How Much Proprioception Training Owners Make: $169K Year 1 Surplus

You’re modeling owner take-home, not a guaranteed salary This estimate covers first-year revenue of about $635,940, listed operating costs, admin payroll, fixed overhead, marketing, billing, equipment planning, and cash available before personal taxes, debt service, reserves, and any unmodeled clinician payroll

Owner income$1.69MNet margin42% to 75%Revenue for target pay$4.0MBusiness difficultyMedium

What drives proprioception training owner income most?

1

Session Volume

463-3.2K/mo

More completed treatments drive the biggest income jump, rising from 463 a month in Year 1 to 3,173 in Year 5 while fixed costs spread out.

2

Collections

$114-$125

Higher collections per session lift revenue on every visit, so the move from about $114 to $125 per treatment feeds straight into take-home.

3

Utilization

55%-88%

Higher booked time pushes more revenue through the same clinician base, and assistant utilization reaches 88% in the model.

4

Staff Mix

5-25 FTE

The team scales from 5 total FTE in Year 1 to 25 in Year 5, and the split between senior staff and assistants shapes labor margin.

5

Overhead

$11.2K/mo

Monthly fixed overhead of $11.2K means each extra treatment matters more once the clinic covers rent, software, insurance, and admin.

6

Referral Flow

8.0%-4.5%

Lower direct marketing and referral spend keeps more collected revenue in the business as the clinic matures.

What could your proprioception training program pay you?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. Actual owner income depends on collections, staffing, pay mix, reserves, debt, and timing. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see the full owner-income model?

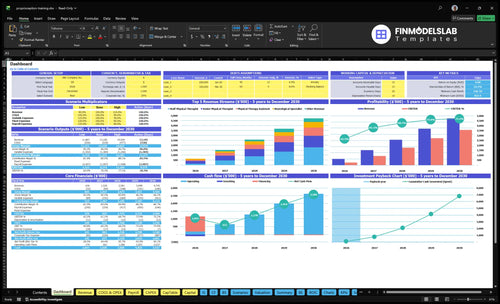

This dashboard shows revenue assumptions, clinician capacity, payer mix, expense buildout, cash flow, owner compensation, and scenario testing in Proprioception Training Program Financial Model Template; open the model. It also shows $635,940 Year 1 revenue, $2.58 million Year 3 revenue, $4.74 million Year 5 revenue, and $1.687 million Year 1 operating surplus before exclusions.

Owner-income model highlights

Owner pay stays visible

Revenue and margin tracked

Scenario testing cuts risk

What expenses reduce proprioception training program owner income?

The biggest income drains in a Proprioception Training Program are admin payroll, lease, billing, referral marketing, supplies, insurance, software, utilities, and maintenance; in Year 1, admin payroll is $212,000 and fixed overhead is $11,200 per month. Here’s the quick math: listed variable costs hit 190% of revenue in Year 1, including 60% billing and 80% direct marketing and referrals, while COGS is 50% for medical supplies, tape, and patient education materials; see How Increase Profits Proprioception Training Program?. No-shows reduce paid sessions, but rent and salaries still run, and clinician payroll must be modeled separately if it is not already in the wage data.

Big cost pressure points

$212,000 admin payroll in Year 1

$11,200 fixed overhead each month

190% variable costs of revenue

50% COGS for supplies and materials

Costs that still run

No-shows cut paid sessions

Lease still gets paid

Salaries still get paid

Clinician payroll may be separate

Can a proprioception training program owner make more by hiring clinicians?

Yes — hiring clinicians can raise revenue capacity for a Proprioception Training Program, but it can also cut margin if utilization (booked session rate) is weak or payroll runs too high. An owner-as-clinician keeps more gross margin, yet session volume caps out; a hybrid owner-manager can add the $115,000 Clinic Director role and still take distributions if profit supports it. In the staffed model, the plan scales from 5 provider roles in Year 1 to 25 in Year 5, and mature-year revenue reaches $474 million at 3,173 monthly completed treatments.

Owner-led model

Keeps more gross margin

Caps sessions and visits

Limits payroll exposure

Fits tighter quality control

Hired-clinician model

Raises revenue capacity

Needs strong utilization

Adds $115,000 director cost

Raises scheduling and referral risk

How much revenue does a proprioception training program need to pay the owner?

For a Proprioception Training Program, revenue alone does not tell you if the owner gets paid. Using the model’s 81% contribution margin, you need about $612,800 of annual revenue to cover $134,400 fixed overhead, $212,000 admin payroll, and $150,000 in pre-tax owner cash before reserves. At the model revenue of $635,940, there’s about $168,700 left before exclusions.

