can still be a weak account because the setup and follow-up work do not shrink much.

1

Pricing Model

Price to the Work

The pricing model controls how much cash each active client brings in. With $1,200 Basic, $2,500 Pro, and $5,000 Enterprise, plus a $2,000 implementation minimum, the service can cover its $14,400/month fixed load faster. Here’s the quick math: 12 Basic, 5.8 Pro, or 2.9 Enterprise clients cover fixed costs before labor and rework.

If price does not match scope, turnaround time, documentation burden, payer portals, and rework, busy accounts can still be unprofitable. Stronger minimums protect gross margin and make owner pay more stable because each client pays for the work it creates, not just the account name.

Track Scope Before You Quote

Price the account, not just the clinic. Track what drives effort so the fee matches the workload and the owner keeps the margin.

Count active clients by tier.

Track monthly authorization request volume.

Measure payer portals per account.

Log rework hours and appeal touches.

Watch turnaround time by client.

If one client brings more missing notes, slower responses, or more portal work, move it to a higher tier or raise the implementation floor. That keeps cash flow cleaner and reduces the chance of busy but low-profit accounts.

2

Authorization Workflow Efficiency

Authorization Workflow Efficiency

Cleaner intake, standard checklists, portal tracking, and fewer rework loops protect margin without adding clients. The key inputs are first-pass completion, turnaround time, open requests by payer, missing documentation, and rework hours. When each request takes fewer touches, labor cost per request falls, so more of the subscription fee turns into cash the owner can keep.

This matters because Year 1 EBITDA is -$11,000. With that little cushion, small workflow leaks can wipe out owner pay flexibility fast. Automation can help with routing and status tracking, but it does not fix bad intake or sloppy handoffs. One missing note can trigger another portal touch, another delay, and another cost.

Track the Rework Rate

Measure first-pass completion by payer and specialty, then link it to rework hours per request. If one payer keeps driving missing documents, tighten the checklist before volume grows. The point is simple: fewer back-and-forth loops mean faster completion and better margin.

Track open requests by payer weekly.

Count missing-documentation items.

Log every rework hour.

Compare turnaround time by client.

Use those numbers to staff and route work. If requests pile up in one portal, fix the intake step or the handoff step first. Faster completion lowers labor cost per request, and that is the cleanest path to better owner income when the model is still close to break-even.

3

Labor Productivity

Specialist Productivity

Labor productivity is the main cost lever after pricing. Year 1 assumes 3 authorization specialists at $65,000 each, or $195,000 total, and the team grows to 25 FTEs by Year 5. If each specialist handles more requests with less rework and less supervision, gross margin improves and more cash is left for owner draws after reserves.

The key inputs are requests handled per specialist, training time, supervision load, and error rework. Owner-performed authorizations can cut early cash burn, but that work does not scale into profit. The business wins when trained staff handle more clean requests per hour, because every extra request spread across fixed labor lowers cost per case.

Track Requests Per Trained Specialist

Measure output by specialist, not just headcount. Track how many requests each person closes, how long new hires take to become productive, and how many cases bounce back for missing data or payer follow-up. That tells you whether labor is turning into margin or just payroll.

Use standard intake checklists, clear handoffs, and error logs to cut rework. If a specialist needs heavy oversight, that cost belongs in the model. Better productivity lifts gross margin, helps protect monthly cash flow, and makes owner pay more reliable after operating reserves are covered.

4

Payer And Specialty Complexity

Payer and Specialty Complexity

Payer rules, specialty mix, missing notes, and appeals can push one prior auth request from a quick task into a long one. That changes labor hours per case, and in a service with $14,400/month fixed costs, extra rework can wipe out profit fast. The issue is not medical advice; it’s operational load, queue aging, and slower cash flow.

Here’s the quick math: if a client looks large on paper but drives more portal touches, document requests, and denial follow-up, the account can become low-profit even at a strong monthly fee. Complex cases often need higher retainers, volume bands, or rework fees so revenue matches the work. One messy payer mix can change owner pay more than a small client add.

Price and track complexity

Measure complexity by payer, specialty, denial rate, appeal volume, missing-note requests, and aging work queues. If the account needs more portal touches or follow-up, price it like a heavier workload, not like a simple one. That keeps gross margin closer to plan and protects cash for payroll and owner draws.

Track denial follow-up time.

Count portal touches per request.

Flag documentation requests early.

Review aging work queues weekly.

Bill rework when scope expands.

If a specialty or payer keeps creating appeals, the fix is pricing and scope control, not more unpaid labor. Tie the contract to request volume and complexity bands so the team can stay productive and the owner can still pay themselves after overhead.

5

Retention And Expansion

Retention and Expansion

Retention keeps recurring subscription revenue steady and lowers the need to replace churn with paid acquisition. In Year 1, $120,000 of marketing at $2,400 CAC supports about 50 client wins; by Year 5, $450,000 of marketing at $1,800 CAC implies about 250 wins. Higher retention makes each client worth more months of fee income, which improves cash flow and gives the owner more room to pay themselves.

For this service, retention depends on fast turnaround, clear communication, clean account management, and strong reporting. Expansion can come from more providers, more locations, or higher tiers. One clean renewal is cheaper than replacing the account, and one expanded account is better than chasing a new one.

How to improve retention and expansion

Track renewal rate, expansion revenue, CAC, and churn by client type. Also watch which accounts need the most follow-up, because slow status updates and messy handoffs usually hit renewals first. If a client renews but stays at one provider when it could add locations, you’re leaving margin on the table.

Report turnaround times weekly.

Review open issues by account.

Ask for expansion at renewal.

Fix communication misses fast.

6

Medical Prior Authorization Service Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Owner income shifts with staffing depth, payer volume, and overhead. A lean setup keeps cash needs lower, while the modeled and scaled cases can support higher earnings if volume lands.

Low, base, and high income cases for a prior authorization service.

Scenario

Low Caseowner-operated

Base Casestaffed

High Casemanaged-team

Launch model

The owner does more of the authorization work, keeps hiring light, and accepts slower revenue growth.

This is the modeled case with Year 1 revenue of $1.287M, EBITDA of -$11k, CEO pay of $175,000, breakeven in Month 7, minimum cash of $519,000, and payback in 20 months.

The upside case scales toward Year 5 revenue of $9.565M and EBITDA of $4.314M with a larger operating team.

Typical setup

Lower volume, fewer hires, and lean overhead keep cash needs down, but the owner absorbs the replacement work and scale stays limited.

The plan uses the modeled team mix, with 3 authorization specialists in Year 1, 1 sales and account manager, 1 customer success rep, 8% HIPAA cloud and security cost, and 10% referral commissions.

The business runs with 25 authorization specialists, 5 sales and account managers, and 8 customer success reps, while referral commissions fall to 6% and HIPAA cloud and security cost drops to 4%.

Cost drivers

Founder labor

fewer specialists

lower payroll

smaller cash reserve

10% referral commissions

CEO pay $175k

3 authorization specialists

1 sales manager

1 customer success rep

10% referral commissions

25 authorization specialists

5 sales managers

8 customer success reps

6% referral commissions

4% cloud and security

Owner income rangeBefore owner reserves

Salary onlyLow income base

$175k salary plus profitModeled earnings

Salary plus upside profitUpside earnings

Best fit

Best for a founder-led start that stress-tests how much one owner can carry before service quality slips.

Best for planning around the core model and checking whether cash, staffing, and breakeven timing hold up.

Best for operators testing a larger provider book and a team-led service model that can support stronger margins.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

The model uses a $175,000 annual CEO salary assumption, but Year 1 EBITDA is -$11,000 after payroll and overhead By Year 2, EBITDA reaches $811,000 on $2809 million of revenue Owner distributions, if any, should come after taxes, reserves, debt service, and reinvestment

The researched model reaches breakeven in Month 7 and payback in 20 months It also needs a minimum cash cushion of $519,000 in Month 6 That cash gap matters because payroll, marketing, compliance, and technology costs arrive before provider revenue fully ramps

Yes, plan for compliance and data security costs from the start This model includes $2,500 per month for legal and regulatory compliance, $1,200 per month for professional liability insurance, and HIPAA cloud hosting and data security at 8% of Year 1 revenue

Owner salary is planned compensation for work performed distributions are profit taken after the business can afford them In this model, the CEO salary is $175,000, while EBITDA moves from -$11,000 in Year 1 to $811,000 in Year 2 Taxes, reserves, capex, and reinvestment reduce distributable cash

Hire when request volume, turnaround promises, and client service needs exceed owner capacity This model starts with 3 authorization specialists at $65,000 each, then grows to 6 in Year 2 and 25 by Year 5 Hiring too early burns cash hiring too late risks churn and rework

About the author

Philip Stone

Business Model Writer

Philip Stone is a business model writer at Financial Models Lab, focused on the economics behind day-to-day business operations. He explains startup planning in plain language, helping aspiring small business owners think through the money questions new founders ask. With a clear, grounded approach, he helps readers compare business opportunities realistically and choose ideas that fit their goals without getting lost in heavy finance jargon.

Choosing a selection results in a full page refresh.