Quick math

$134,400 overhead

$212,000 admin payroll

$150,000 owner cash target

$612,800 revenue needed

What the model says

81% contribution margin

$635,940 model revenue

$168,700 before exclusions

Owner pay comes after costs

Key Takeaways

Completed sessions, not leads, drive revenue.

Year 1 averages 463 treatments monthly.

Collections average about $114 per treatment.

Fixed overhead starts at $11,200 monthly.

Compare lean, base, and mature owner-income scenarios

Owner income scenarios

Owner income moves with visit volume, weighted collections, and how much payroll and overhead the clinic carries. Higher capacity helps, but clinician payroll, reserves, taxes, debt, and execution can cut take-home.

Low, base, and high cases show how sessions and cost load change owner income.

Scenario

Low CaseLow Case

Base CaseBase Case

High CaseHigh Case

Launch model

This is the lower owner-income path.

This is the modeled middle path.

This is the stronger earnings path.

Typical setup

Year 1 runs at 463 monthly sessions, about $114 weighted collections, $635,940 revenue, 190% listed variable cost load, $134,400 fixed overhead, and $212,000 admin payroll.

Year 3 reaches 1,810 monthly sessions, about $119 weighted collections, $2,581,000 revenue, 152% listed variable cost load, and $340,000 admin payroll.

Year 5 reaches 3,173 monthly sessions, about $125 weighted collections, $4,745,000 revenue, 133% listed variable cost load, and $420,000 admin payroll.

Cost drivers

463 monthly sessions

$114 weighted collections

190% variable cost load

$134.4k fixed overhead

$212k admin payroll

1,810 monthly sessions

$119 weighted collections

152% variable cost load

$340k admin payroll

Year 3 scale

3,173 monthly sessions

$125 weighted collections

133% variable cost load

$420k admin payroll

Year 5 scale

Owner income rangeBefore owner reserves

About $270kLow income band

About $1.77MBase income band

About $3.57MHigh income band

Best fit

Use this to stress-test a slow launch and early capacity ramp.

Use this as the working plan for a steady clinic ramp and normal execution.

Use this to test upside if capacity stays full and collections hold.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Proprioception Training Program Core Six Income Drivers

Weekly Completed Sessions And Utilization

Weekly Completed Sessions

Completed sessions are the paid visits that actually finish, not leads or booked slots. In Year 1, the model shows 463 completed treatments per month, or about 107 per week. By Year 5, that rises to 3,173 per month, or about 732 per week. More completed visits lift revenue first, then help cover fixed costs like rent, software, insurance, and admin payroll.

The key risk is simple: no-shows and underfilled clinician calendars cut income fast while overhead stays flat. Here’s the quick math: if a session is not completed, that revenue is gone, but the monthly cost base does not shrink with it. So this driver changes owner pay through higher top-line revenue and better absorption of fixed costs before profit is shared.

Track Fill Rate and Show Rate

Measure scheduled visits, completed visits, and show rate every week. The model’s utilization assumptions range from 550% for the neurological specialist to 700% for the physical therapy assistant in Year 1, so even small gaps in fill hurt fast. If schedules slip, revenue falls before margins do, which means less cash for owner draw.

Track the drivers that change completed sessions: open slots, no-show rate, care-plan completion, and clinician hours used. Keep calendars tight, confirm visits early, and watch weekly completed treatments against the target of 107 in Year 1 and 732 by Year 5. That is the lever that turns fixed overhead into profit.

Referral Flow And Patient Retention

Referral Flow and Retention

For this program, referral flow is the count of referral sources, booked evaluations, completed sessions, and care-plan follow-through. In Year 1, direct marketing and referrals are modeled at 80% of revenue, then 45% by Year 5. That tells you the business starts with a heavy pipeline load, so weak referrals or drop-off quickly shrink cash flow and owner pay.

Here’s the quick math: more booked evaluations only help if they become completed treatments. Physician referrals, sports medicine partnerships, and senior fitness channels all matter, but retention matters just as much. If care plans stall early, clinician calendars open up, revenue per fixed dollar falls, and the clinic still has rent, software, insurance, and admin payroll to cover.

Track the full referral funnel

Measure referrals received, booked evaluations, completed sessions, and care-plan completion rate each week. If referrals are strong but visits stay light, the problem is conversion, not awareness. If visits start but end early, retention is the leak. That gap raises marketing spend and cuts clinician utilization, which hits gross margin fast.

Set source-level targets for physician, sports medicine, and senior fitness channels, then compare them to cash collected per completed treatment. A simple rule helps: when referral volume drops, reforecast capacity and fixed-cost coverage right away. One clean line: empty schedules are expensive.

Track source-to-evaluation conversion

Track evaluation-to-start conversion

Track completed-session rate

Track care-plan drop-off by source

Program Packages And Service Mix

Program Packages And Service Mix

This driver is the mix of one-on-one assessments, multi-session plans, group balance classes, sports injury add-ons, wellness packages, and fall-prevention programs. It moves income by changing weighted average collections, room use, and clinician scheduling. In Year 1, session prices range from $85 for an assistant session to $145 for a specialist session, with model collections around $114 per completed treatment.

A richer mix lifts owner pay because the same clinic hour can produce more revenue if higher-priced visits and packages are attached to the right patient. If the schedule fills with low-rate sessions, revenue per hour drops even when volume is steady. The key inputs are completed visits, package length, session mix, and the share of higher-priced follow-ups.

Build packages that match the patient mix

Start with a simple path from evaluation to next step: a balance assessment plus a multi-session plan, or a fall-prevention package for seniors. Measure package attach rate, average visits per client, and collections per treatment. Keep specialist slots for the hardest cases and use assistant-led follow-ups where fit allows; that protects margin and keeps rooms full.

Track revenue per clinic hour.

Watch package attach rate weekly.

Price by complexity, not habit.

Match group classes to demand.

Limit low-value slot crowding.

Clinician Labor Model

Clinician Labor Cost

This driver is the pay for clinicians and support staff needed to deliver each session. It hits gross margin fast: owner-led sessions can lift near-term cash, but they cap capacity; contractors cut fixed payroll risk but can cost more per session; employed therapists need strong utilization. Owner clinical pay must be separated from business profit, or take-home income gets overstated.

Year 1 support wages already total $212,000 for the Clinic Director at $115,000, Office Manager at $55,000, and Patient Coordinator at $42,000. With 463 completed treatments per month, labor cost per visit is a key margin test. Here’s the quick math: if labor rises before volume does, the owner’s draw shrinks even when revenue looks steady.

Track Cost per Completed Session

Track labor cost per completed session, not payroll alone. Split out owner clinical compensation, then test three cases: owner-delivered, contractor, and employed therapist. If support staff free clinicians to treat more patients, the extra admin pay can be worth it. If they do not lift completed sessions, they just add fixed cost.

Build a monthly model that shows pay by role, sessions per clinician, and utilization. The useful question is simple: does each added labor dollar create more completed treatments than it costs? If not, gross margin falls fast and cash left for owner pay gets thin.

Fixed Overhead And Clinic Setup Costs

Fixed Overhead And Setup Cost Pressure

A proprioception training clinic carries $11,200 in monthly fixed overhead before the first visit is completed: $6,500 lease, $850 software, $1,200 liability insurance, $950 utilities and internet, $600 janitorial, and $1,100 office admin and legal. At the model’s $114 average collection per completed treatment, overhead alone needs about 99 completed sessions a month just to break even on rent and admin.

The setup bill is also heavy at $65,500 for parallel bars and gait rails, a computerized balance plate system, a bodyweight support harness, and treatment tables. That spend does not hit monthly profit, but it does tie up cash, so low utilization makes the business feel expensive fast. One clean line: empty calendars turn fixed costs into pain.

Keep Overhead In Line

Track fixed overhead as a share of collected revenue and watch it against booked and completed sessions, not just evaluations. If utilization is soft, the lease and admin costs stay flat, so every missed treatment pushes owner pay farther away. The key test is simple: does monthly collection cover $11,200 plus clinician labor and still leave cash for the owner?

Monitor completed sessions each week.

Recheck break-even at 99 visits.

Delay nonessential equipment buys.

Match staffing to real volume.

If you’re below that volume, shorten burn by keeping the space lean, negotiating startup terms where possible, and using equipment only when it raises paid visits. More volume turns the same fixed cost base into operating leverage, which is what creates room for owner income.

Session Pricing, Collections, And Payer Mix

Session Pricing And Collections

Revenue per visit depends on what you actually collect, not just the posted rate. In Year 1, sessions are priced at $125 for senior physical therapist visits, $110 for staff therapist visits, $145 for neurological specialist visits, and $85 for physical therapy assistant visits, with weighted average collections of about $114 per completed treatment.

Cash-pay packages, copays, insurance collections, and negotiated rates all change that average. If the mix shifts toward lower-rate visits, the same calendar can produce less cash and a smaller owner draw. Model collections as an editable rate, because payer mix affects both profit and cash flow.

Track Realized Rate By Payer

Track completed treatments, collected dollars, and payer mix every month. Use the clean test: collected revenue ÷ completed treatments = realized revenue per session. If that slips below $114, profit drops even if visit count stays flat.

Split visits into cash-pay, copay, and insurance, then compare each one’s net cash and timing. If negotiated rates or denials push collections down, tighten the service mix toward higher-yield sessions or packages that fit the patient base.